Some people have

expressed surprise that UK real wages have recently fallen during a

period when the UK labour market was pretty tight. (That tight labour

market may be coming to an end as unemployment has begun to rise).

Here is the real (in terms of consumer prices) level of the monthly

average earnings data for regular pay (excluding bonuses) ending in

April this year.

Levels of this

measure are a little messed up in 2020 because of the pandemic, but

the recent fall in real wages is real enough, reflecting consumer

price inflation rising more rapidly than regular pay. In April

consumer price inflation was over 3% above the increase in regular

pay.

That real wages

should be falling even though the labour market is tight is no

surprise when we recognise that a key reason why inflation is rising

so rapidly is a huge hike in the price of energy. Higher energy

prices represent a transfer from consumers of energy to producers of

energy. Unless you can stop that transfer happening by some means

(by, for example, taxing

energy producers making unusually large profits), then

consumers have to pick up the tab.

That in turn must

mean a reduction in real consumer wages (nominal wages less consumer

price inflation). That is likely to happen because in most cases firms

set wages, and in looking at what they can afford to pay they will

not look at consumer prices, but at the prices of the products they

produce, which are rising less rapidly than consumer prices. They may

be forced to raise wages above this and productivity growth in a tight labour market, but

they have absolutely no reason to compensate workers for a rise in

energy prices. Equally, to argue that workers on average do not have

to take a real (consumer) wage cut in these circumstances is at best

wishful thinking, which is why I didn’t sign this

letter.

Does this reflect

weak union power?

But why should

workers shoulder all the higher costs of energy? What about those

living off rents or dividends, or pensioners? Well landlords and

shareholders consume energy as well, so they will pay, although as

they tend to be richer than average they will feel it less. In the

UK, however, the government has said that state pensions will be protected from higher energy

prices (with a delay) because pensions are indexed to either earnings

or consumer prices, whichever is the higher. This illustrates a more

general point, which is that the government can (and indeed should)

adjust who pays for higher energy prices among the population by

altering taxes or benefits. [1]

What would happen if

some or all workers did manage to persuade companies to keep nominal

wages at the level of consumer price inflation? Consider the case

where only some rather than all workers did this first. It is just

possible that the companies they work for would absorb higher wages

through lower profits, but the more likely outcome is that their

prices would rise by more than other firms. Consumers would pay those

higher prices, so this is another way besides government action of

redistributing the cost of higher energy among consumers. (Workers

who get a high pay rise gain, those that don’t lose.)

But belonging to a

union is not the only way some workers can transfer real income falls

due to higher energy prices to others. In terms of the current

situation it also matters how much personal bargaining power they

have, which in turn depends on how tight particular labour markets

are, how much money their employers are making or whether their

employer is the state. This last factor is particularly important at

the moment, as the following chart shows (from

here).

Currently it is

public sector workers who are really being hit by higher energy

prices, while workers in finance are (on average) getting wage rises

that are at least keeping pace with inflation. The former is untenable if we want good public services, and the government can hardly argue that bringing public sector pay in line with the private sector will be inflationary (although that probably won’t stop them trying!). The latter raises a question over why financial firms think they can afford such pay rises, and

whether recent fiscal transfers from the government to banks (e.g.)

have been wise.

Now consider what

would happen if all workers managed to emulate their comrades working

in finance? Would all workers avoid an immediate fall in real wages?

In this situation it is then even more likely that firms would raise

their prices to protect profits, producing a wage price spiral. [2]

The Bank of England would raise interest rates sufficiently high such

that unemployment rose, and aggregate demand fell, substantially,

persuading enough workers to accept lower real wages and some firms

to accept lower profits. This 1970s scenario will not happen today,

because unions are not nearly as strong now as they were then.

While the reduction

in union power since the 1970s will help avoid the kind of wage-price

spiral we saw then, it is also reasonable to suppose that a tight

labour market will have some effect on nominal wage inflation. This

in turn could lead to higher domestically generated excess inflation

(threatening the inflation targets of central banks). In addition

when inflation is high firms may find it easier to raise profit

margins. Arguments

about whether its wages or profits being too high that is risking

persistent excess inflation are not very helpful when the only

solution we currently have to reduce inflation from either source is

to reduce the aggregate demand for goods and services. [3] Equally,

arguments that generally higher wages or profits will have no

consequence for the economy are simply false. [4]

This is why in the

US and UK short term interest rates are rising. In general it is hard

trying to decide how far interest rates need to rise (and economic

activity to be correspondingly lower) to avoid a large temporary

energy price shock and temporary supply side shock (and temporary

Brexit inflationary shock in the UK) leading to permanently excess

inflation. That also means it is possible to make big mistakes,

allowing either inflation to persist or creating an unnecessary

recession. Given the mandates of most central banks, the latter is more likely than the former.

So why have real

wages grown so little over the last 15 years?

If we return to the

first chart, we can see that basic real pay is now around where it

was before the Global Financial Crisis. (Total pay, including

bonuses, would be a little higher.) Does this reflect a general shift

in GDP from labour to profits?

Here is the share of

corporate income in GDP since 1970 (source ONS).

There has been no

trend rise in the share of GDP going to profits since 1970, so rising

profits are not why real wages have grown so little over the last

decade and a half. Where there is a problem is that this steady

profit share has been accompanied by a recent slump in business

investment.

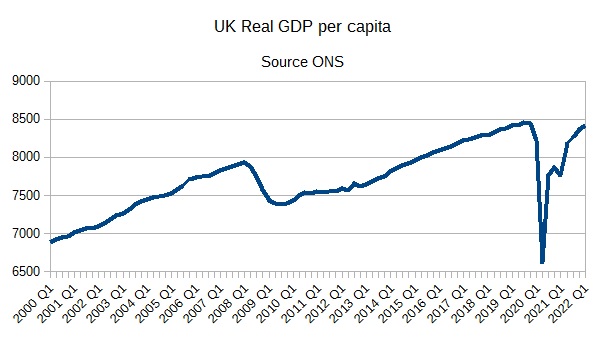

By far the most

important reason for stagnant real wages can be seen by looking at an

old favourite, real GDP per capita, over the same period as the first

chart..

You can see from

this that there just has not been much growth in national output per

head after the GFC. GDP per head was about 6% higher in the first

quarter of this year than at its pre-GFC peak, which is pretty

pathetic over a 14 year period. The UK economy has been hit by one

disaster after another: the GFC, then the austerity period that

squashed growth during what should have been the recovery period 2010-2013, a certain vote in 2016, and then Brexit and the pandemic.

Why is GDP per

capita 6% higher since the GFC compared to no growth for average real

earnings? The most obvious reason is the decline in the terms of

trade caused by higher energy prices at the end of the period, which

reduces the real wage when deflated by consumer prices but does not

reduce the amount produced in the UK to the same extent. Other

reasons include a slight fall in the share of wages in income caused

by a rise in indirect taxes (e.g. the 2010 increase in VAT). In

addition I have already noted that there is some small positive

growth in total real earnings once we include bonus payments.

The main message is

that a lack of growth in real wages over the last 15 years reflects a

lack of growth in the economy as a whole. The current cost of living

crisis is all the more painful because of this lack of real growth

over the last decade and a half. No one should be fooled by

government ministers talking about ‘a strong economy’: on this

like much else they are lying. Furthermore we know why the UK economy

has been so weak since the GFC. First austerity severely limited our

ability to recover from the GFC recession, and then Brexit has cut UK

growth and increased UK inflation.

Declinism

David Edgerton wrote

recently in the Observer about the dangers of

declinism (in short, the UK economy has suffered because of deep

longstanding and particular problems that we have never solved) and

its opposite, revivalism (from cool Britannia to Brexiter hype). Both

as generalities are nonsense, and as he points out there is a danger

of looking at the UK independently of trends in other major

economies, particularly those we trade a great deal with.

So, for example, our

economic performance after the GFC crisis was terrible because of

austerity, but austerity also happened in the US and was perhaps more

severe in the Eurozone, where it generated a second recession. As I

noted

recently, since the pandemic the US has grown more

rapidly than Europe (including the UK) in part because of a fiscal

stimulus that spurred the post-vaccine recovery.

Declinism stems in

part from not seeing the UK in an international context. Of course

the UK has many deep seated problems, but the same is true in most

other countries. This chart, from

here, can perhaps make this point more clearly than

any words.

Compared to the

original EU countries, UK growth was lower before we joined the EU,

but since we joined the EU it has at least kept pace with those

countries. I suspect this overstates the beneficial impact of joining

the EU, as the EU5 were recovering from a much lower base after WWII

and therefore could grow faster. But what it does show is that from

the 1980s onwards, for whatever reasons (and there were probably

many) the UK was actually doing rather well compared to our European

neighbours. As I noted

here, the same was true relative to the US. So stories

about some unique UK national economic decline that starts well

before 2010 are simply wrong. It is why we should not regard accounts

like this as applying to the UK alone.

But while this chart

may exaggerate the beneficial impact of EU membership, those benefits

are real enough, and what we may already be seeing since the GFC and

particularly Brexit is the beginning of another period of relative UK

decline. Italy may save us from being the sick

man of Europe once again, but if we want to see

reasonable real wage growth again we have to do something about

improving trade with our neighbours, which means getting rid of a

hard Brexit, which in turn inevitably means removing from power the

political party that delivered Brexit.

[1] It could also

shield all consumers by borrowing, transferring some of the cost of

higher energy into the future, although that would make no sense if

higher energy prices were permanent.

[2] The employment

contract is not symmetric in terms of power between employee and

employer, which is why trade unions are important in improving terms

and conditions, preventing exploitation etc. However if union

membership was widespread, the ability of unions to improve the real

wages of workers as a whole is severely constrained by the fact that

firms set prices.

[3] What about

passing laws to prevent excessive increases in profits or wages? They

were tried in the 1960s and 1970s, and they failed because they

require the state to work out, product by product or worker by worker, what reasonable

profits or wage increases are. Over the longer term it is better to

ensure excessive profits are controlled through competition

(enforced, if necessary, by breaking up monopolies) or, when

competition is impossible, through forms of regulation.

[4] If the aim is to

reduce the proportion of profits going to dividends, or share buy

backs, high nominal wage demands is a very uncertain method of

achieving this (as firms set prices). A more inevitable outcome is

widespread unemployment as the central bank attempts to control

inflation.

{kind=link}