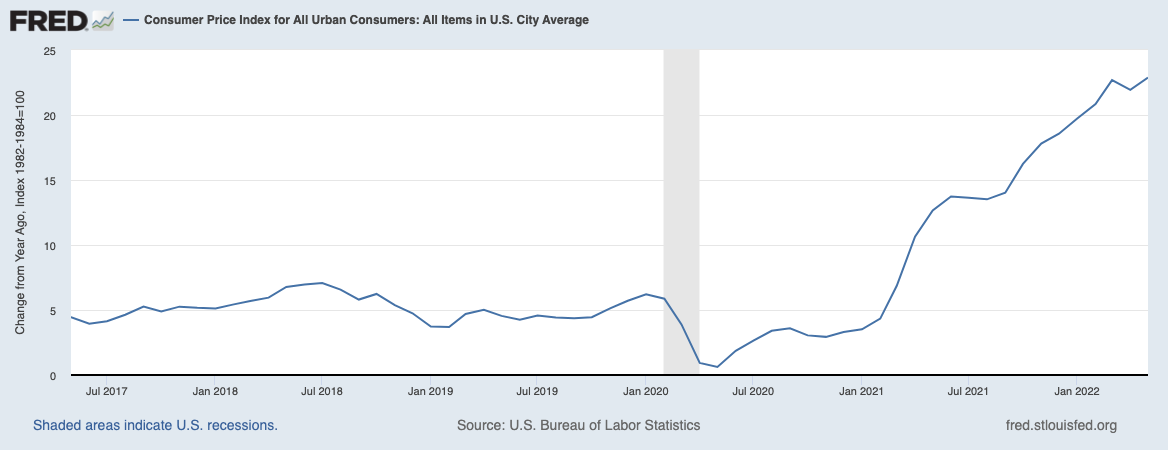

Who is to blame for the rampant inflation the United States (and the entire world) have been experiencing over the past 12 to 24 months? Which individuals and institutions can we hold accountable for the highest consumer price increases in 40 years?

A variety of people have been asking this question lately. The last time we saw an issue generating this much interest and confusion was when the country tried to understand who was to blame for the Great Financial Crisis (GFC). The approach I used in assigning blame for the 2008-09 financial crisis was based on the premise that the world is complex and ascertaining actual causation is a challenge.1 We can use the same approach to the causes of inflation.

People seem to like simple, binary answers to complex questions. Econ-Twitter will tell you “It’s the Fed’s fault; Blame Biden, no, it’s Trump’s fault.” But the world is a much more complicated place, not easily broken into clear black and white answers — at least, if you value accuracy. Over-simplified faultfinding is more suitable for ideological slogans that fit on bumper stickers than actual economic analysis.2

Prices change from moment to moment, but the factors that drive those changes can be years or even decades in the making. We tend to overlook this, caught up as we are in the here & now. The reality is many things have contributed to the current inflationary pressures.

Here are 15 or so drivers of rising prices, roughly in order. Most of the blame goes to those at the top of the list, the bottom of the list are very modest but real contributors:

Inflation Blame

1. Covid-19

2. Congress

3. President Biden CARES Act 3

4. President Trump CARES Acts 1+2

5. Consumers (overspent without regard to cost)

6. Consumers (shift to Goods)

7. Russian Invasion of Ukraine

8. Just in Time Delivery (supply chains)

9. Fed/Monetary Policy

10. Wages/Unemployment Insurance

11. Home Shortages

12. Semiconductors/Automobiles

13. Corporate Profit Seeking

14. Tax Cuts (2017) / Infrastructure (2022)

15. Crypto

Let’s delve into each of these:

Covid-19: The global pandemic – and the response by governments to the deadly and unknown pathogen – created a unique moment in history. A majority of the workforce was unable to go to their offices or workplaces. Essential workers scrambled to service 100s of millions of people stuck at home. This began a cascade of reactions that dramatically changed the structure of the economy, with lasting ramifications.

Without the pandemic, there is no massive fiscal stimulus, no WFH, and no supply chain disruption.

Fiscal Stimulus: CARES Act 1, 2, & 3 represent the single largest government response to a crisis — ever. Unprecedented in size and scope, the first CARES Act was a $2.2 trillion stimulus bill signed into law by President Trump on March 27, 2020. Next up, CARES Act II was a $900 billion extension of the original stimulus and was signed into law by President Trump on December 27, 2021. CARES Act 3 (aka The American Rescue Plan Act of 2021) was a $1.9 trillion economic stimulus bill signed into law by President Joe Biden on March. 11, 2021.3 It poured even more fuel on an already smoldering fire.

The first CARES Act legislation was the largest economic stimulus package in U.S. history at more than 10% of U.S. gross domestic product; together with parts II ($900B) and III ($1.9T), and the fiscal stimulus was ~$5 trillion. This is almost seven times the amount of the American Recovery and Reinvestment Act of 2009, the $831 billion signed into law by President Obama in February 2009 in response to the Great Financial Crisis.

All of this fiscal spending was approved by Congress – so while you can argue over the apportionment between Biden & Trump, it is Congress that controls the spending of government, and so deserves much of the blame.

Goods versus Services: The work from home (WFH) phenomena led to a shift in our consumptive habits: Fewer Services, more Goods. Out: Travel, restaurants, entertainment, vacations, elective (non-emergency) medical care. In: Everything that makes nesting, homeschooling, and WFH more tolerable, from computers and desk chairs. Home extensions and renovation led to a massive increase in demand for lumber, landscaping materials, raw building materials, appliances, and furniture.

The shortage of starter yeast revealed just how radically consumption had changed.

The pandemic lockdown moved the consumer towards goods and away from services. Pre-pandemic, consumers spent 38.7% on Goods, but a whopping 61.3% on Services. In 2020, the demand for Goods rose 20% globally, but production increases were barely 5%. Prices rose accordingly.

As an economy, we suddenly began buying food via Instacart/Amazon/Target/Walmart instead of going out to eat; we bought Peletons vs. a gym membership; we purchased large screen TVs instead of going to the movies; we bought cars and Winnebagos instead of going on vacation. Perhaps it’s a good sign that used Pelotons can be found on eBay for a fraction of what they cost new.

Russian Invasion of Ukraine: Foods and energy prices were already elevated pre-invasion, but Putin supercharged their prices. Until this war ends, energy prices will likely remain elevated as will grain and other foodstuffs.

Consumers: People driving during rush hour complain about being “stuck in traffic.” They are not stuck in traffic, they are traffic. A similar paradigm applies to inflation: Consumers who continue to buy Homes and Cars despite substantial price increases are not suffering from inflation, they are (in part) a driver of inflation.

Think about the purchases of homes or used cars, despite price increases that range from substantial to outright ridiculous. When you buy a good, despite big increases, demand can be described as “inelastic.” So you (over)pay an inflated price in order to get the necessitated item. It may feel like you’re suffering from inflation but (just as in traffic) but recognize you are also a source of inflation.

Just in Time Delivery/ Inventory shortfall: In the relentless effort to become more efficient and profitable, warehousing inventory became anathema to corporate managers. This dramatically reduced inventory costs but required logistics and supply chains to be incredibly robust. As it turns out, they were not.

Semiconductors (Autos): Reopening a temporarily closed chip fab is a complicated expensive process. In 2021, the shortage of New and Used Cars was among the largest contributors to price increases.

Housing: We underestimated demand for single-family homes, and then underbuilt them for a decade. Suddenly lots of people wanted one. The large price increases on admittedly smaller volumes are the result.

The Eviction Moratorium also plays into this; the unintended consequences may be that landlords are raising apartment rents in order to catch up on lost revenues from nonpaying renters from 2020-21.

For some context, BLS reports that in 2021, on the days they worked, 38% of employed persons did some or all of their work at home; 68% did some or all of their work at their workplace. Compare that to the pre-COVID-19 pandemic era on 2019: Workers were less likely to work at home (24%) and much more likely to work at their workplace (82%).

Wages: For the past 4 decades, the bottom half of the wage scale lagged dramatically. The minimum wage contributed to Deflation. But nothing is forever, and the circumstances of that power dynamic have turned. Workers,especially the bottom half of paid employees, seem to have gained the upper hand. (We discussed this in April of 2021).

Unemployment Insurance: When you give Americans $1.4 trillion in Unemployment, they tend to not want to work for $8 or $10 an hour. And, they form new businesses in record numbers.

Fed/Monetary Policy: ZIRP QE did nothing for inflation for a decade-plus, so it’s hard to have them at the top of the list. (I know this back of the list placement will infuriate Fed haters, but I am aiming for accuracy). But once the fiscal stimulus kicked in, the Fed was somewhat behind the curve. At the very least, thru should have been normalizing rates back in 2021.

Tax Cuts / Infrastructure: For the sake of completeness, I am including the Tax Cuts and Jobs Act (TCJA) ($1.1 trillion, annually, from 2018 forward) and the 2022 Infrastructure bill (minimum $1.1 trillion over 10 years). I do not believe these are big contributors to the current bout of rising prices, but it’s just that much more fiscal fuel for the fire.

Corporate Profit Seeking: I am not in the camp that seeks to place blame on rising prices in companies seeking to increase their revenue and profits. However, as a consumer of goods, one cannot help but notice substantial price increases in items that have very little to do with input costs, supply chain snafus, or semiconductor production shortfalls. While transportation costs affect all goods, some of the price rises we’ve seen are simply people taking advantage of inflation to raise their own prices.

You can’t have a capitalist system where companies, shareholders and their management are rewarded for profitability and not end up with some dubious behavior/profiteering on the margins. But I doubt it adds up to very much, best guess maybe 5-10% of the increases (if anyone has data showing more, I’d be curious to see it).

Crypto: Why is crypto on this list? 4 Because massive gains led to a series of big spends – from $100 million mansions as Hedge funds and VCs cashed in; but do not ignore the starter homes, where Redfin found “11.6% of people buying homes for the first time said that selling investments in cryptocurrency had helped them save for a down payment.”

Lamborghinis have been sold out for 2 years, and (anecdotally) crypto profits are driving at least some of that. Some of the larger dealerships are accepting crypto as a form of payment.

~~~

The world is complex, but the human mind seems to prefer simplicity, even at the expense of accuracy. As much as we want to point a finger at a single person – whether it’s for partisan reasons or simply as a way of expressing our angst – this is simply not how economies in the real world actually work.

The truth is we have many factors leading to higher prices – and some of them are showing signs of peaking…

Previously:

Goods Versus Services (June 3, 2022)

Normalization vs Inflation (March 14, 2022)

$1.395 Trillion Peak Unemployment Insurance (March 4, 2022)

Structural or Transitory? (November 23, 2021)

How Everybody Miscalculated Housing Demand (July 29, 2021)

Elvis (Your Waiter) Has Left the Building (July 9, 2021)

The Inflation Reset (June 1, 2021)

Shifting Balance of Power? (April 16, 2021)

Who is to Blame, 1-25 (June 29, 2009)

_____________

1. That approach eventually led to the book Bailout Nation.

2. I considered the causation question in the aftermath of the financial crisis, and found numerous people and institutions to blame. Fed Reserve Chairman Alan Greenspan was top of the list, the Federal Reserve’s monetary policy was #2, and the Fed (again) as bank regulator was #11. I originally titled that chapter of Bailout Nation Blame 1-25 but ended up with a list of 33 but could easily have made it 50.

3. The Tax Cuts and Jobs Act of 2017 was signed into law by President Trump on December 22, 2017 and put ~$1.125 trillion into the economy 2 years before the pandemic.

4. I left out very tenuous to demonstrate players, such as the anti-vaxxers, who delayed the reopening of the economy, and Facebook/Twitter and other social media, who spread their misinformation. Crypto is here due to housing and cars, but I put it at the bottom of my list. At a certain point, the impact of modest factors attenuates rapidly.

{kind=link}