What’s driving inflation?

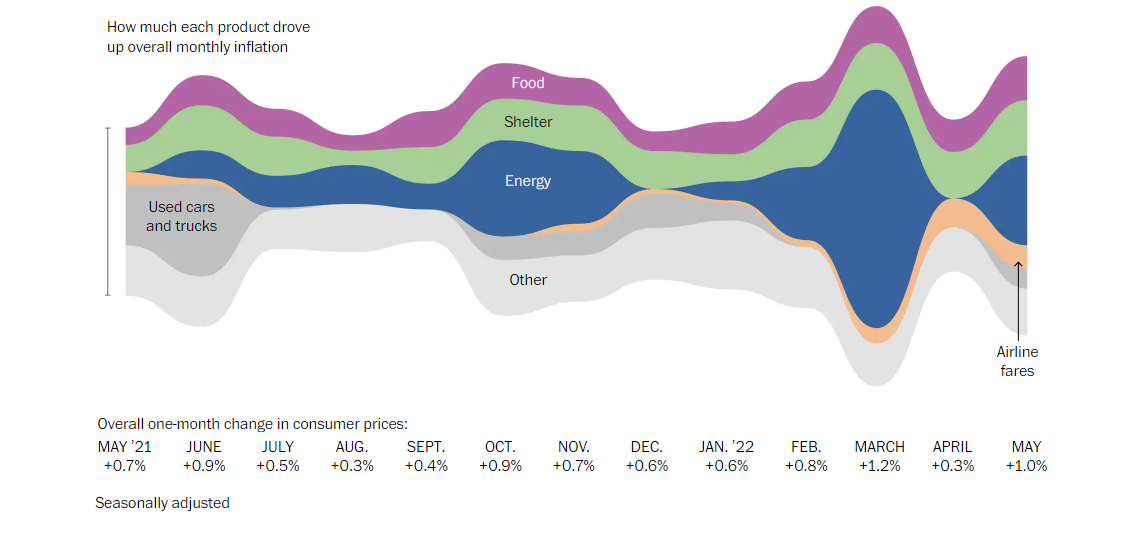

When we think about the prospects for future inflation increases, I think it’s important to consider what’s currently driving inflation and how it’s changing. The Washington Post published a useful graph last week:

My main takeaway from this graph is that what was pushing overall inflation numbers has varied dramatically over the last little while. One could find a plausible path back to high-but-reasonable inflation rates of 3% to 4% pretty easily if the war in Ukraine ended, leading to substantial quantities of grain, oil and gas flowing again. The problem is that (most) governments and central banks can’t end the war—all they can do is try to fix the inflation problem on the edges with monetary and fiscal tools that will likely have a minor impact if used correctly or make things much worse if used incorrectly.

Until we get back to a more stable inflation rate environment (and subsequent boringly predictable interest rate movements), investors might calm some of their anxieties by going beyond the headlines to understand just why asset prices are going down (versus panicking about the random walk downwards). They can also focus on practical ways of trying to avoid the worst impacts of inflation, thus lowering their personal inflation rate.

Buy when others are fearful: Is it time to be greedy about tech stocks?

Generals have a tendency to fight the last war. Investors have a tendency to fight the last bubble.

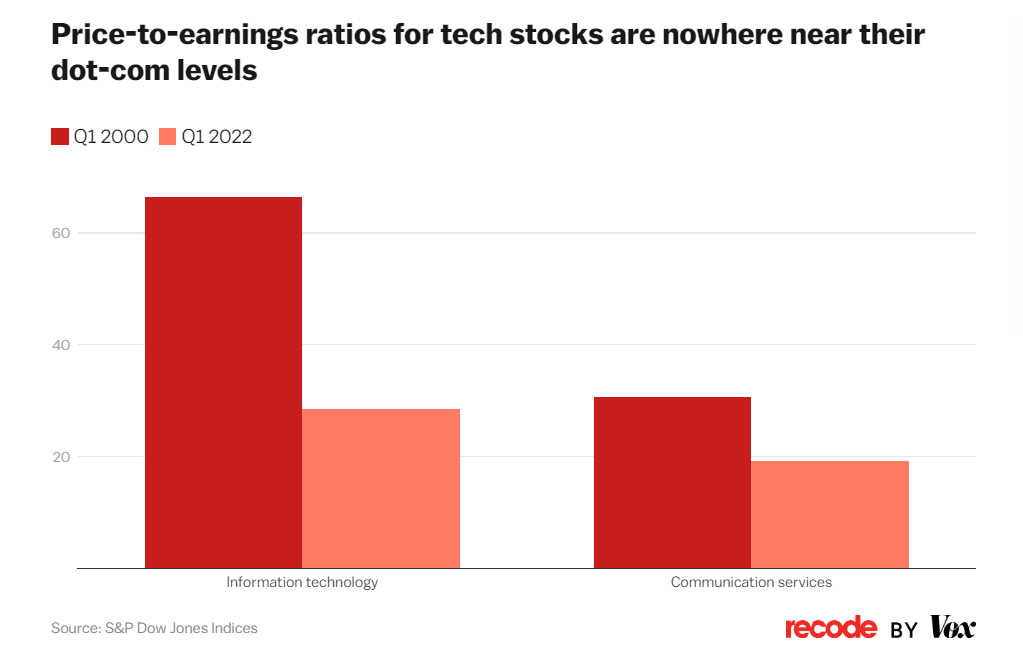

In this case, the tech bubble was actually one or two bubbles ago. Nonetheless, the “dot-com bubble” provides a convenient comparison point for TV talking heads when they comment on today’s evaporating tech stock valuations.

Here’s the key difference: In 2000, most of those fancy tech companies didn’t actually make money. Today, though, the really big fish—Apple, Amazon, Google, Facebook (Meta)—make massive amounts of money.

While one could argue that a lot of tech stocks are still overvalued, many of these companies are real businesses making real money. For example, Oracle (ORCL/NYSE) just announced this week that its quarterly adjusted earnings per share of $1.54 handily beat the expectation of $1.37 (all figures USD). Revenue of $11.84 billion topped expectations of $11.6 billion. Back in 2000, Pets.com was not looking at nearly $12 billion in revenues!

It’s also worth noting that if you’re using an indexing approach to your investment portfolio, while we might not know which company will be the next Amazon, we’re pretty sure the next Amazon will come from somewhere in the field of tech. (Actually, Amazon will probably buy the next Amazon before it goes public, thus enriching current shareholders.) Just because shares are down now doesn’t mean they always will be.

{kind=link}