If you are a follower of my blog for a long, then you are aware that yearly I used to publish my Top 10 Best SIP Mutual Funds to invest in India. As usual, I am publishing my Top 10 Best SIP Mutual Funds to invest in India in 2022.

Note:- Refer to my debt funds recommendations for 2022 at “Top 10 Best Debt Mutual Funds to invest in India in 2022“.

First of all, I am really sorry for publishing this post late. Many of my readers waited a lot. However, due to my hectic Fee-Only Financial Planning Service, I was unable to publish as usual like during the months of December or January.

Let me recap what I have recommended last year (Top 10 Best SIP Mutual Funds to invest in India in 2021).

If you remember, since it’s almost two years, I stayed away from active fund recommendations and adopted the passive funds (Index Funds) and the reasons are as below:-

By adopting the Index investing, you are ending the search for the BEST MUTUAL FUND COMPANY and BEST FUND MANAGER. Investing in Index Fund and expecting the returns of the Index is the simplest way of investment. The only risk you can’t avoid is market risk, which you have to manage by proper asset allocation between debt and equity (I mean at the portfolio level).

As you may be aware, many AMCs are now launching a lot of Index Funds. Because they are trying to follow the trend. Few launched with an idea of low cost and few brought complications by launching smart-beta funds. However, in my view, owning the whole market (especially Nifty 100) is far better than these various smart-beta index funds. I know that they may reduce the volatility. However, it comes with compensation of returns. Hence, for simplicity, owning the Nifty 100 is far better. It remembers me the quote from John Bogle.

“The winning formula for success in investing is owning the entire stock market through an index fund, and then doing nothing. Just stay the course.”

– John C. Bogle, The Little Book of Common Sense Investing.

Owning Index Funds is fine. However, sticking to this strategy requires lot of patience. As you may be aware, day in and day out, we are flooded with information (I call it NOISE) and obviously, there may be few active funds and they may be currently beating the Index. During such a period, you start to doubt your strategy of adopting index investing.

John Bogle once said, “Buying funds based purely on their past performance is one of the stupidest things an investor can do.“. The majority of buying of new mutual funds is based on their past performance. We HOPE that past performance will repeat. However, fund managers themselves are not sure whether they repeat the same past performance. But, we the investors are forced to believe that it will repeat.

Sharing once again the quote of Morgan Housel.

“If I had to summarize my views on investing, it’s this: Every investor should pick a strategy that has the highest odds of successfully meeting their goals. And I think for most investors, dollar-cost averaging into a low-cost index fund will provide the highest odds of long-term success.” – Morgan Housel, The Psychology of Money (Timeless Lessons on Wealth, Greed and Happiness).

Hence, we all know that there are few fund managers who can BEAT the Index. However, finding such rare species that can beat the index CONSISTENTLY is the biggest task and in fact impossible task.

The cost you pay to them is fixed. However, the returns are not fixed. If a fund manager is claiming that his fund is beating the index, then you have to check what is the actual returns after cost and how consistently he can deliver returns.

How to choose the Best Index Funds?

When you decided to invest in Index Funds, you have to just concentrate on three aspects of the funds and they are as below.

# Expense Ratio:-Lower the Expense ratio is better for me.

# Tracking Error:-It is nothing but how much is the fund deviated in terms of returns with respect to the Index it is benchmarked. Lower the tracking error means better the fund performance. Few fund houses do not publish this data on regular basis. Hence, you have to be cautious with this data.

# AUM:-Higher the AUM means better the advantage for the fund manager to manage the liquidity issues.

If you go by these criteria, then Index NFOs are also not considered. Once they have decent AUM with historical tracking error, then you can consider them.

Basics of Investing Mantras

Now before jumping to investing, you must have an idea of what are the basics of investing. I repeat this exercise on yearly basis in my blog post. But still, find the same type of questions from the readers. Hence, to give you the clarity, I am writing once again.

As per me, before jumping into an investment, one must aware of how well they are prepared for facing financial emergencies. Financial emergencies maybe like loss of life, meeting with an accident, hospitalization or sudden income loss, or job loss.

Hence, the first step is to cover yourself with proper Life Insurance (Term Life Insurance where the coverage should be at least 15-20 times of your yearly income). You must have your own health insurance (rather than relying on employer-provided health insurance). Create better coverage with a family floater plan and Super Top Up Health Insurance. Ideally around 3-5 Lakh of family floater plan and around Rs.10-25 Lakh of Super Top Up is a must nowadays. Buy around 15 to 20 times of your monthly salary corpus as accidental insurance. Then finally create an emergency fund of at least 6-24 months of your monthly commitment. This will be handy whenever your income will stop or if you face any unplanned expenses.

Once these basics are done, then think of investing. If your basics are not done properly, then whatever investment building you are creating may tumble at any point of time. Let us move on and understand the basics of investing.

You must have a proper Financial Goal

I noticed that many investors simply invest in mutual funds just because they have some surplus money. The second reason may be someone guided that mutual funds are best in the long run compared to Bank FDs, PPF, RDs, or even LIC endowment products.

If you have clarity like why you are investing, when you need the money, and how much you need money at that time, then you will get better clarity in selecting the product. Hence, first, identify your financial goals.

You must know the current cost of that goal. Along with that, you must also know the inflation rate associated with that particular goal. Remember that each financial goal has its own inflation rate. For example, the education or marriage cost of your kid’s inflation is different than the inflation rate of household expenses.

By identifying the current cost, time horizon, and inflation rate of that particular goal, you can easily find out the future cost of that goal. This future cost of the goal is your target amount.

I have written a separate post on how to set your financial goals. Read the same at “Financial Goals – How to set before jumping into investing?”

Asset Allocation is MUST

Next step is to identify the asset allocation. Whether it is a short-term goal or a long-term goal, the proper asset allocation between debt and equity is a must. I personally suggest the below-shared asset allocation strategy. Remember that it may differ from individual to individual. However, the basic idea of asset allocation is to protect your money and smoothly sail to reach your financial goals.

If the goal is below 5 years-Don’t touch equity product. Use the debt products of your choice like FDs, RDs, Liquid Funds, Money Market Funds, or Ultra Short Term Funds.

If the goal is 5 years to 10 years-Allocate debt: equity in the ratio of 60:40.

If the goal is more than 10 years-Allocate debt:equity in the ratio of 40:60.

While choosing a debt product, make sure that the maturity period of the product must match your financial goals. For example, PPF is the best debt product. However, it must match your financial goals. If the PPF maturity period is 13 years and your goal is 10 years, then you will fall short of meeting your financial goals.

First fill the debt allocation with EPF, PPF, or SSY (based on the maturity and goal type). If you still have room to invest in debt, then choose the debt funds. Personally, my choice always is to fill these wonderful debt products like EPF, PPF, and SSY.

Return Expectation

Next and the biggest step is the return expectation from each asset class. For equity, you can expect around 10% to 12% return. For debt, you can expect around 6% to 7% returns.

When your expectations are defined, then there is less probability of deviating or taking knee-jerk reactions to the volatility.

Portfolio Return Expectation

Once you understand how much is your return expectation from each asset class, then the next step is to identify the return expectation from the portfolio.

Let us say you defined the asset allocation of debt:equity as 40:60. Return expectation from debt is 6% and equity is 10%, then the overall portfolio return expectation is as below.

(60% x 10%) + (40% x 6%)=8.4%.

How much to invest?

Once the goals are defined with the target amount, asset allocations are done, return expectation from each asset class is defined, then the final step is to identify the amount to invest each month.

There are two ways to do it. One is a constant monthly investment throughout the goal period. The second way is increasing some fixed % each year up to the goal period. Decide which suits you.

I hope the above information will give you clarity before jumping into equity mutual fund products.

How many mutual funds are enough?

How many mutual funds do we have? Is it 1, 3, 5 or more than 5? The answer is simple…you don’t need more than 3-4 funds for investing in mutual funds. Whether your investment is Rs.1,000 a month or Rs.1 lakh a month. With a maximum of 3-4 funds, you can easily create a diversified equity portfolio.

Having more funds does not give you enough diversification. Instead, in many cases, it may create your portfolio overlapping and leads to underperformance.

Few choose new funds for each goal. That creates a lot of clutter and confusion. Because, starting is easy and after few years, it looks like a hilarious task to manage. Hence, my suggestion is to have the same set of funds for all goals. Either you create a unified portfolio or create a separate folio for each goal and invest.

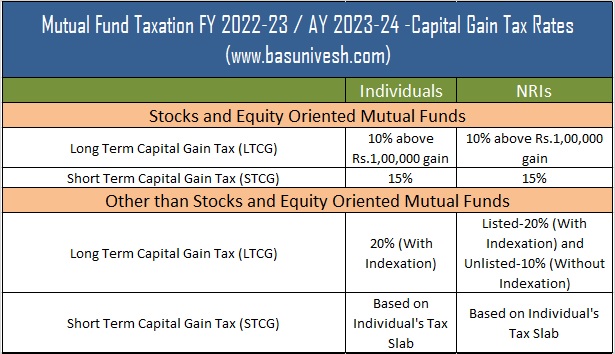

Taxation of Equity Mutual Funds for FY 2022-23

Remember that Equity Funds and Debt funds are taxed differently. Hence, you must understand the taxation part as well before jumping into investment. I tried to explain the same in the below image.

The rate of taxation is as below for the FY 2022-23 is as below.

I hope the taxation part is clear to all of you. If you still have doubts, then refer my latest post ”Mutual Fund Taxation FY 2022-23 / AY 2023-24“.

Top 10 Best SIP Mutual Funds to invest in India in 2022

I have written few posts in the last year which as per me are best to add value to your investment journey. Hence, suggest you to read them first (sharing the list below).

Now let us move on and share with you my Top 10 Best SIP Mutual Funds to invest in India in 2022.

Best SIP Mutual Funds to invest in India in 2022 -Large Cap

Last year I recommended two Large Cap Index Funds. I am retaining the same funds for this year too.

# UTI Nifty Index Fund-Direct-Growth

# HDFC Index Fund Sensex Plan-Direct-Growth

Best SIP Mutual Funds to invest in India in 2022 -Mid Cap

Last year, I recommended two Nifty Next 50 Index Funds. This year also, I am retaining the same funds for my recommendations in Mid Cap Funds. In my latest article Nifty Next 50 Vs Nifty Midcap 150 – Which is best?, I have given the reasons why Nifty Next 50 should be your better alternative than the Nifty Mid Cap.

Nifty Next 50 is actually an essence of both large-cap and mid-cap. Because of this, it acts with the same volatility as mid-cap. Hence, I am suggesting Nifty Next 50 as my mid-cap fund than particular Mid Cap Active or Index Funds.

I am continuing last year’s choices:-

# ICICI Pru Nifty Next 50 Index Fund-Direct-Growth

# UTI Nifty Next 50 Index Fund-Direct-Growth

Best SIP Mutual Funds to invest in India in 2022 -Flexi-Cap

Last year I recommended Parag Parikh Long Term Equity Fund and Axis Multi-Cap Fund. I am retaining both funds as usual.

# Parag Parikh Flexi Cap Fund-Direct-Growth

# Axis Flexi Cap Fund–Direct-Growth

Now, you may be surprised why I am recommending the Axis AMC fund when there is news of scam by fund managers. First thing, the fund managers who are involved in the front running are not managing this fund and hence have no impact on this fund. However, if you are uncomfortable with this AMC, then you can go with my favorite Parag Parikh Flexi Cap Fund.

Best SIP Mutual Funds to invest in India in 2022 – Equity Oriented Balanced Funds or Aggressive Hybrid Fund

Last year I recommended HDFC Hybrid Equity Fund and Franklin India Equity Hybrid Fund. However, this year, I am changing my recommendations in both the funds. Regarding HDFC, I am a bit skeptical about their debt portfolio which I noticed during the Covid period when they did some inter scheme transfer. Along with this, its consistent underperformance is one more reason. Regarding the Franklin, I am not sure how long they sustain with a bad history behind them (Franklin Templeton India Closed 6 Debt Funds – Is it right?).

Hence, this year, I am recommending two new funds in this category.

# SBI Equity Hybrid Fund

# Canara Robeco Equity Hybrid Fund

What if someone already invested in my earlier recommended funds? No need to panic. For few of my clients, I suggested continuing the HDFC Hybrid Fund. You can stop the fresh investment and start with these two funds. After a year or so, as per your tax liability, you can slowly move to the above-recommended funds.

Best SIP Mutual Funds to invest in India in 2022 – ELSS or Tax Saver Funds

Last year, I have recommended Birla Sunlife Tax Relief ’96 and DSP Tax Saver. This year also, I am maintaining the same.

# Aditya Birla Sun Life Tax Relief ’96 – Growth – Direct Plan

# DSP Tax Saver – Growth – Direct Plan

What about Small-Cap Funds?

Personally, I never invested in small-cap funds, and also for all my fee-only financial planning clients, I never suggest small-cap funds. I may be conservative. However, in the end, what I want is a decent return with sound sleep at night. Hence, this year, I thought not to recommend any small-cap funds.

So you noticed that there are no major changes this year (except Hybrid Funds). You can continue the same funds which I have recommended. However, don’t forget to check your asset allocation (at least once a year). It is very much important.

Finally, a list of my Top 10 Best SIP Mutual Funds to invest in India in 2022 are as below.

What is my style of construction Equity Portfolio?

I have listed all the funds above. However, I suggest constructing the portfolio as below within your equity portfolio.

50% Large Cap Index+30% Nifty Next 50+20% Hybrid Funds

50% Large Cap Index+30% Nifty Next 50+20% Flexi Cap Funds

50% Large Cap Index+20% Nifty Next 50+30% Hybrid Funds

50% Large Cap Index+20% Nifty Next 50+30% Flexi Cap Funds

However, my favorite is 80% Index and around 20% active (either through Hybrid or through Flexi Cap).

Disclosure:-I have investments in UTI Nifty Index Fund, ICICI Pru Nifty Next 50 Index Fund, Parag Parikh Flexi Cap Fund, and HDFC Hybrid Fund (will wait for few more years before taking a call on this) as equity part of my daughter’s educational goal and my retirement goal.

Conclusion:-These are my selections but it does not mean they must be universal selections. Hence, if you have a different opinion, then you can adopt so. You also noticed that I hardly change my stance until and unless there is a valid reason. In the end, investing is a BORING and LONG TERM journey ? Best of LUCK!!

{kind=link}