To fight persistent inflation, the Federal Reserve has committed to significantly cooling demand. This approach reflects a non-monetary policy failure to fix underlying supply-side challenges that are pushing up inflation. The Fed lacks policy tools to make these supply-side fixes, so it must rely on demand-side impacts to bring down inflation by reducing economic growth.

Consequently, at the conclusion of its June meeting, the Fed raised the federal funds target rate by 75 basis points, increasing that target to an upper bound of 1.75%. This is the largest increase for the funds rate since 1994 and is a clear response to elevated inflation data from May. Moreover, the Fed’s forward-looking projections indicate on a median participant basis an additional 205 basis points of tightening through 2023. Without convincing evidence of moderating inflation, the Fed is likely to continue to raise the target rate at each meeting by 50 basis points or more. The Fed’s target is a 2% inflation rate.

The Fed’s June statement also confirmed its existing plan to reduce its balance sheet, including net reduction of $35 billion of mortgage-backed securities a month when fully phased in. The lack of change for the balance sheet reduction plan is a positive element of today’s news for housing, as there was a risk of a planned faster pace, which would further increase mortgage interest rates.

Given signs of slowing economic activity, including six straight months of declines for home builder sentiment, a clear risk is that by falling behind the curve, the Fed will overshoot on tightening and bring on a recession as it fights inflation. This would not be the soft landing the Fed is attempting to orchestrate. Indeed, the NAHB economic forecast now includes a 2023 recession as financial conditions tighten. Chair Powell noted in his press conference that housing market conditions are slowing given higher mortgage rates.

The Fed notes that inflation remains elevated, citing the Ukraine war and global supply-chain issues, among other factors. Their revised economic projections find slowing economic growth, with a GDP outlook for 2023 of 1.7%. This will be very difficult to achieve. The Fed’s unemployment projection sees that rate increasing to 4.1% through 2024. So even under this optimistic outlook, this increase for joblessness would qualify as a growth recession.

As this economic slowing occurs, the Fed’s projections indicates inflation will decline. Using the core PCE measure, the Fed sees a 4.3% rate for 2022, then 2.7% in 2023 and falling to 2.3% in 2024. This too will be difficult to achieve given the lagged impact on inflation from increasing residential rents, which materialize in inflation readings on a lagged basis when leases are renewed. This shelter impact on inflation is also a reminder that tightening interest rate conditions can affect supply, not just demand. Higher rents are due to a lack of housing supply. And higher interest rates will make it difficult to finance the development of additional housing supply.

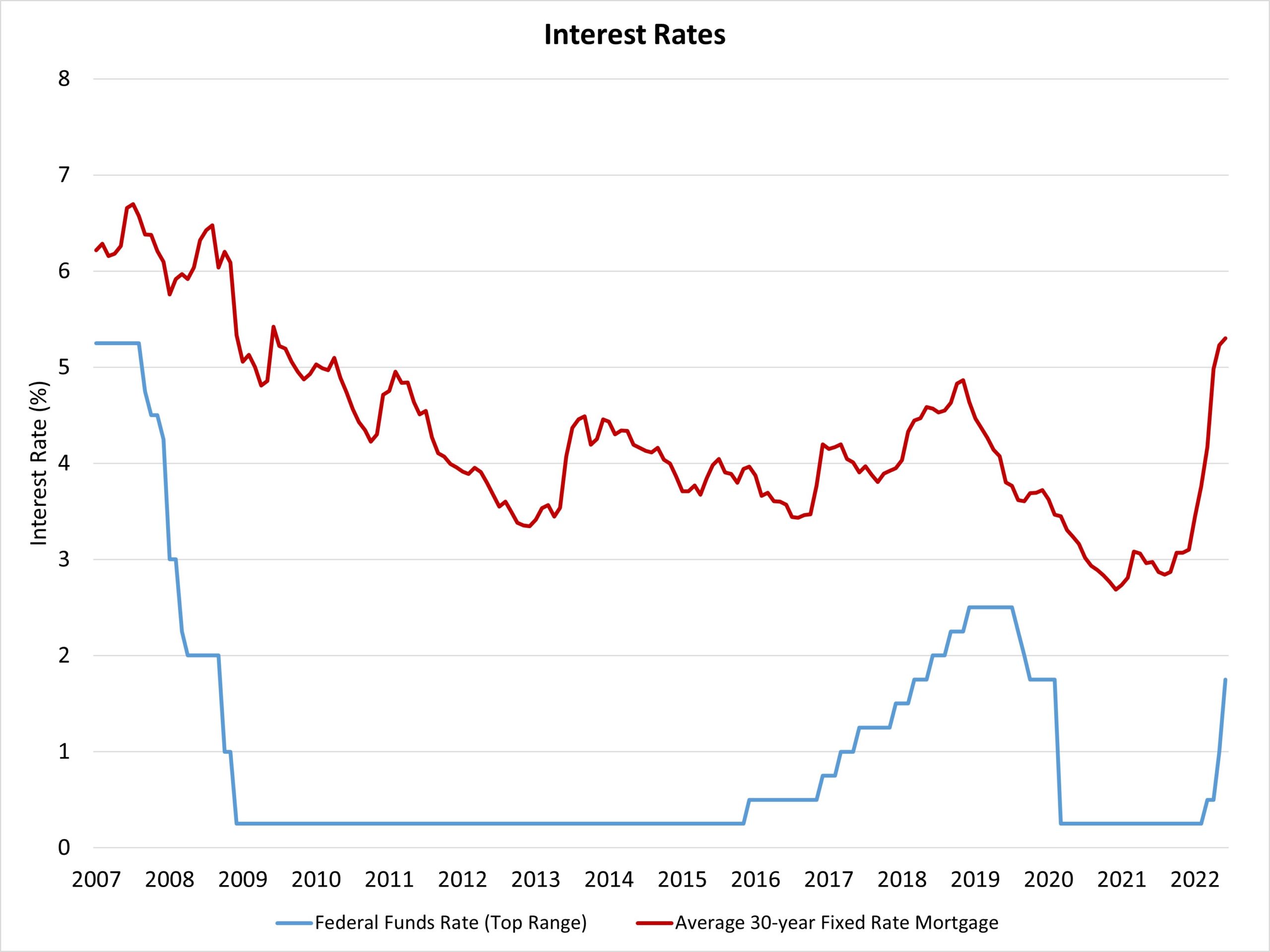

It is important to note that there is not a direct connection between federal fund rate hikes and changes in long-term interest rates. During the last tightening cycle, the federal funds target rate increased from November 2015 (with a top rate of just 0.25%) to November 2018 (2.5%), a 225 basis point expansion. However, during this time mortgage interest rates increased by a proportionately smaller amount, rising from approximately 3.9% to just under 4.9%.

Previously, the Fed noted that inflation is elevated due to “supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.” While this verbiage may incorporate policy failures that have affected aggregate supply and demand, I do think the Fed should explicitly acknowledge the role fiscal, trade and regulatory policy is having on the economy and inflation as well.

Given today’s projections, we reiterate our policy recommendation with respect to any possibility of a soft landing. Clearly, elevated inflation readings call for a normalization of monetary policy, particularly as the economy moves beyond covid-related impacts. However, fiscal and regulatory must complement monetary policy as part of this adjustment. Yet, many of these measures are simply beyond the Fed’s control.

For example, higher inflation in housing is due to a lack of rental and for-sale inventory and cost growth for building materials, lots and labor. Higher interest rates will not produce more lumber. A smaller balance sheet will not increase the production of appliances and materials. In short, while the Fed can cool the demand-side of the economy (reducing inflation and growth), additional output on the supply-side is required in order to tame the growth in costs that we see in housing and other sectors of the economy. And efficient regulatory policy in particular can help achieve this goal and fight inflation.

Related

{kind=link}