From semiconductors to infant formula, U.S. consumers are facing acute shortages of essential goods. Ironically, both global and anti-global forces are behind this current disruption in supply chain. On the one hand, the shortage of infant formula reflects a highly protectionist trade regime that has led to dramatic concentration in production—only four domestic firms produce 90 percent of infant formula consumed in the U.S. On the other hand, the ongoing shortage of semiconductors highlights a similar outcome for the opposite reason: Until the recent U.S.-China trade war, decades of free trade in semiconductors have resulted in the concentration of chip production in Taiwan, South Korea, and China. While free trade has generated low prices and substantial productivity gains for consumers and workers, in both cases the concentration of industry production among a few firms in a handful of locations has exposed consumers to supply chain risks that are now coming to bear.

These hardships have pushed policymakers to consider new ways to ensure a more diverse and resilient supply chain for the most critical products, while still protecting the gains that the country receives from international trade. For semiconductors this means bringing some portion of the industry back to the U.S., which Congress is attempting to do through the CHIPS for America Act. This legislation creates a $52 billion tax credit for semiconductor equipment or manufacturing facility investments in the U.S., which intends to grow the domestic semiconductor industry on the coattails of the rising global demand for chips. Even though this funding is unlikely to be enough to make the industry competitive in leading-edge chips, it is a good start.

While tax credits may spur U.S. investment in equipment and facilities, firms still need to find thousands of workers with specialized skills to scale the industry—and they need to do so in time to compete with other countries’ efforts to do the same. Unfortunately, the long decline of the manufacturing labor force in the U.S. has eroded the country’s manufacturing base and redeveloping it could take years. But there is another possibility: Highly skilled immigrants could provide a substantial amount of this expertise immediately and could help retrain the domestic semiconductor workforce at the same time.

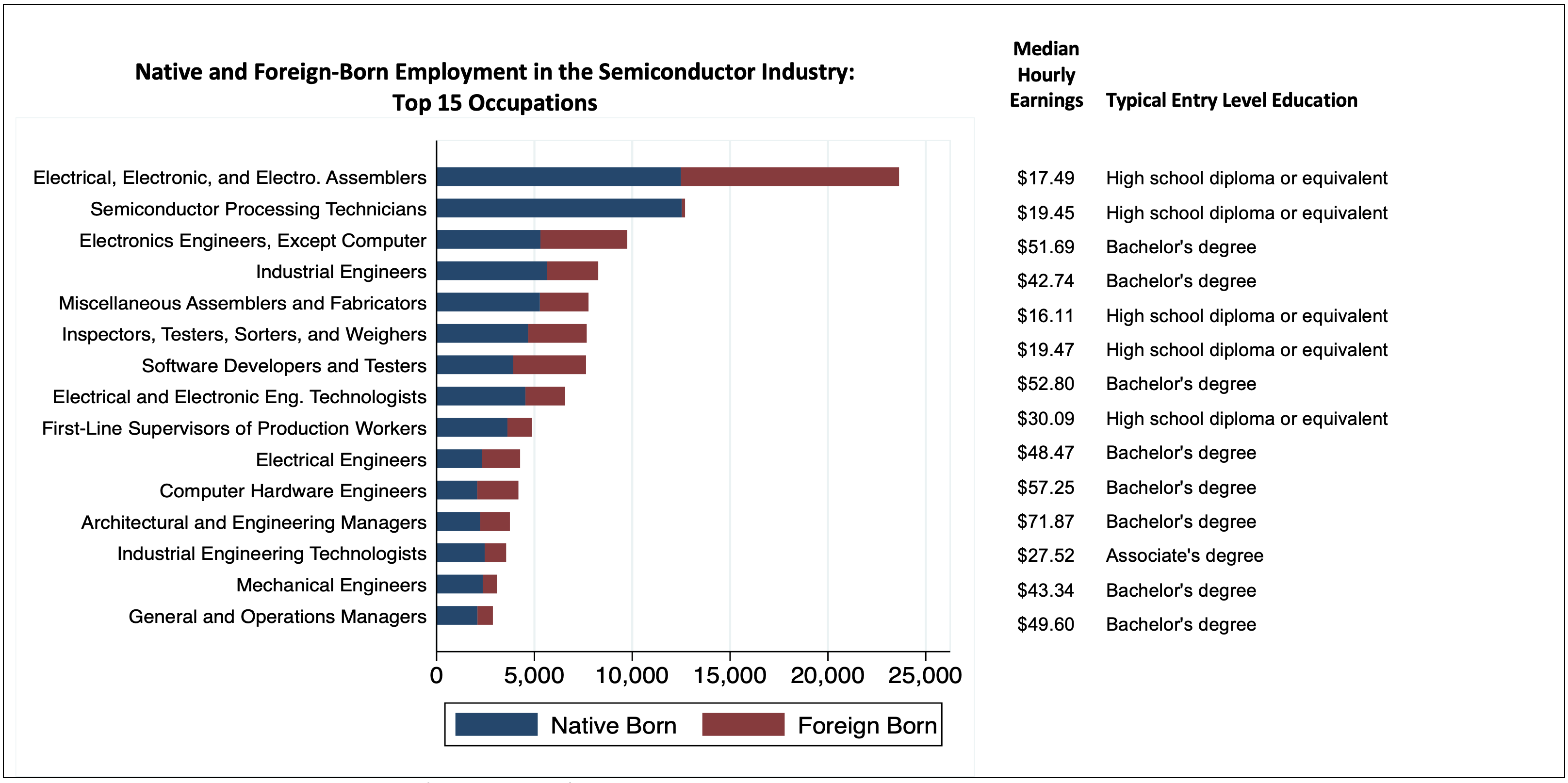

Figure 1. Immigrants already comprise a large share of talent in the semiconductor industry

Source: American Community Survey and Emsi-Burning-Glass

Source: American Community Survey and Emsi-Burning-Glass

Crucially, immigrants already constitute a large presence in nearly all the occupations in the semiconductor industry, regardless of degree levels and skill requirements (Figure 1). Electrical, Electronic, and Electromechanical Assemblers, for instance, is the largest occupation in the sector at 14 percent of the total semiconductor labor force, and requires only a high school degree. The majority of workers within this occupation are also foreign-born, coming mainly from Mexico and Central America. At the other end of the education distribution are Electronics and Electrical Engineers, the third largest occupation, which typically requires an advanced degree. Again, half of these workers are foreign-born, with India and China being the largest origin countries.

As in the past, America’s path to global competitiveness in the semiconductor industry won’t arise solely from additional funding but will also require the country to import expertise through immigration.

Doubling or tripling the size of this workforce will be challenging if current congressional ambivalence about immigration policy continues. The new jobs that do not require a college degree can potentially be filled by native-born workers, but even this will require drawing thousands of workers out of other industries in some of the tightest labor markets in the country. For instance, new semiconductor fabrication plants may be built around Dallas, Texas and Chandler, Arizona, the locations of existing Texas Instruments and Intel manufacturing facilities. However, in both locations job postings per unemployed worker—a common measure of labor market tightness—are currently among the highest in the country, indicating a shallow pool of potential employees for the semiconductor industry.

Even in Ohio, where Intel has announced a $20 billion investment to build two new plants, the share of foreign-born workers in chip-making occupations (10 percent) is double the state’s average immigrant share (5 percent). Here, immigrant workers are drawn from a diverse set of countries, with nearly equal employment shares from India, Mexico, China, and Germany.

A starting point could be to retrain manufacturing workers who have recently lost their jobs and live in the same regions that also host semiconductor facilities. Table 1 shows that occupations in many declining industries have significant skills-overlap with the top semiconductor occupations. For instance, an astonishing 11,000 Sewing Machine Operators have lost their jobs over the past decade in Texas, California, Arizona, and Oregon, and these workers have substantial skills-overlap with both Semiconductor Processing Technicians as well as Electrical, Electronic, and Electromechanical Assemblers. But even this labor pool is unlikely to be enough. A more comprehensive solution to building a competitive semiconductor workforce would combine skills-retraining programs with an expansion of the H2-B visa program to allow more temporary, nonagricultural workers into the U.S. On this front, proposed legislation has gained some recent traction, but its passage remains highly uncertain.

Table 1. Some native-born workers in declining industries have the skills to staff a resurgent semiconductor industry

Note: SPT stands for Semiconductor Processing Technicians and EEE stands for Electrical, Electronic, and Electromechanical Assemblers. The figure focuses solely on industries and occupations that are in decline and that have a large presence in California, Texas, Oregon, or Arizona.

Source: EMSI-BurningGlass and Census American Community Survey

Jobs requiring a bachelor’s or advanced degree will prove even more difficult to fill. These jobs are almost entirely engineering positions that draw from the U.S. graduate school pipeline of foreign-born talent. In this case, a likely policy solutions will focus on expansion of H1-B temporary visa caps. Such solutions however face bipartisan resistance in Congress, as members (wrongly) worry that additional immigrants would suppress the wages of native U.S. workers.

In fact, expanded immigration policy is a necessary aspect of workforce development that can also benefit existing workers. The good news is that immigration inflows are nearly back to their pre-pandemic level. The bad news is that prospective engineering students are increasingly enrolling in undergraduate and graduate programs in other countries. Here, the nonpartisan desire for a more competitive semiconductor industry collides with the partisan politics of immigration.

As in the past, America’s path to global competitiveness in the semiconductor industry won’t arise solely from additional funding but will also require the country to import expertise through immigration. Any mix of policies that does not acknowledge this is doomed to fail.

{kind=link}