The U.S. Treasury makes regular decisions about the issuance patterns of its debt securities with the objective of meeting the financing needs of the government at the lowest cost of servicing the debt over time.[1] The overall level of outstanding debt is beyond the direct control of the Treasury, as it is determined by federal budget deficits resulting from legislative decisions and economic developments. However, the Treasury exercises full control over the structure of that debt through its decisions on the pattern of issuance across different types of securities and different maturity points.

We have developed a tool to make projections of the structure of Treasury debt based on assumed funding needs and an assumed path for gross issuance amounts.[2] This tool, which can be found in the Brookings Institution’s public Github page, tracks the outstanding stock of Treasury debt (and the evolution of the Federal Reserve’s holdings of Treasury debt) at the individual security level. This post describes how to implement that tool and provides an illustrative example.

A variety of measures have been used to describe the structure of outstanding Treasury debt. In the presentation it publishes at the time of the quarterly refunding announcement, the Treasury reports the weighted average maturity of the debt, the share of debt maturing within particular horizons, and the shares of debt in bills, floating rate notes (FRNs), and inflation-protected securities (TIPS).[3] The Treasury Borrowing Advisory Committee (TBAC), a group of private market participants with which the Treasury consults as part of the quarterly refunding process, has considered a more extensive set of measures to characterize the outstanding debt.[4]

The structure of the debt, along with market conditions, determines the expected debt service costs to the Treasury as well as the risks it faces regarding those costs, such as their volatility over time. There have been several efforts in recent years to measure the trade-off between these considerations and to determine the optimal debt structure under a given model (see, for example, this paper published by the Hutchins Center).[5] The TBAC itself has incorporated this type of analysis when formulating recommendations on key debt management issues.[6]

It is therefore important to be able to make projections of the full maturity structure of Treasury debt—whether for purposes of understanding the path of various statistics describing the debt structure or assessing the optimality of that debt structure. These projections need to have a relatively long horizon because debt management decisions made today have repercussions on the debt structure for many years going forward and because issuance (with the exception of bills) tends to adjust gradually under the “regular and predictable” approach taken by the Treasury.

One additional consideration is that the Fed’s portfolio, known as the System Open Market Account (SOMA), has substantially altered the characteristics of the debt. As detailed in a TBAC presentation from February 2020, from the perspective of a consolidated government balance sheet, one can think of Treasury securities held in the SOMA portfolio (if held to maturity) as being FRNs indexed to the overnight interest rate.[7] Thus, it often will be useful to adjust the reported statistics on the debt to reflect this maturity adjustment from the SOMA portfolio.

The tool that we have developed tracks both the outstanding stock of Treasury debt and the evolution of the SOMA portfolio at the individual security level. These two components are considered jointly because the evolution of the SOMA portfolio (and whether its Treasury holdings are reinvested or allowed to mature) affects the Treasury’s borrowing needs from the private sector.[8]

The basic mechanics of this tool are as follows: The user inputs the path of Treasury borrowing needs for the forecast horizon, reflecting assumed budget deficits for the federal government and technical issues such as the assumed path of the Treasury’s cash balance. The user also inputs a path of gross issuance for all non-bill securities over the forecast horizon. The assumed gross issuance for non-bill securities provides a path of net issuance outside the bill sector after accounting for maturing securities. The tool then assumes that any funding needs not covered by non-bill net issuance will be made up by issuance of bills. That is, bills are the residual in this exercise, which allows the non-bill issuance assumptions to capture the regular and predictable approach of the Treasury.[9]

To demonstrate how the tool functions, we consider a projection in which nominal issuance sizes going forward are kept constant. To be clear, this assumption does not reflect any decision or projection that has been made by the Treasury or the TBAC—it is simply posited here for illustrative purposes. We input the funding needs for the government based on the latest CBO projection and assume that the Treasury’s cash balance will grow at 3.5% to keep it roughly in line with nominal GDP.

Under those assumptions, we observe some important patterns in the projections:

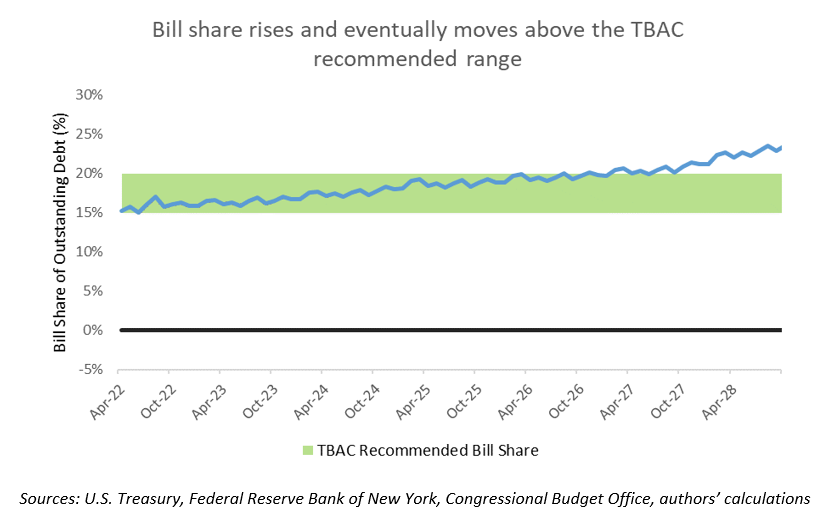

- The bill share of outstanding debt is within the TBAC recommended range of 15% to 20% over the next several years, albeit at the lower end of that range in the near term.[10] This share, because it is the residual in the exercise, provides a gauge of whether the non-bill issuance assumptions are appropriate. If the projection had instead fallen below the recommended range, it would indicate that non-bill issuance would need to be cut to meet TBAC’s bill share recommendation.

- The bill share rises over the projection horizon, eventually moving above the recommended range. At that time, holding non-bill issuance constant does not raise enough net revenue to keep the bill share from rising past 20%, and non-bill issuance would need to be raised to meet the TBAC recommendation.

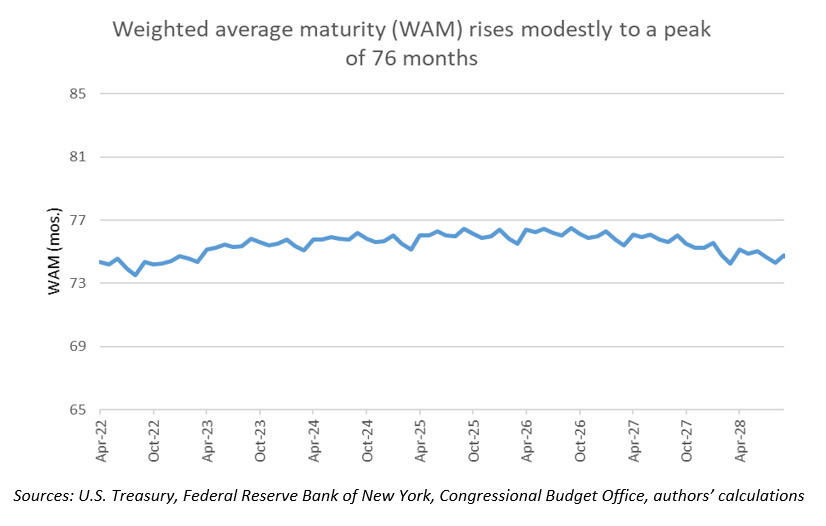

- The weighted average maturity (WAM) of the debt rises modestly over the next several years to a peak of 76 months. The TBAC often describes the desired trajectory of the WAM in qualitative terms. This tool allows one to quantify that path under any desired set of issuance assumptions.

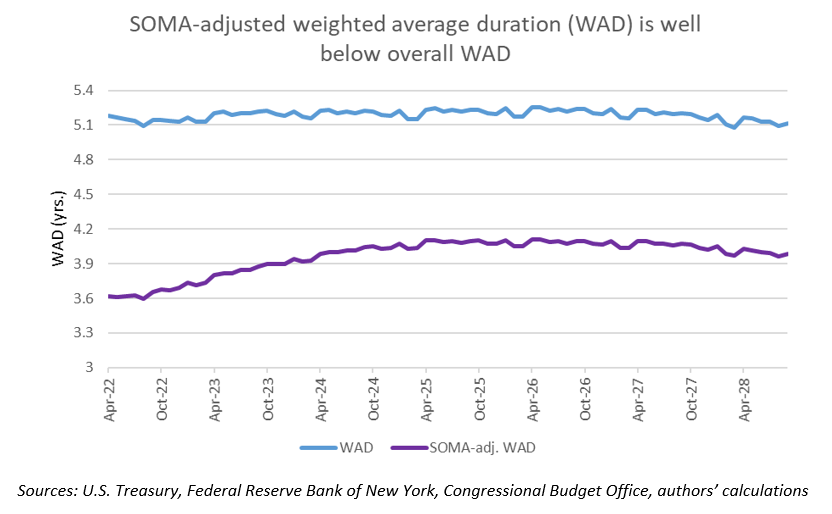

- The weighted average duration (WAD) of the debt holds relatively steady at just over five years. Adjusting for SOMA holdings reduces the current WAD by nearly 1.5 years. The adjusted WAD measure rises more steeply because the decline in SOMA holdings reduces the stock of zero-duration assets for the Treasury.

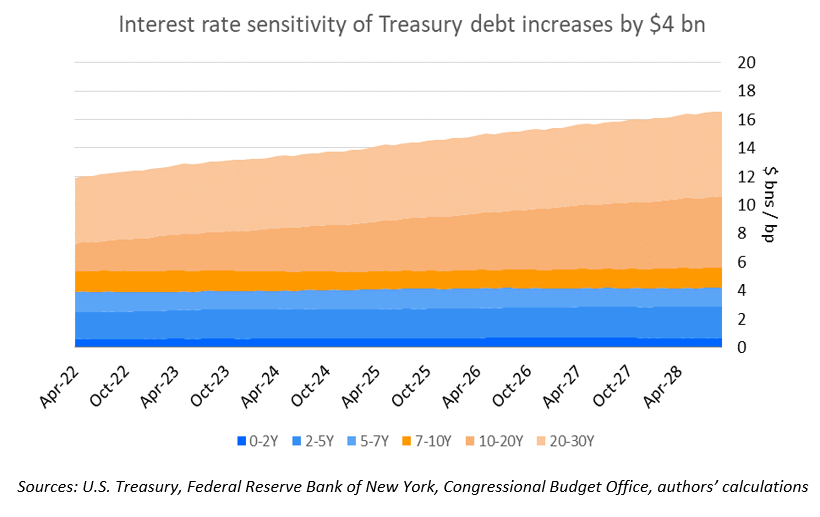

- We can measure the total amount of interest rate risk in the market as the sensitivity of the market value of Treasury debt to a one basis point (or 0.01 percentage point) shift in Treasury yields across all maturities. That risk rises notably over the forecast horizon, from about $12 billion today to $16 billion by 2028. The majority of this risk arises from outstanding debt with maturities longer than 10 years.

Overall, we hope this analysis and the related code can serve as a useful tool that supports further assessment of the structure of Treasury debt and its path going forward.

[1] This objective is not formally stated anywhere, but it is a common description used in the discussion of debt management issues.

[2] The model presented here is based on the structure of Treasury issuance and the form of the input files as of March 2022. The code would potentially need to be adapted if there were changes to the types of Treasury securities issued, to the settlement cycles of Treasury securities, or to the structure of the input files.

[3] For example, see slides 24 to 27 of this Treasury presentation https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/.

[4] For example, see the material on slides 48 to 62 of this presentation https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/.

[5] The code for running the optimal debt structure model is also available on the Brookings Institution’s public Github page https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/. That model is designed to assess the optimality of different maturity structures, whereas the code described here is focused strictly on projecting the maturity structure obtained under a given set of issuance assumptions (with greater detail than used in the optimal debt structure model).

[6] For example, see the material on slides 95 to 109 of this presentation https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/.

[7] See slides 55 to 75 of this presentation https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/.

[8] The Fed typically reinvests its SOMA holdings by rolling maturing amounts into new securities. These amounts are treated as “add-ons,” or additional amounts added to the gross issuance to the private sector. Because our exercise specifies gross issuance as the amount offered to the private sector, a decision by the Fed to stop reinvestments in order to shrink the SOMA implies less net funding raised for the Treasury relative to the issuance specified in the exercise.

[9] The tool does not keep track of the maturity structure within the bill sector. It simply calculates the amount of outstanding bills needed each month and is agnostic about how bill issuance is structured to reach to that amount.

[10] The targeted bill range was discussed in a TBAC charge from November 2020. See slides 48-68 of this presentation https://www.brookings.edu/blog/up-front/2022/07/27/projecting-the-structure-of-us-treasury-debt/. This range represents the current recommendation from TBAC and could always be altered by TBAC as conditions evolve.

Both authors are employees of the D. E. Shaw group, a global investment and technology development firm. The D. E. Shaw group reviewed the data and analysis prior to publishing. Other than as employees of the D. E. Shaw group, the authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. Neither author is currently an officer, director, or board member of any organization with a financial or political interest in this article. Brian Sack is a member of the U.S. Treasury Borrowing Advisory Committee, but this work does not necessarily reflect the views of that committee.

{kind=link}