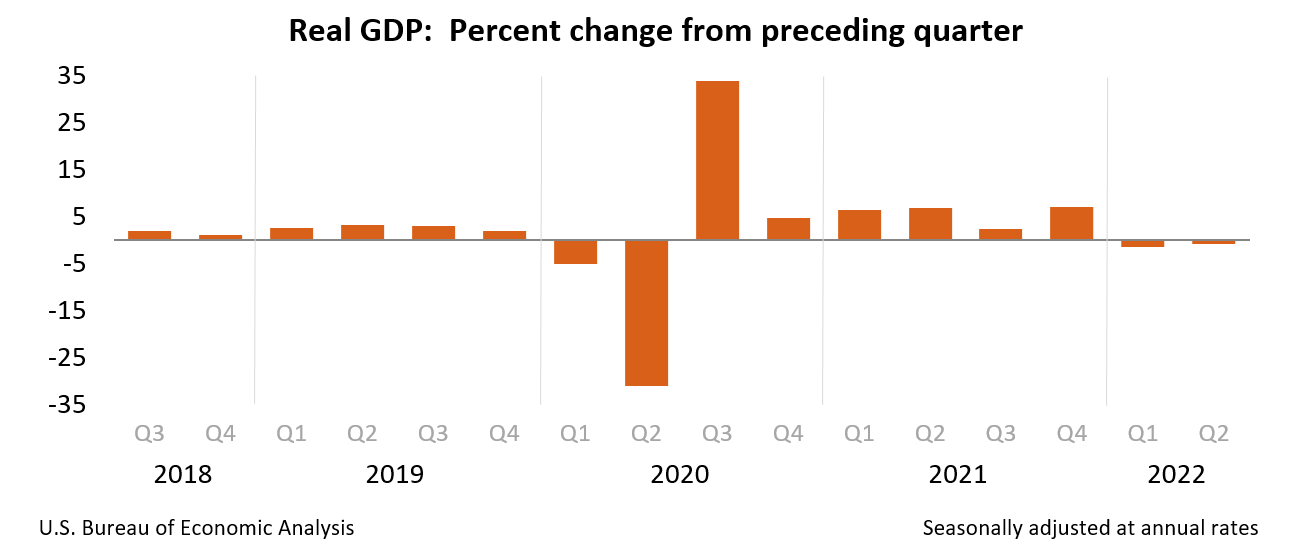

Following a negative GDP print in the first quarter, a strong but inflation-racked economy expanded in the second quarter on a nominal basis, but contracted in real inflation-adjusted terms. BEA reported “Real gross domestic product decreased at an annual rate of 0.9 percent in the second quarter of 2022, following a decrease of 1.6 percent in the first quarter. The smaller decrease in the second quarter primarily reflected an upturn in exports and a smaller decrease in federal government spending.”

Despite the robustness of the labor market and consumer spending during the first half of the year, this is the second consecutive quarter of real (Inflation-adjusted) economic contraction. Nominal GDP is plus 7.8% annualized, but that is due mostly to the post-pandemic surge in prices.1

What does this mean for investors?

As we discussed prior, Recessions matter to investors because they reduce employment, drag down consumer spending, lower corporate revenues, and ultimately drag profits down. On top of that is the sentiment impact, which affects equity multiples. Lower earnings and lower multiples on those earnings are a one-two punch.

My colleague Ben Carlson describes the two kinds of bear markets: Recessionary and Non-Recessionary. The non-recessionary bear markets fall ~25.9% on average, while the recessionary bear markets get hit a much harder 39.6%. Note these are averages, and they have a broad dispersion 20% to 33.5% for run-of-the-mill bear markets to a much deeper bear range during recessions of 20% to 86.2%.2

The bad news is we are stuck with debating the meaning of 2 consecutive quarters of negative GDP as a Recession for three more months. The good news is this lowers expectations for the FOMC going 75 basis points in September. Market reaction was almost non-existent, suggesting a slowdown or even a mild recession is already priced in.

See also:

The 2 Types of Bear Markets (A Wealth of Common Sense, May 22, 2022)

Previously:

Soft Landing RIP (July 25, 2022)

Why Recessions Matter to Investors (July 11, 2022)

Too Late to Sell, Too Early to Buy… (June 16, 2022)

GDP Update: -52.8% (June 2, 2020)

Cherry Picking Your Favorite GDP Forecast (May 18, 2016)

____________

1. Note the Atlanta Fed’s GDPNow got the direction right but the magnitude wrong.

2. This assumes you accept the 20% rule of thumb as meaningful…

The post GDP = -0.9% appeared first on The Big Picture.

{kind=link}