NAHB analysis of the Census Bureau’s quarterly state and local tax data shows that $672.9 billion in taxes were paid by property owners in the four quarters ending Q1 2022 (not seasonally adjusted), a 0.1% quarterly increase.[1] State and local governments collected $1.9 trillion over the same period, the largest amount on record (nominal and real) and 16.0% more than the four-quarters ending Q1 2021.

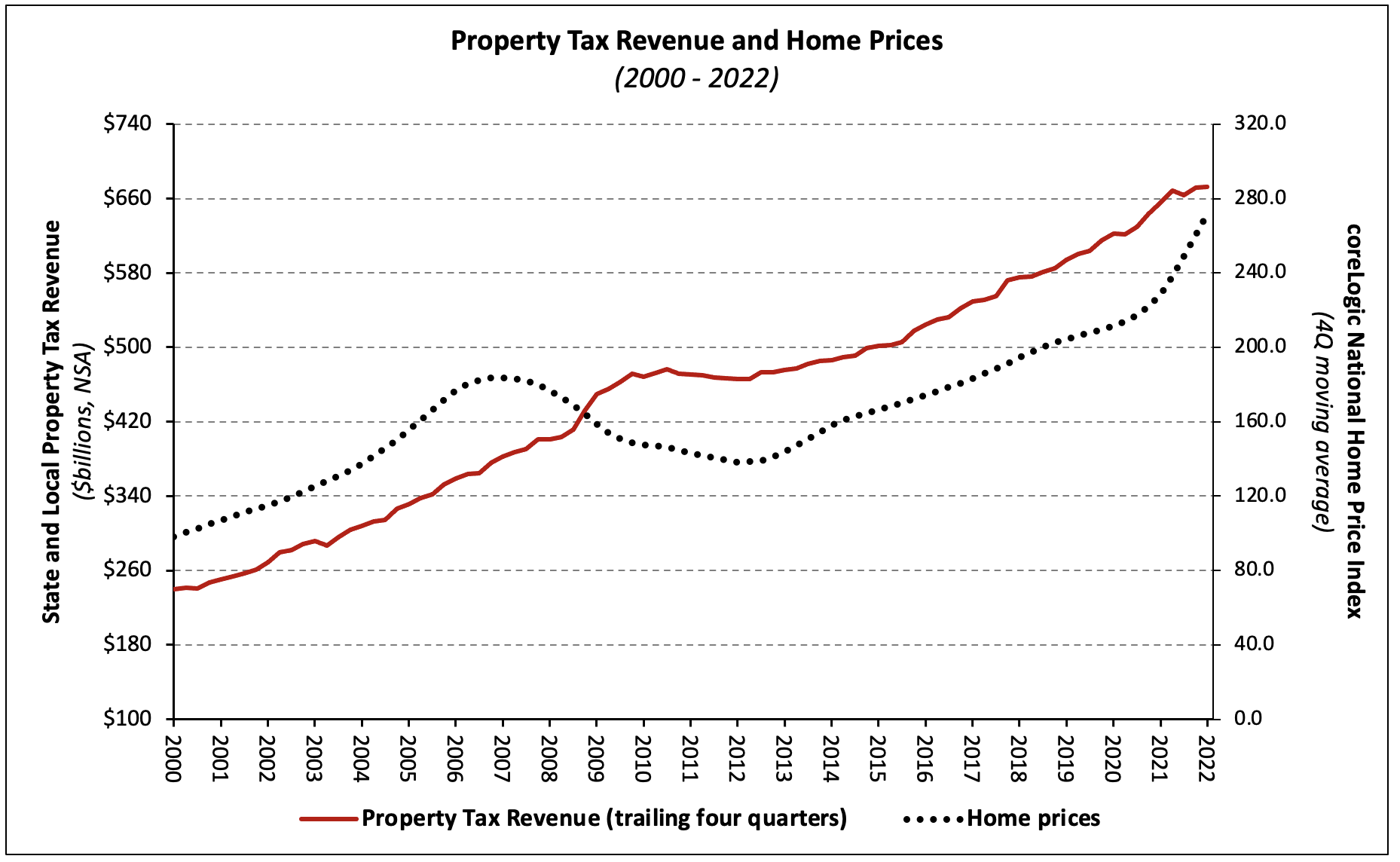

As governments’ assessments and adjustments of property values lag home prices so, too do property tax collections. This lag—which has historically been between two and three years—is due to two primary factors: 1) the frequency at which governments assess property values for tax purposes varies by state and municipality, and 2) some localities only reassess property values to market value when the property is sold or transferred.

Property taxes accounted for 35.0% of state and local tax receipts, a 1.2 percentage point decrease over the prior quarter. In terms of the share of total receipts, property taxes were followed by individual income taxes (30.8%), sales taxes (27.3%), and corporate taxes (6.9%).

The ratio of property tax revenue to total tax revenue from the four sources has been below its pre-housing boom average of 37% for the past four quarters. Quarterly corporate income tax revenues increased as a share of the total, accounting for 6.9% of state and local tax receipts (NSA), up from 6.2%.

Year-over-year growth of four-quarter property tax revenue has decelerated each of the past three quarters after accelerating each quarter from Q3 2020 to Q2 2021. Four-quarter corporate income tax, individual income tax, and sales tax revenue increased 74.5%, 21.7%, and 19.2%, respectively, year-over-year.

The share of property tax receipts among the four major tax revenue sources naturally changes with fluctuations in non-property tax collections. Non-property tax receipts including individual income, corporate income, and sales tax revenues, by nature, are much more sensitive to fluctuations in the business cycle and the accompanying changes in consumer spending (affecting sales tax revenues) and job availability (affecting aggregate income). In contrast, property tax collections have proven relatively stable, reflecting the long-run stability of tangible property values as well as the aforementioned effects of lagging assessments and annual adjustments.

[1] Census data for property tax collections include taxes paid for all real estate assets (as well as personal property), including owner-occupied homes, rental housing, commercial real estate, and agriculture. Owner-occupied and rental housing units combine to make housing’s share the largest among these subgroups.

Related

{kind=link}