A big debt crisis is brewing in the Global South. The IMF had sounded alarm over growing debt sustainability problems in many low-income countries already prior to the coronavirus crisis. More than two years into the pandemic, the debt situation has deteriorated significantly. According to the IMF, 60 percent of low-income countries are now at high risk of or already in debt distress. Moreover, a growing number of middle-income countries is also suffering from high debt service burdens. The number of emerging markets with sovereign debt that trades at distressed levels—with yields more than 10 percentage points above those on similar maturity U.S. Treasuries—has more than doubled in the past six months. Monetary tightening in the U.S. and other advanced economies is driving up the cost of debt and making international refinancing ever harder for those countries that still maintain access to international capital markets. The composition of financing is continuing to evolve toward new, more expensive sources.

The Russian invasion of Ukraine has further escalated the situation, creating a perfect storm. The war has sent shockwaves through the global economy and caused the largest commodity shock since the 1970s. Whereas oil, gas, and grain exporters may get temporary relief in the short term, many developing and emerging market countries—including in sub-Saharan Africa—are net fossil fuel and grain importers. The effects of the war in Ukraine are likely to significantly worsen the social and economic situation in many developing and emerging market countries, further undermining debt sustainability.

High levels of public debt service and insufficient fiscal and monetary space have already constrained the crisis responses of most low and middle-income economies. While advanced countries were able to implement extremely expansionary fiscal and monetary policies in response to the pandemic crisis, few countries in the Global South had this option.

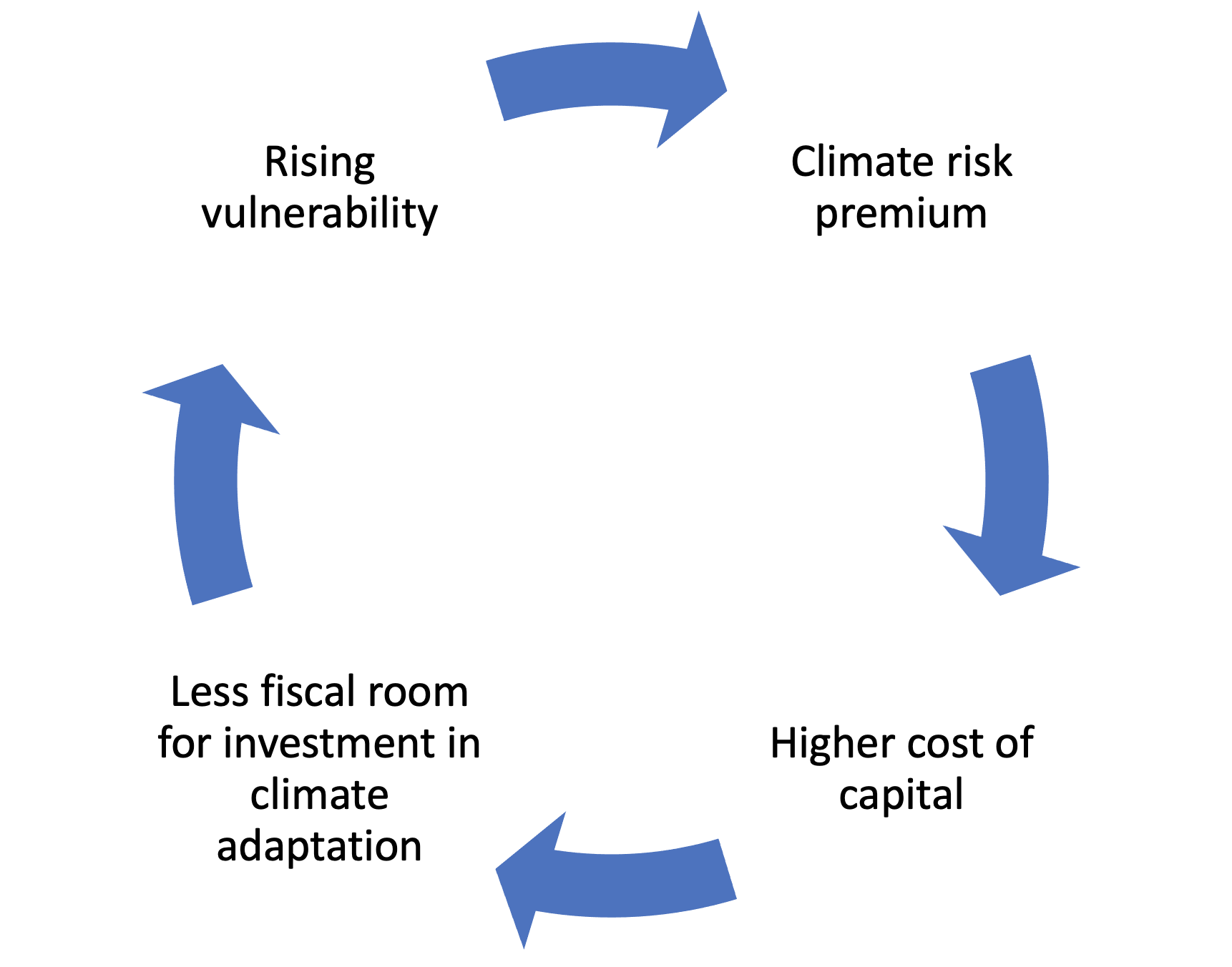

The precarious debt situation has not only been threatening recoveries. It has also impeded much-needed investments in climate resilience. These investments are indispensable and urgent: Governments must climate-proof their economies and public finances or face an ever-worsening spiral of climate vulnerability and unsustainable debt burdens. In several empirical studies that were replicated by the IMF and others, we showed that physical climate vulnerability is driving up the cost of capital of climate-vulnerable developing countries. As financial markets increasingly price climate risks, and global warming accelerates, the risk premia of these countries, which are already high, are likely to increase further. There is a danger that vulnerable developing countries will enter a vicious circle in which greater climate vulnerability raises the cost of debt and diminishes the fiscal space for investment in climate resilience.

Figure 1. The vicious circle of climate vulnerability and the cost of capital

Source: Volz, “Climate Change and the Cost of capital in Developing Countries”, Presentation at the Understanding Risk Finance Pacific Forum organized by the Government of Vanuatu and the World Bank Group’s Disaster Risk Financing and Insurance Program in Port Vila from 16-19 October 2018.

The impact of COVID-19 on public finances risks reinforcing this vicious circle. In many countries, including many Small Island Developing States, high public debt service is crowding out critical investment that is needed for climate-proofing economies and enabling a green, resilient, and equitable recovery. With the impacts of the climate crisis becoming evermore damaging economically, there is a great urgency to address sovereign debt problems head-on and put countries in a position to not only respond to short term needs posed by the pandemic and the engulfing food price crisis, but also invest in much-needed climate resilience.

There is a danger that vulnerable developing countries will enter a vicious circle in which greater climate vulnerability raises the cost of debt and diminishes the fiscal space for investment in climate resilience.

In 2020 we put forward a proposal for Debt Relief for a Green and Inclusive Recovery as an ambitious, concerted, and comprehensive debt relief initiative that frees up resources to support recoveries in a sustainable way and allow governments to invest in strategic areas of development, including climate-resilient infrastructure, health, education, digitization, and cheap and sustainable energy. A key tenet of this proposal is that debt relief should not only provide temporary breathing space. It should empower governments to lay the foundations for sustainable, climate-resilient development. As part of our proposal, debtor countries that receive debt relief would commit to reforms that align their policies and budgets with Agenda 2030 and the Paris Agreement. The country commitments would be designed by country governments under the involvement of the parliaments and in consultation with the relevant stakeholders.

Ahead of the 2021 United Nations Climate Change Conference in Glasgow, the V20 Finance Ministers—which represent 55 climate-vulnerable nations with a total population of 1.4 billion people—issued a Statement on Debt Restructuring for Climate-Vulnerable Nations, drawing on our proposal. In the statement, the V20 Finance Ministers called for “a major debt restructuring initiative for countries overburdened by debt—a sort of grand-scale climate-debt swap where the debts and debt servicing of developing countries are reduced on the basis of their own plans to achieve climate resilience and prosperity”.

With the debt and climate crises escalating, it is time that these calls are heard. The Common Framework for Debt Treatment that the G20 established in November 2020 to address insolvency and protracted liquidity problems has not delivered. Not only does it exclude middle income countries, it also lacks incentives and mechanisms to bring debtor governments and private creditors together. As pointed out by the World Bank, “[t]he lack of measures to encourage private sector participation may limit the effectiveness of any negotiated agreement and raises the risk of a migration of private sector debt to official creditors.”

To incentivize participation of private creditors—which hold more than 60 percent of all debt claims on countries in the Global South—in debt restructurings, a combination of positive incentives (“carrots”) and pressure (“sticks”) is needed. In terms of incentives, we propose the creation of a new Guarantee Facility for Green and Inclusive Recovery that is designed to entice the commercial sector to engage in debt restructurings. The facility, which could be established relatively quickly at the World Bank, would back the payments of newly issued sovereign bonds that would be swapped with a significant “haircut” for old, unsustainable, and privately held debt. Private creditors would benefit from a partial guarantee of the principal, as well as a guarantee on 18 months’ worth of interest payments, analogous to the Brady Plan that helped to overcome the stalemate of debt crisis of the 1980s.

In terms of pressure, the financial authorities of the jurisdictions in which the major private creditors (both banks and asset managers) reside and that govern the majority of sovereign debt contracts—most importantly the United States, the United Kingdom, and China—could use strong moral suasion and regulations on accounting, banking supervision, and taxation to improve creditors’ willingness to participate in debt restructuring.

Economic history teaches us that delaying the resolution of debt distress is very costly for debtor countries. In the absence of an appropriate international sovereign debt restructuring mechanism, creditors and borrowers alike keep kicking the can down the road. This has been a long-standing problem that has time and again caused lost decades of development and avoidable human suffering. What is making things worse now is that the stakes are even higher in the face of an evolving climate crisis.

The international community—especially the major advanced economies and China—needs to overcome the current deadlock and work toward a solution of the debt crisis that will enable all countries to respond to the multiple crises confronting them. The consequences will be dire if they fail to do so.

{kind=link}