Before the pandemic, fewer than 6% of Americans worked from home. But by the end of 2022, experts project that number will increase to 25%. So, there’s some bad news: The confusion around state tax withholding for remote employees is going to stick around—at least for the short term.

We know that withholding taxes can be tricky. Employees who commute to work in different states or who work in states different from their company headquarters can make things even more complicated, depending on the states involved.

COVID-19, lockdowns, and the rise of remote work only made things more confusing.

This article will help:

- Explain withholding for remote workers

- Provide an overview of temporary state rule confusion

- Prepare for what the future holds

State tax withholding for remote employees Q&A

Only seven states in the United States don’t have state income tax; the other 43 states (plus D.C.) do. Keep in mind how this affects you and your employees living or working in the following income tax-free states:

- Alaska

- Florida

- Nevada

- South Dakota

- Texas

- Washington

- Wyoming

Two additional states, New Hampshire and Tennessee, only tax interest and dividend income. If someone lives in a state that doesn’t withhold income tax but works in a state that does, they’ll usually pay nonresident taxes in the state where they work. The same is true if an employee works in a state that doesn’t withhold income tax but lives in a state that does—they’ll pay resident state taxes for where they live.

With this state income tax information in mind, take a look at the following state tax withholding questions and answers.

What is the general rule of income tax withholding?

According to the general rule of withholding, state income tax withholding for remote employees depends on where the employee performed the work.

Let’s look at an example. If an employee lives in Summerville, Georgia, but works in Mentone Alabama, you would only withhold Alabama state taxes because this is where the employee works. Your employee would then file state income tax in Georgia, and claim a credit for the taxes you withheld for Alabama.

There are some exceptions to this rule:

- States that have reciprocal agreements

- The convenience of the employer rule

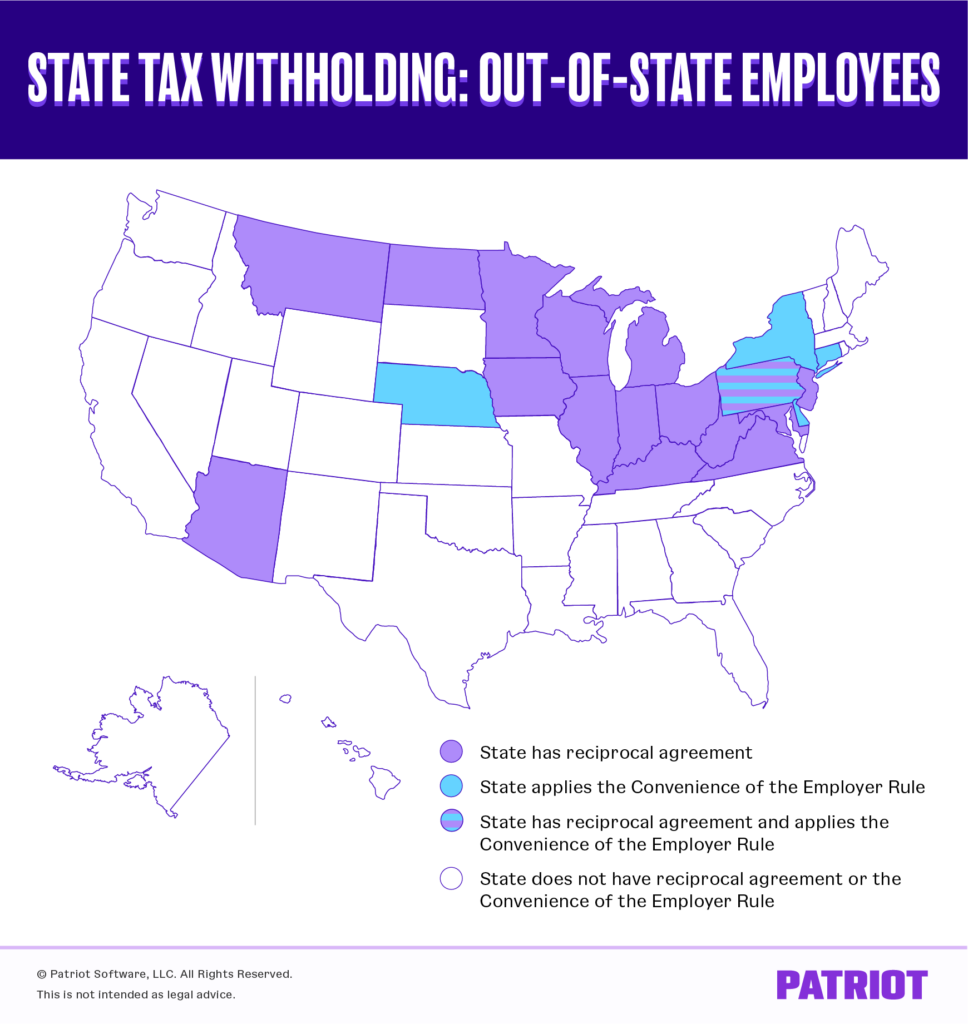

How do reciprocal agreements change tax withholdings?

When states have reciprocal agreements with each other (16 states do), basic tax withholding gets flipped upside down. Instead of tax withholdings from the state where the employee does the work, withholdings come from the state where the employee lives.

If your employee lives in a state with a reciprocal agreement, make sure you:

- Inform your employees of their state exemption form

- Stop withholding for the employee’s work state and withhold in their home state (after they complete the exemption form)

- Fill out W-2 form to let the employee know how much you withheld from their state income tax (at the end of the year)

As with all things tax-related, reciprocal agreements can be tricky. It isn’t safe to make assumptions.

Just because a state has a reciprocal agreement with another state doesn’t mean that neighboring states are included. Arizona, for instance, shares agreements with California, Indiana, Oregon, and Virginia. But, the four other states that share its borders aren’t included in the reciprocal agreement. Visit your employee’s state’s Department of Revenue to find out exactly what you need to know about reciprocal agreements.

Does the convenience of the employer rule change my tax withholdings?

The convenience of the employer rule has to do with the reasons for the employee living where they do—is it because it’s convenient for the employer or the employee?

If you require an employee to live in a different state for the purposes of their work (at the convenience of the employer), you must withhold taxes for that state. But if the employee works in a different state for their own reasons, you can withhold taxes for both states—the state where the business is located and the state where the employee chooses to live.

Unfortunately, this means that some employees may be taxed twice unless they use income tax credits supplied on their resident return.

There are five states that follow this rule: Delaware, Nebraska, New Jersey, New York, and Pennsylvania. Connecticut also applies the convenience of the employer rule but only if the employee’s resident state uses a similar rule for work performed for a Connecticut employer.

The complications of temporary state rules

When companies closed locations because of COVID-19, some states scrambled to create new rules. These new regulations allowed states to continue to tax non-resident workers even if they went remote and stayed home. The dispute between New Hampshire and Massachusetts is a prime example.

Before COVID-19, close to 100,000 New Hampshire residents would regularly commute to Massachusetts for work. Because New Hampshire doesn’t have an income tax, these employees didn’t pay one in Massachusetts.

When these employees were forced to stay home because of COVID-related shutdowns, Massachusetts created a new regulation (the “COVID sourcing regulation”) that suddenly taxed New Hampshire residents when they stopped commuting. The regulation sought to recoup lost income from any out-of-state residents who worked in Massachusetts before COVID-19 made them remote. It seems employees from New Hampshire got caught up in the safety net.

New Hampshire sued Massachusetts because this new taxation infringes on their state sovereignty.

New Hampshire v. Massachusetts eventually went to the Supreme Court where the court declined to hear the lawsuit. The Massachusetts regulation expired on June 15th, 2021, 90 days after Massachusetts lifted its state of emergency. But the question of how some states tax workers during exceptional disruptions, like lockdowns, is still up in the air.

So why does this matter, and how might it affect you? With the increase in out-of-state employees, states are working to create rules on taxation.

What the future holds

The world of remote work is alive and well. Because of this, both you and your employees should be on the lookout for changes in tax law. The Senate’s Remote and Mobile Worker Relief Act of 2021 would stop states from withholding taxes for nonresident employees who are only in the state for 30 days or less. If passed, this could help future workers disrupted by lockdowns. The House has introduced a similar bill, the Remote Worker Relief Act of 2020, that would limit the use of the “convenience of the employer” rule for nonresident workers.

Other than introducing the bills in late 2020 and early 2021, no other federal action has been taken. We can expect some movement on the bills later this year because Congress has two years to act once the bills are introduced.

This is not intended as legal advice; for more information, please click here.

{kind=link}