Dork alert – this blog may be dry, but I’ll try to keep it snappy.

I know this part is just re-writing the news, but let’s start with the facts:

- The Consumer Price Index (CPI) increased 1.0% in May, well above the +0.7% that was expected.

- The CPI is up 8.6% from a year ago. This is what a lot of dorks on CNBC refer to as “Headline CPI” because, well, it’s the number you see in the headlines.

- Headline CPI is usually broken down by the same dorks into something called Core CPI, which is everything EXCEPT food and energy prices. This is done because, historically, food and energy prices are very volatile, and with inflation, there is another group of dorks trying to identify a trend. Since these two components make that hard, they are stripped out to create the Core CPI.

- Core CPI rose 0.6% in May, above the 0.5% expected. By the way, the core prices are up 6% compared to a year ago.

- Energy prices increased 3.9%…that’s probably a big surprise to those of you who haven’t been to a gas station in a while.

- Food prices increased 1.2%.

So, looking more closely at the details of the latest report, energy prices with a +3.9% increase were the biggest contributor to the higher headline CPI reading – mostly thanks to gasoline.

Then there is the war tension in Ukraine and the re-opening of China from strict COVID lockdown enforcement that assure us energy will continue to impact consumer prices into the immediate future.

Food prices, the other volatile category, were driven by prices for dairy products. Dairy products posted their largest monthly increase in fifteen years.

SO, after removing these two components, it’s clear that there is additional inflationary pressure.

For example, housing rents (which is both rent prices AND the rental value of actual homes) were up +0.6%. That’s important because rents make up more than 30% of the headline CPI, and I’m not sure rents have caught up with actual home prices, which have skyrocketed more than 30% since COVID started.

Then there are the price increases across service categories like airline fares (+12.6%), car and truck rentals (+1.7%), and hotels/motels (+1.0%).

And go ahead, I dare you to tell me you DIDN’T just sing Sugar Hill Gang “Hotel, Motel, Holiday Inn” to yourself…

Anyway, back to the dorks…prices for new autos continued to rise, and used car prices rose 1.8% for the month as well.

No matter where you look or which way you cut it, inflation is high, and it has continued to rise.

But wait, you know I have a “but”.

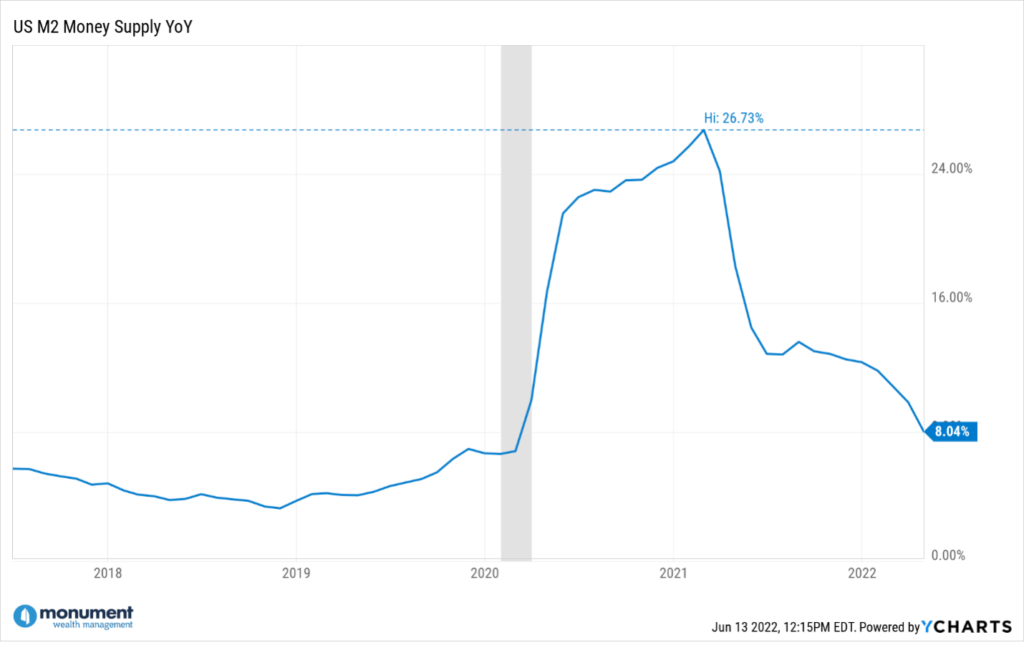

There is this thing that a whole OTHER group of dorks calls the “money supply” …AKA “M2”.

The M2 or money supply skyrocketed during COVID. See the chart below.

According to a research firm we follow, Trend Macro, there is a huge correlation between M2 and CPI, but CPI lags M2 by about 13 months.

So if M2 peaked at the beginning of 2021…and it’s now the summer of 2022…maybe…just maybe…we will see CPI come down based on M2 growth slowing.

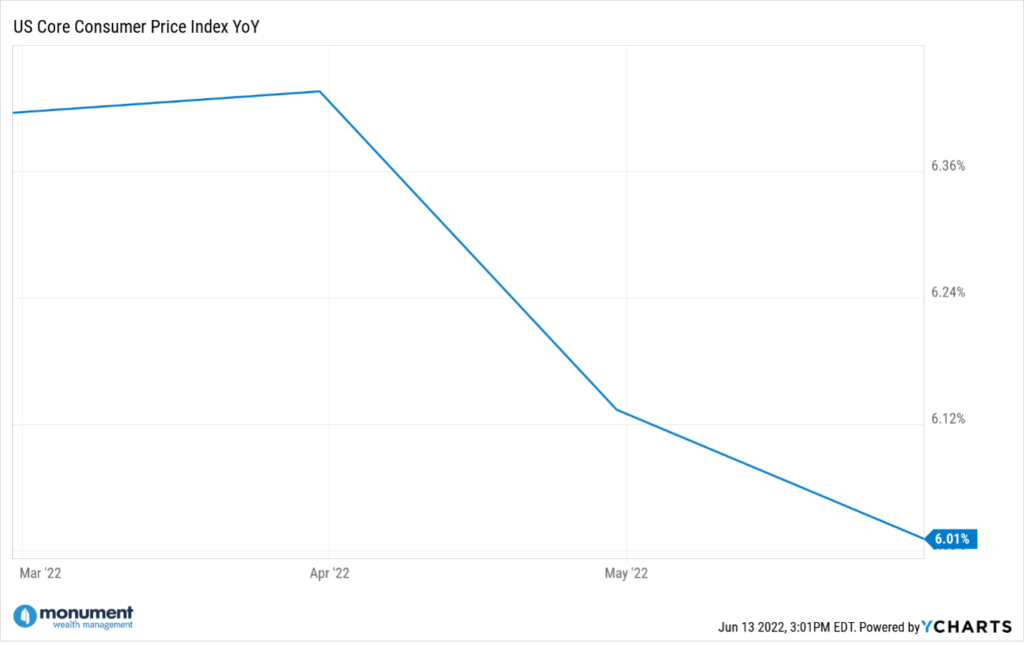

Meaning we’d need to see the year-over-year (Y/Y) Core CPI’s monthly reading start to trend DOWN.

But as I previously stated, the Y/Y Core CPI was up 0.6% in May, and we need to see the Y/Y Core CPI trending DOWN. We’d need to see something like this…

Wait, what?

Yeah, the Y/Y Core CPI has been LOWER for two straight months, almost exactly in line with the M2 downtrend that started in February 2021.

What if, and I’m just wondering here, but what if Core inflation keeps going down? Well then, all the Fed will have to do is wait.

Since most of the market tantrum we are seeing (Friday and today) is based on expectations that the Fed will take an even MORE aggressive stance on raising interest rates than was expected a few weeks ago, what happens if Chairman Powell DOESN’T get more aggressive?

Wednesday will tell all…I’m reading some dorks are expecting an increase of 75 basis points (bps), but what if it’s not?

If the Y/Y Core CPI keeps falling over the next few months in line with the reduction in M2 that started in February of 2021, it’s not inconceivable that Core CPI is back down to the Fed’s own target rate of 2.5% all by itself.

I’m not making a prediction, I’m just saying that it’s possible M2 is what was (and is) driving a lot of the CORE inflation.

And I’m saying that right now, any surprise of good news will have a similar effect as we see with the bad news.

So don’t mess around with your portfolios trying to guess all of this. Everything can change very quickly (of course, both for the good and the bad), but you can’t guess these things. Need more proof? Listen to our recent Off the Wall podcast with Dr. Daniel Crosby where he explains why.

The best news is that whether I’m right or wrong, it’s irrelevant because none of this is coupled with a recommendation to do anything. You should have the portfolio you need for tomorrow and not try to build the portfolio you WISH you had on January 5th.

Again, I’m not in the prediction business, but I am in the probability business, and no matter how you feel, there is NOT a 100% chance of anything. Someday a recovery will start, and I’m here to tell you that on March 9th of 2009, no one felt like that was the day it would all start to turn around.

And don’t even get me going on the topic of Christmas Eve of 2018.

(But if the Fed doesn’t raise by 75bps on Wednesday AND Powell is upbeat in his report, I’ll happily accept an opportunity to take a victory lap while you chant “Dork Dork Dork”!)

Keep looking forward.

{kind=link}