New orders for durable goods increased 1.9 percent in June, following an 0.8 percent gain in May, the 8th increase in the last nine months. Total durable-goods orders are up 12.2 percent from a year ago. The June gain puts the level of total durable-goods orders at $272.6 billion, the second highest on record.

New orders for nondefense capital goods excluding aircraft, or core capital goods, a proxy for business equipment investment, rose 0.5 percent in June after increasing 0.5 percent in May. Orders are up 11.2 percent from a year ago, with the level at $73.9 billion, a new record high.

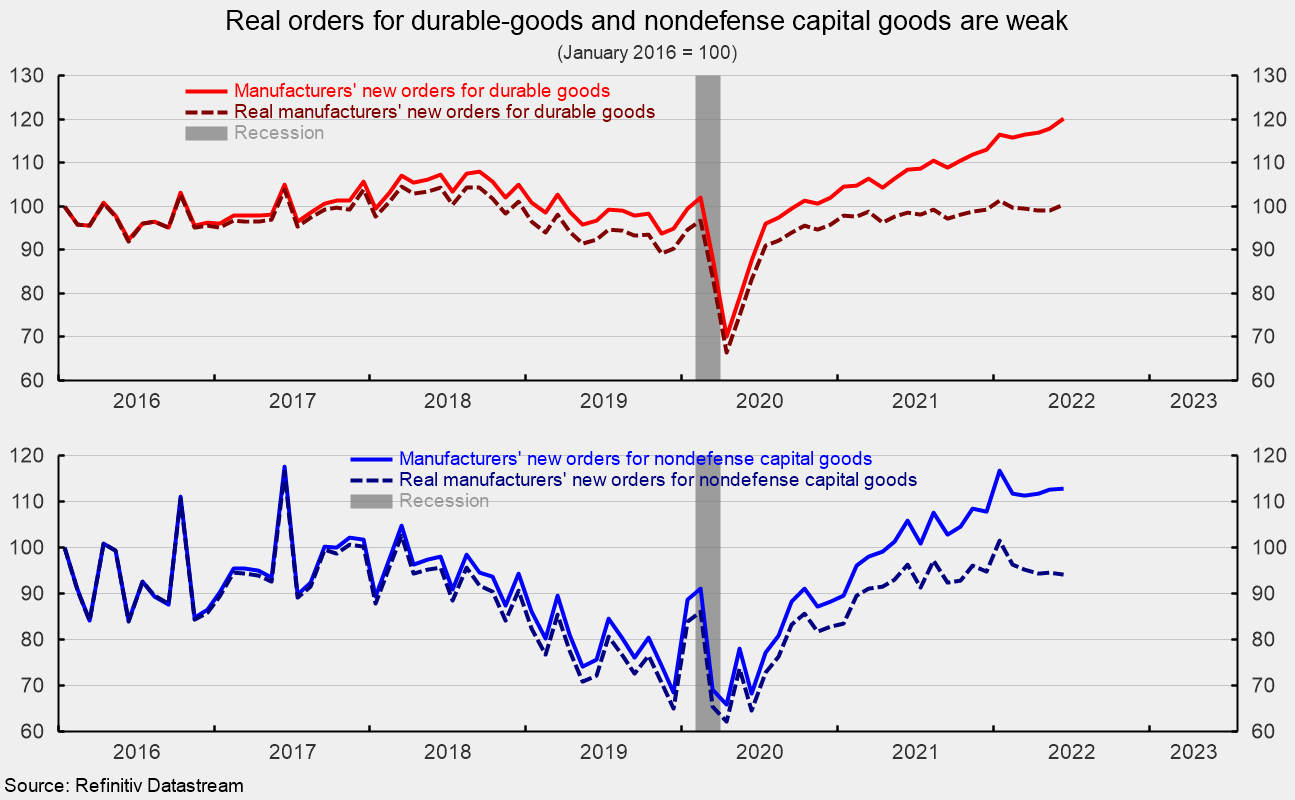

However, rapid price increases have had an impact on capital goods orders. In real terms, after adjusting for inflation, real new orders for durable goods rose 1.2 percent in June, while real new orders for nondefense capital goods – one of AIERs leading indicators – fell 0.6 percent (see first chart). Real new orders for durable goods and real new orders for nondefense capital goods were below their January 2022 level (see first chart again).

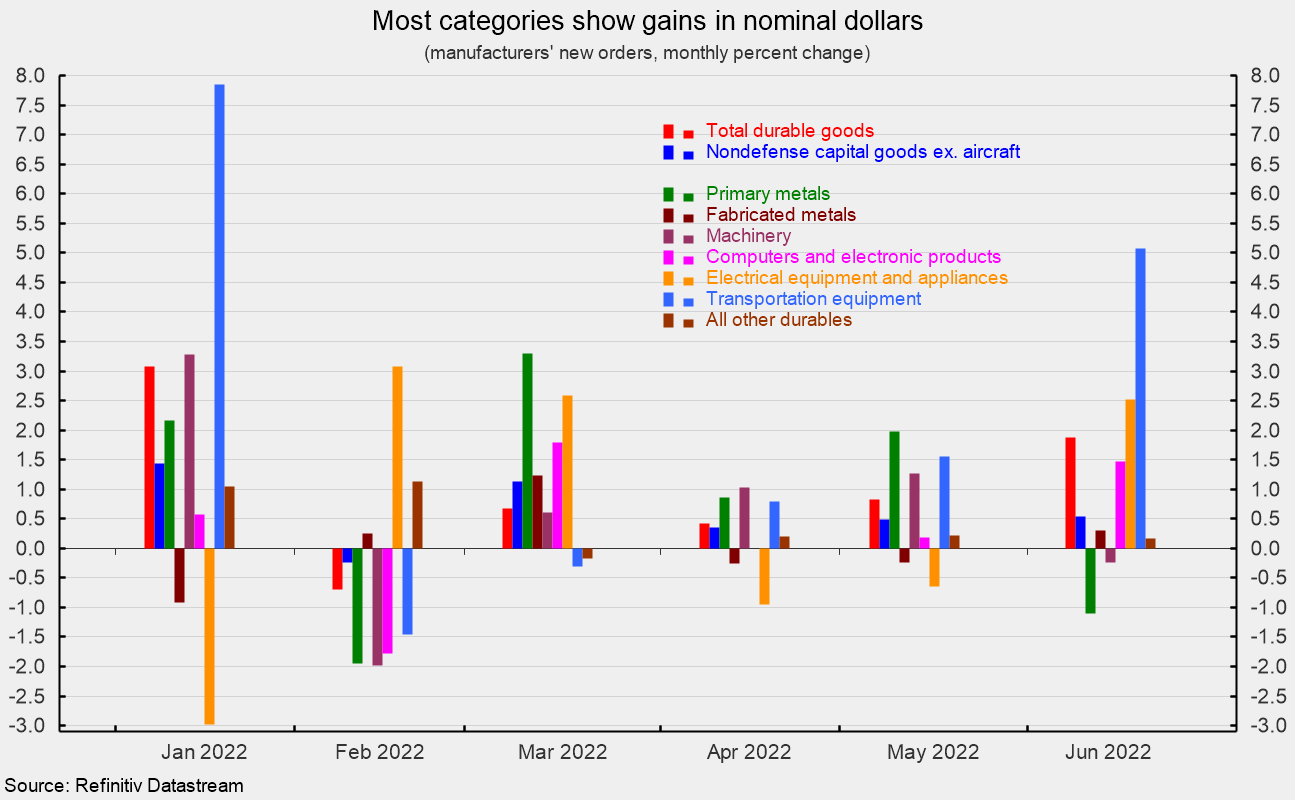

Five of the seven categories shown in the durable-goods report posted a gain in June, in nominal terms. Among the major individual categories, transportation equipment orders led with a 5.1 percent increase, followed by electrical equipment and appliances with a 2.5 percent rise, and computers and electronic products with a 1.5 percent gain. Fabricated metals gained 0.3 percent while all other durables added 0.2 percent. Within the transportation equipment category, defense aircraft surged 80.6 percent and motor vehicles and parts were up 1.5 percent, but nondefense aircraft fell 2.1 percent. On the downside for the major categories, primary metals orders dropped 1.1 percent and machinery orders fell 0.2 percent (see second chart). From a year ago, every major category shows a gain.

Durable-goods orders continue to rise at a robust pace in nominal-dollars but after adjusting for price increases, real orders for durable goods are rising at a very slow trend rate. Nominal new orders for capital goods are also growing briskly but in real terms, the trend is flat or down slightly. The outlook remains highly uncertain as sustained upward pressure on prices continues to distort activity and impact decision making. Though progress is being made, labor and materials shortages continue to hamper production. Furthermore, the fallout from the Russian invasion of Ukraine and periodic lockdowns in China continue to disrupt global supply chains. Finally, the Federal Reserve has intensified the current interest rate tightening cycle, boosting the probability of a policy mistake. Caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}