There are three basic questions when it comes to credit: What is a good credit score? Why do I need one? And how do I get one? It’s no secret that we don’t love debt here at YNAB, however, we recognize that credit can be a useful tool when used carefully.

But instead of just writing “carefully” at the end of the sentence, we want to spray paint it in big red letters, we want to hire a skywriter to emblazon the sky with ‘carefully’ in a cloudy cursive font, we want to follow you around all day chanting it into a bullhorn while beating on a drum.

This will have to do, though.

The reality is that debt can be necessary to achieve dreams like buying a house or going to college. The flip side of that reality is that debt can be insidious; it can pose as an invitation to live a life you can’t afford and it can rob you of future opportunity. It seems manageable at first—and therein lies the danger!

Use it Carefully, with a capital C.

Now that we’ve covered all of that, let’s learn what’s a good credit score and how you can get one.

What is a Good Credit Score?

A credit score is a three digit number calculated by credit bureaus using information like your payment history, the amount of debt you carry, and your length of credit history.

What’s considered “good” may depending on the credit scoring model (the two most commonly used are FICO and VantageScore), but here’s a general idea of where different credit score ranges fall on a scale of fair to excellent:

| 300-579 | Poor |

| 580-669 | Fair |

| 670-739 | Good |

| 740-799 | Very Good |

| 800 and up | Excellent |

Why Does Good Credit Matter?

Your credit score is an indicator of your creditworthiness, and is used by creditors and lenders to make lending decisions about your application for a credit card or loan. It also helps determine what terms, credit limit, and interest rates you qualify for—a better score means that you’re a lower risk, so you’ll pay less as a borrower.

Good credit health can also be the deciding factor when it comes to:

- Getting approved to lease an apartment

- How much your landlord requires for your security deposit

- If you’ll need to provide a security deposit to your utility company (and how much)

- If you’re eligible for car insurance and what your rate will be

- If you can get approved for a mortgage, and if so, for how much and at what rate.

Adult life is a lot easier (and less expensive) when you have good credit.

How is Your Credit Score Calculated?

FICO and VantageScore both generate your score based on information from Equifax, TransUnion and Experian credit reports or, in other words, your credit activity. Don’t be surprised if your scores from these credit reporting agencies don’t match. Rob Kaufman, at FICO, explains, “Due to the fact that the agencies may receive different creditor information at different times (or not at all), you might not have the same FICO Scores at each agency.”

Your credit score is generally calculated based on the following factors:

1. Payment History

Your payment history—including on-time payments, late payments, bankruptcies and related items—is the biggest factor in calculating your credit score.

2. Amount Owed

Credit utilization is the amount of debt you have and how it’s distributed. For a better score, keep your revolving balances low, and pay down any installment debt.

3. Age of Credit History

Next up is the age of your credit. The longer your credit history is, the more it helps your score so avoid closing out older accounts in good standing, if you can help it.

4. Credit Behavior

Applying for or opening new lines of credit can have a negative impact on your credit score, so avoid behavior that may result in a hard inquiry on your credit report if you’ll be applying for an auto loan or mortgage in the near future.

5. Mix of Accounts Types

What kind—and how many types—of credit you have also impacts your credit score. Types of credit include mortgages, installment loans, retail accounts, credit cards and finance company accounts. Keep in mind that if you don’t have a lot of credit activity or history, your mix of accounts will more heavily affect your score.

How to Get Good Credit

The best way to get good credit is to be careful, strategic, and thoughtful as you begin to build your credit history, but if you got off to a rocky start, it’s never too late to clean things up and improve your score. Here are our top tips for increasing your credit score:

Stick to a Budget

The safest way to use credit is to treat it like a payment source vs. a borrowing tool—meaning don’t spend what you don’t have. Creating (and following) a budget helps make sure your spending aligns with your priorities because you make intentional decisions about where you want your money to go.

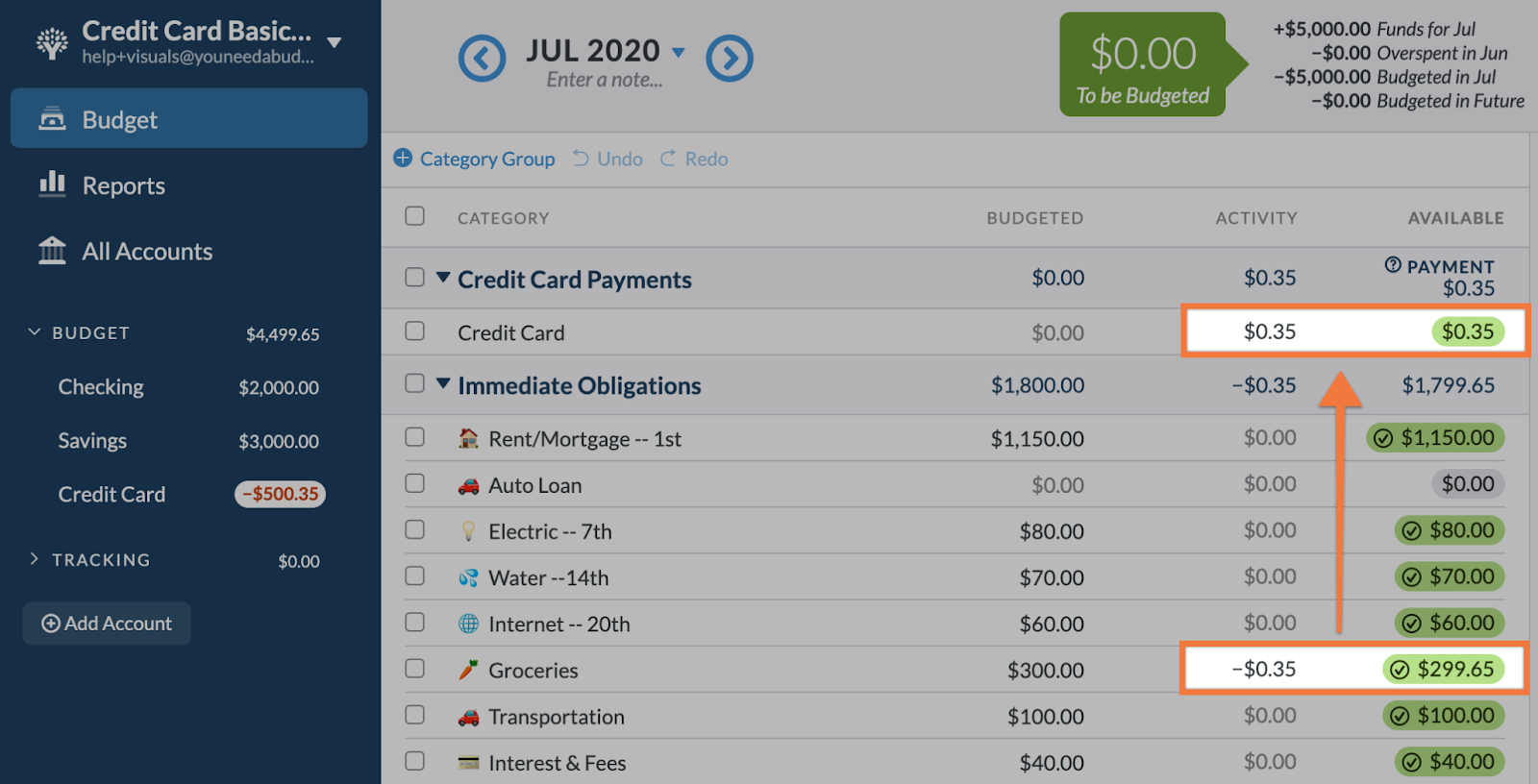

YNAB’s budgeting app makes it easy not to slip into debt accidentally. You assign the money that you already have into different budgeting categories. When you spend money, you enter a transaction, identify which budget category the spending comes from, and select how you paid—if you paid with a credit card, the software automatically moves the amount from your budget category to the category for your credit card payment.

When it’s time to make your credit card payment, all of the money you need to cover your purchases has already been set aside in that category. Voila! No debt or interest!

In the image above, someone bought gum with a credit card at the grocery store. The $.35 cost was deducted from the Groceries category and added to the Credit Card payment category to cover the cost. Learn more about how credit cards work in YNAB

Pay Your Bills on Time

Payment history is the most significant factor in credit score calculations, so it’s critical to pay your bills on time, every time. This is true for more than just credit cards and loans—any debt that goes into collections will negatively impact your credit score. If you’re having difficulty making a payment, call the creditor and ask for guidance on what to do.

Keep Balances Low

Here at YNAB, we’d love to see your balances paid in full each month because it would mean you’re avoiding debt and not wasting money on interest payments. If that’s not possible, a good rule of thumb is to keep your balances below 30% of your total available credit. If you’re already in debt, YNAB’s Loan Planner can help you come up with a plan to pay it off.

Avoid Applying for New Credit

Before you apply for any type of loan or credit, ask yourself if you really need this. And then ask yourself again. Is there any way you could save up the cash instead? Find a cheaper alternative? Live without it for a while? Applying for loans or credit will show up on your credit report as a hard inquiry, which will have a negative impact on your score.

Monitor Your Credit Report

Check your credit report on a regular basis so that you’ll have a full awareness of your credit situation and so that you can dispute any inaccuracies. You can request a free copy of your credit report from all three credit bureaus every 12 months at www.annualcreditreport.com. Requesting one from each bureau every four months allows you to keep an eye on your credit all year round.

What is a Good Credit Score and How Do I Get One?

So, to summarize, the answer to “What is a good credit score, why do I need one, and how do I get one?” is CAREFULLY.

And yes, I know that answer doesn’t make sense for two of the three questions listed but since I cannot tattoo it on your skin, write it in fire, or hire a murder of crows to fly around singing it at you, I’m doing the best I can here.

Don’t buy what you can’t afford, make your payments on time, keep an eye on your credit report, and enjoy a life with lower interest rates and more opportunity to build the future you want with an excellent good credit score that you worked hard to get.

Need some more motivation to clean up your credit? Read how one family went from living paycheck to paycheck to an 800+ credit score and then try YNAB for free for 34 days to enjoy less money stress.

{kind=link}