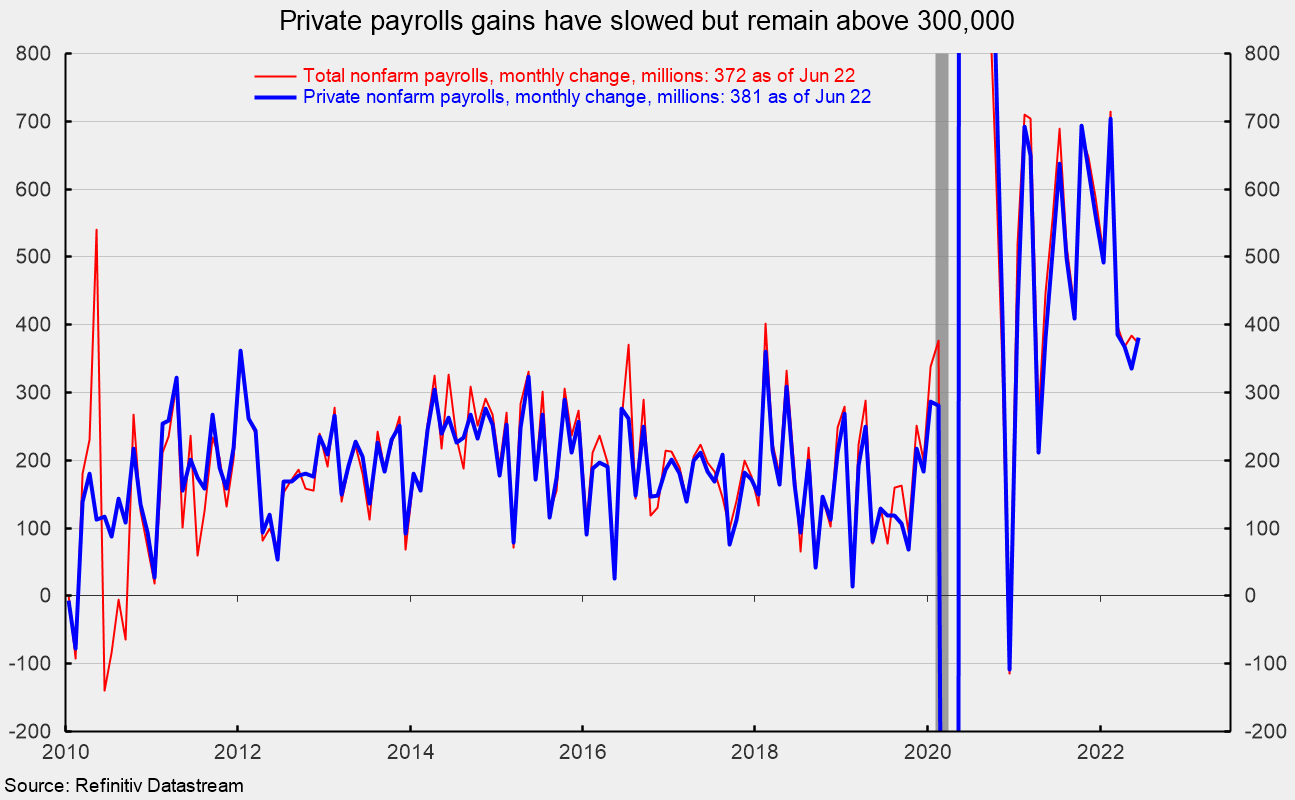

U.S. nonfarm payrolls added 372,000 jobs in June. While that result would be considered very strong by longer-term historical comparison, it is on the lower end of recent gains (see first chart). The average monthly gain from 2010 through 2019 was 183,000 while the average monthly gain over the last twelve months is 524,000.

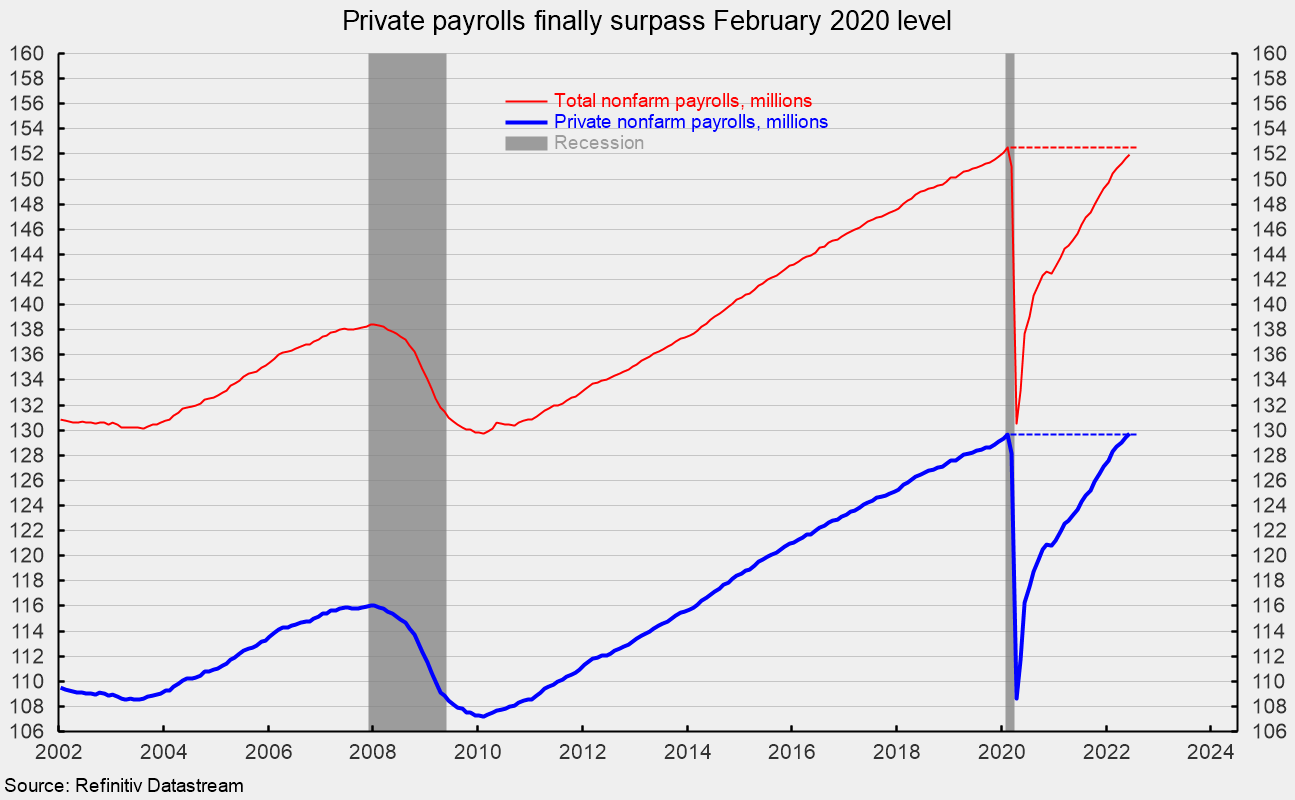

Private payrolls posted a 381,000 gain in June (see first chart). The average monthly gain from 2010 through 2019 was 181,000 while the average monthly gain over the last twelve months is 508,000. Total nonfarm payrolls are 0.3 percent below their February 2020 levels while private payrolls have finally surpassed the February 2020 peak (see second chart).

Gains in recent months have generally been broad-based. Within the 381,000 gain in private payrolls, private services added 333,000 versus a 12-month average of 436,000 while goods-producing industries added 48,000 versus a 12-month average of 71,700.

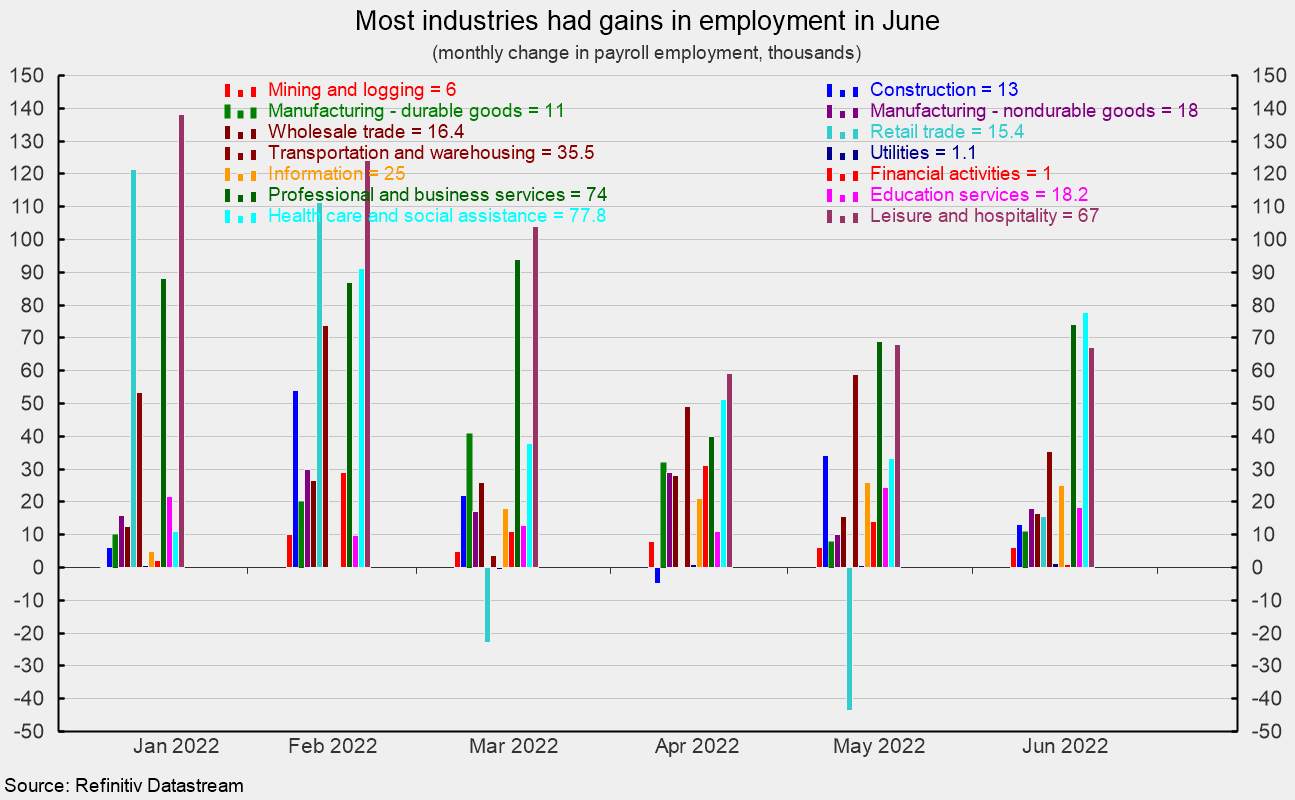

Within private service-producing industries, education and health services increased by 96,000 (versus a 58,300 twelve-month average), business and professional services added 74,000 (versus 99,100), leisure and hospitality added 67,000 (versus 134,300), transportation and warehousing added 35,500 jobs (versus an average 41,000), information services gained 25,000 (versus 15,700), wholesale trade gained 16,400 (versus 16,600), and retail employment rose by 15,400 (versus 32,900; see third chart).

Within the 48,000 gain in goods-producing industries, nondurable-goods manufacturing added 18,000, construction added 13,000, durable-goods manufacturing increased by 11,000, and mining and logging industries increased by 6,000 (see third chart).

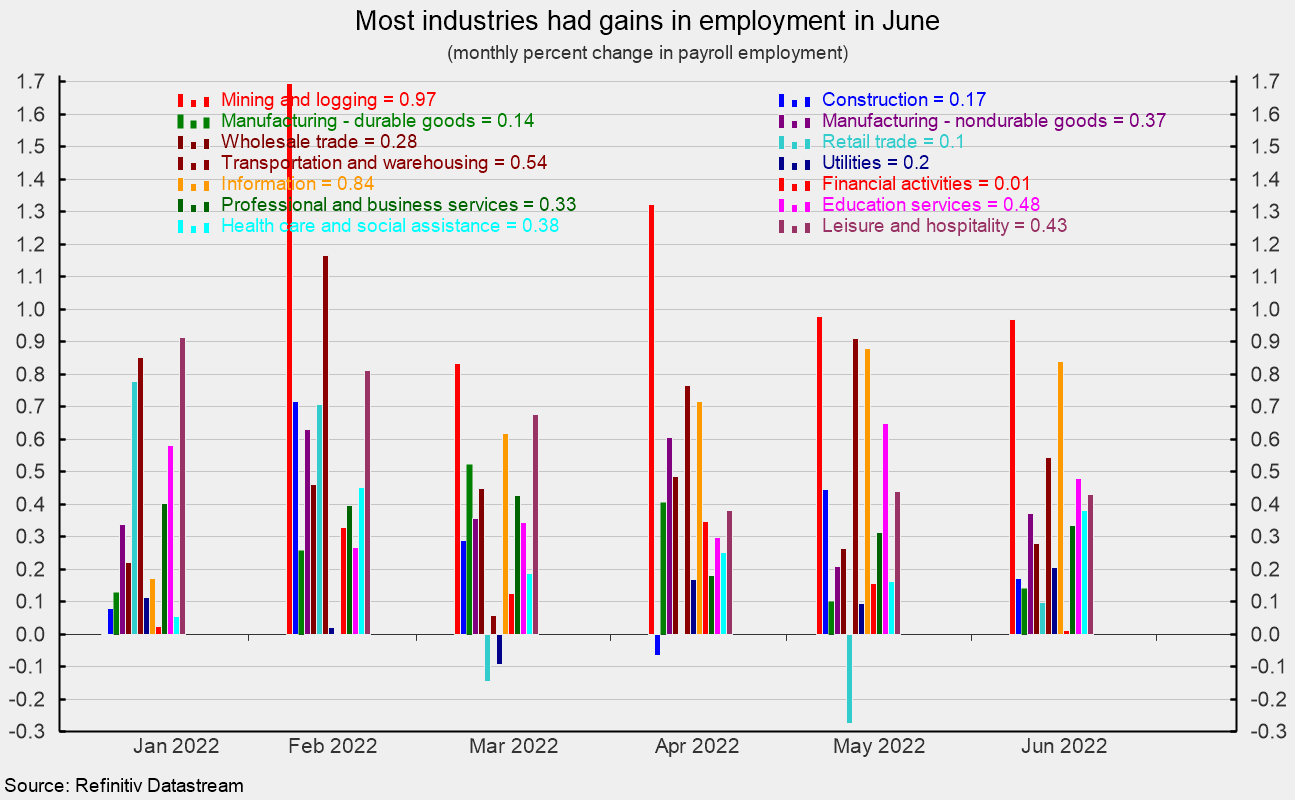

While actual monthly private payroll gains are dominated by a few of the services industries, monthly percent changes paint a slightly different picture. Mining and logging industries, information services, and transportation and warehousing have been posting strong monthly percentage gains recently (see fourth chart).

Average hourly earnings rose 0.3 percent in June, putting the 12-month gain at 5.1 percent. The average hourly earnings for production and nonsupervisory workers rose 0.5 percent for the month and are up 6.4 percent from a year ago. The average workweek for all workers was unchanged at 34.5 hours in June while the average workweek for production and nonsupervisory held at 34.0 hours.

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls for all workers gained 0.6 percent in June and is up 9.4 percent from a year ago; the index for production and nonsupervisory workers rose 0.8 percent and is 10.7 percent above the year ago level.

The total number of officially unemployed was 5.912 million in June, a drop of 38,000. The unemployment rate was unchanged at 3.6 percent while the underemployed rate, referred to as the U-6 rate, fell 0.4 percentage points to 6.7 percent in June. In February 2020, the unemployment rate was 3.5 percent while the underemployment rate was 7.0 percent.

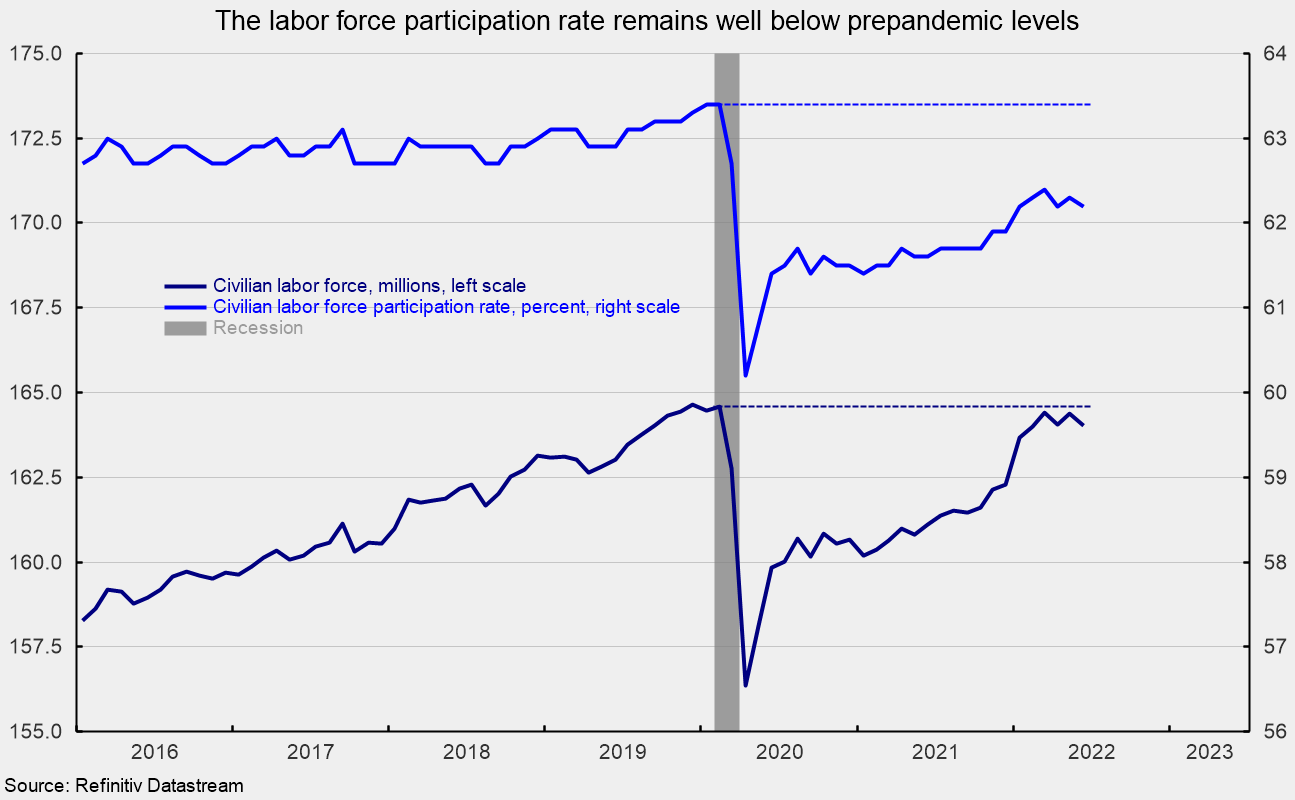

The employment-to-population ratio, one of AIER’s Roughly Coincident indicators, came in at 59.9 percent for June, down 0.2 percentage points and still significantly below the 61.2 percent in February 2020. The labor force participation rate ticked down 0.1 percentage point in June, falling to 62.2 percent, but still well below the 63.4 percent of February 2020 (see fifth chart). The total labor force came in at 164.0 million, down 353,000 from the prior month and more than half a million below the February 2020 level of 164.6 million (see fifth chart).

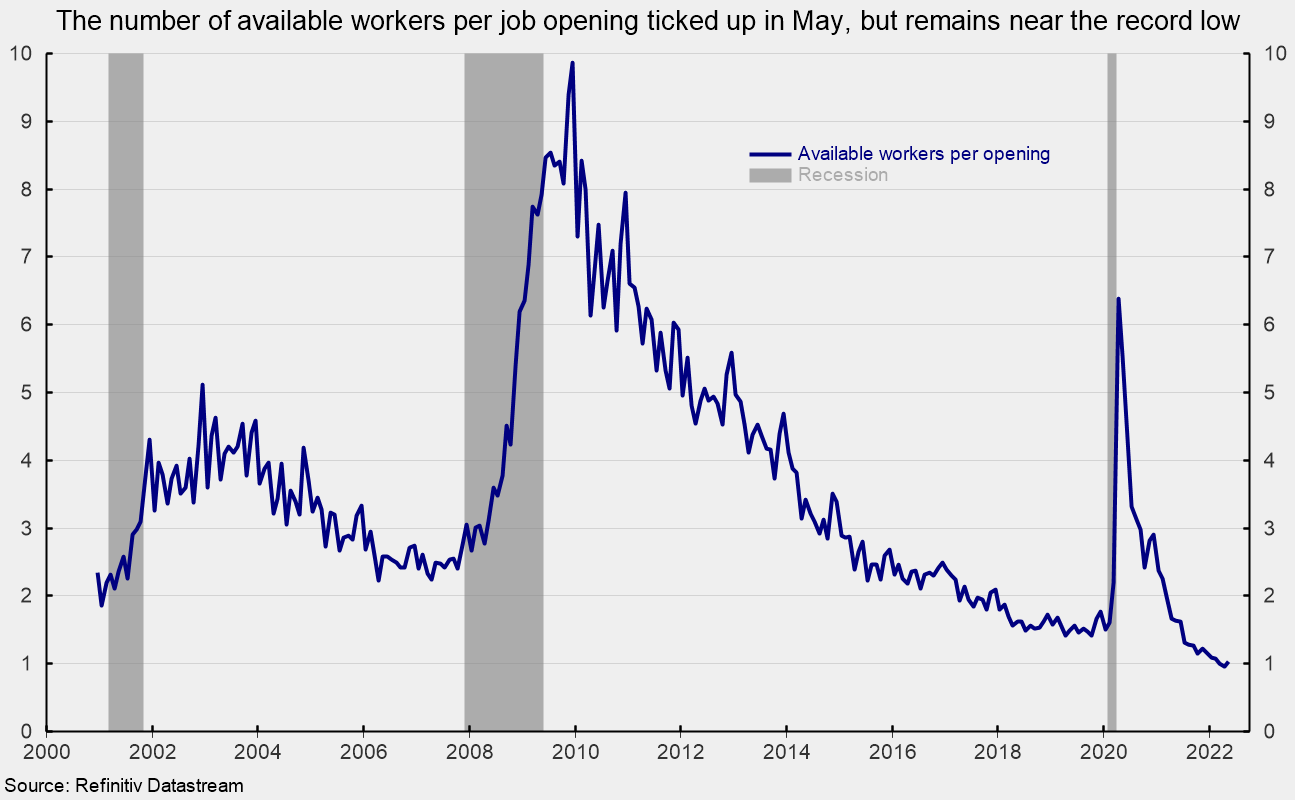

The weaker participation rate is one reason the labor market remains so tight. Based on the latest Job Openings and Labor Turnover Survey (JOLTS), there is 1.034 available workers for each opening, up just slightly from the record low of 0.957 in April (see sixth chart). The JOLTS report did show that the total number of private-sector job openings and the number of private-sector quits eased back in April and May, suggesting there may be some easing in labor conditions.

The June jobs report shows total nonfarm and private payrolls posted strong, albeit somewhat slower, gains. The somewhat slower gains are consistent with the upward trend in weekly initial claims for unemployment insurance, and the slightly lower number of job openings and quits in May. Less confidence in the labor market may lead to a consumer spending retrenchment. Persistently elevated rates of price rise are also harming consumer attitudes and may be starting to impact spending patterns as well. Furthermore, an intensifying cycle of Fed policy tightening is increasing borrowing costs for consumers and businesses alike. At the same time, fallout from the Russian invasion of Ukraine continues to disrupt global supply chains. The outlook remains highly uncertain, and caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}