Increased interest rates, building material supply chain bottlenecks and elevated construction costs continue to put a damper on the single-family housing market. For the first time since June 2020, both single-family starts and permits fell below a one million annual pace.

Overall housing starts fell 2.0% to a seasonally adjusted annual rate of 1.56 million units in June from an upwardly revised reading the previous month, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau.

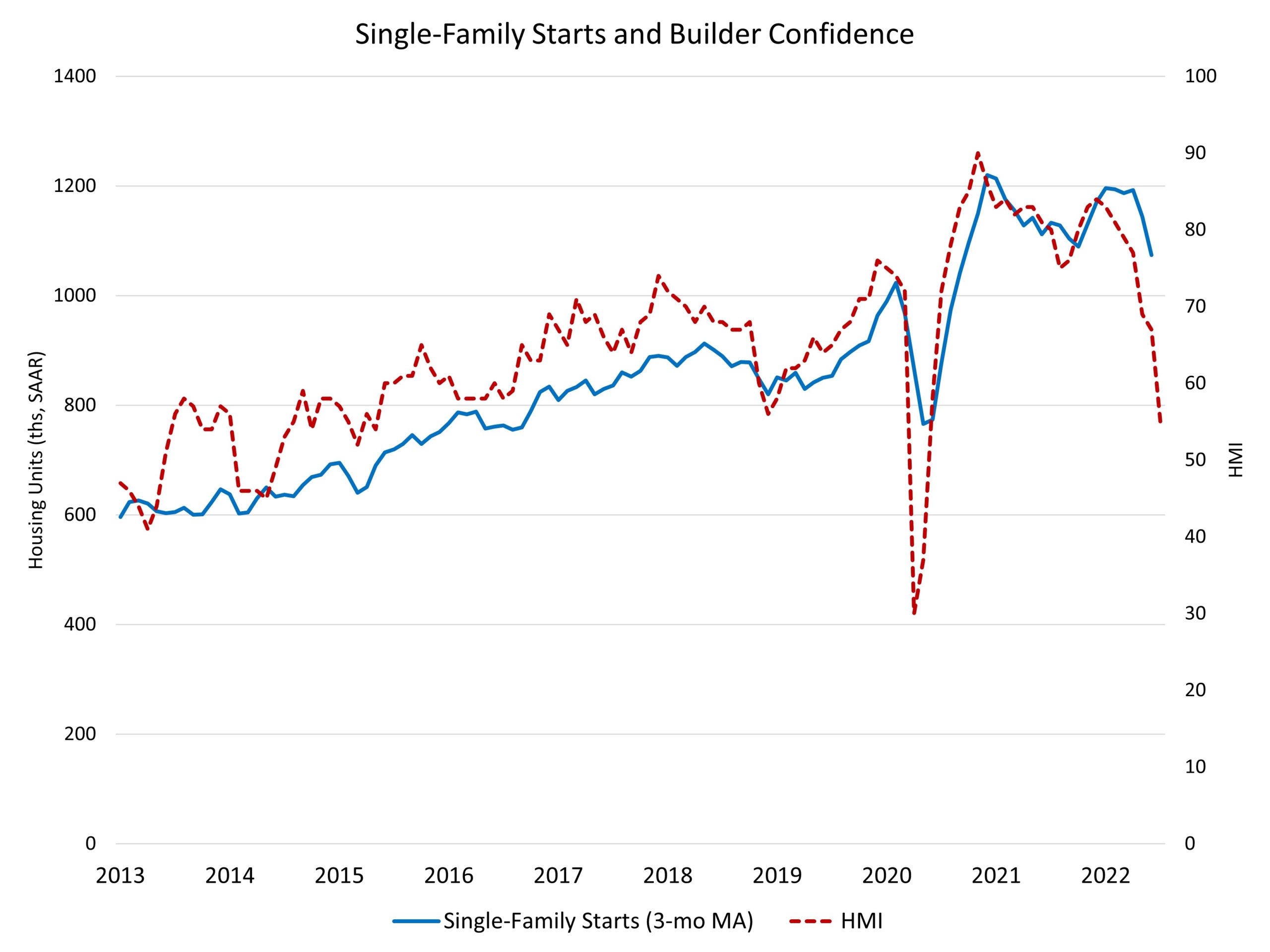

The June reading of 1.56 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months. Within this overall number, single-family starts decreased 8.1% to a 982,000 seasonally adjusted annual rate. This is the lowest single-family starts pace since June 2020.

In June single-family builder confidence decreased a dramatic 12 points to a level of 55, according to the NAHB/Wells Fargo Housing Market Index (HMI). After peaking at a level of 90 in November 2020, builders have reported ongoing concerns over elevated material costs and delivery delays. Moreover, the sharp rise in mortgage interest rates during the first half of 2022 has also had a negative impact on the demand-side of the building market.

Reduced housing demand will continue to have a weakening impact on single-family home building in the months ahead per the HMI. Single-family permits decreased 8.0% to a 967,000 unit rate in June. This is the lowest pace for single-family permits since June 2020.

Driven by ongoing strength in the rental market, reinforced by higher mortgage interest rates, the multifamily sector, which includes apartment buildings and condos, increased 10.3% an annualized 577,000 pace of starts in June. Multifamily permits increased 11.5% to an annualized 718,000 pace.

The number of single-family homes permitted but not started construction has likely peaked after rising over pervious quarters due to supply-chain issues. In June, there were 147,000 homes authorized but not started construction. This marks a year-over-year decline, the first such decline in a year. Additional declines for this count are expected ahead as permit growth weakens and backlog is reduced.

On a regional and year-to-date basis, combined single-family and multifamily starts are 4.4% lower in the Northeast, 4.7% higher in the Midwest, 11.1% higher in the South and 0.4% lower in the West.

Looking at regional permit data on a year-to-date basis, permits are 5.1% lower in the Northeast, 2.5% higher in the Midwest, 2.9% higher in the South and 3.0% higher in the West.

As an indicator of the economic impact of housing and as a result of accelerating permits and starts in recent quarters, there are now 824,000 single-family homes under construction. This is 21% higher than a year ago. There are currently 856,000 apartments under construction, up 24% from a year ago. Total housing units now under construction (single-family and multifamily combined) is 24% higher than a year ago. The number of single-family units in the construction pipeline is now peaking for this business cycle and will decline in the months ahead given recent declines in buyer traffic.

Related

{kind=link}