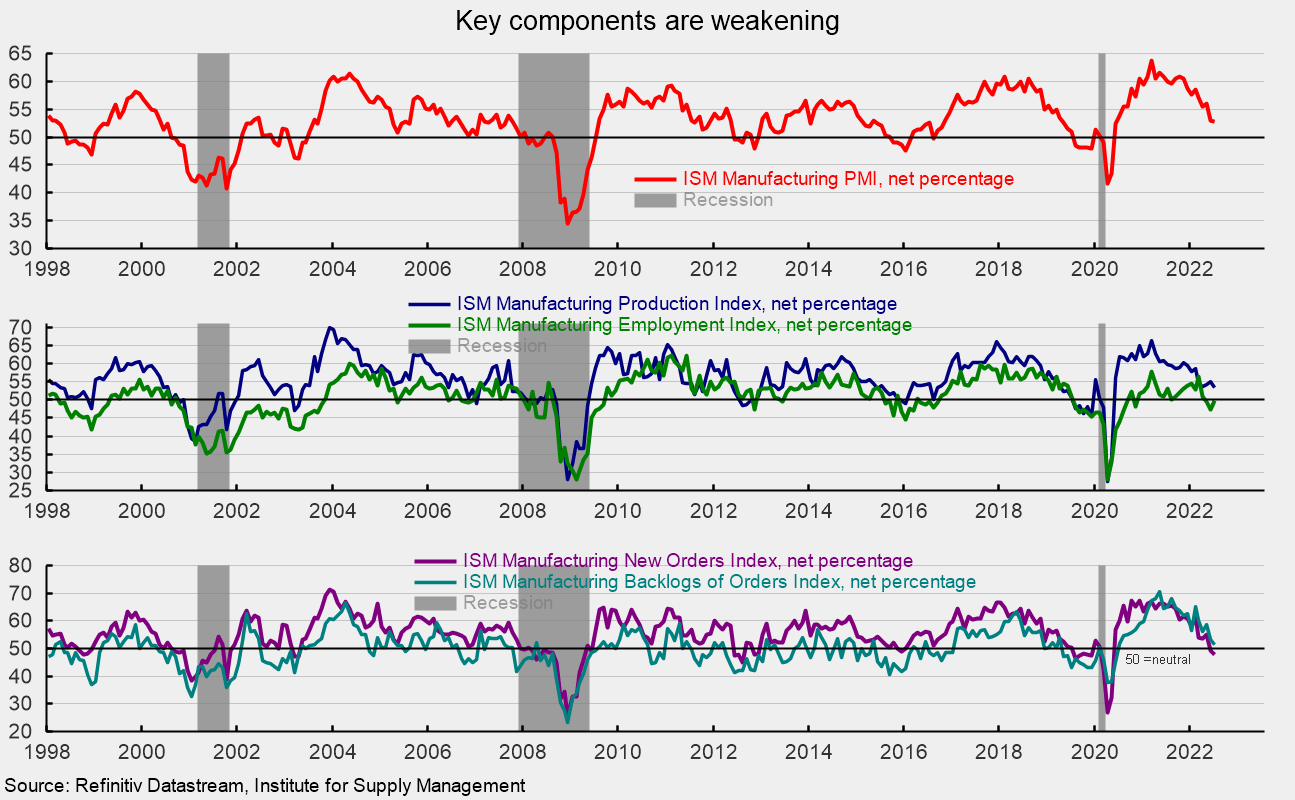

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell to 52.8 percent in July, off 0.2 points from 53.0 percent in June (50 is neutral). July is the 26th consecutive reading above the neutral threshold, but the level is down sharply from the March 2021 peak (see the top of the first chart). The survey results indicate that the manufacturing sector continues to expand, but demand has softened, and price pressures have eased significantly. Furthermore, while survey respondents remained optimistic about future demand, there were also some cautious comments.

The Production Index registered a 53.5 percent result in July, a drop of 1.4 points from June (see the middle of the first chart). The index has been above 50 for 26 months, but the six-month average has declined for 16 consecutive months and the July average of 54.9 percent is the lowest since September 2020.

The Employment Index rose in July but remained slightly below the neutral 50 threshold for the third consecutive month. The 49.9 percent reading suggests employment was essentially unchanged in July (see the middle of the first chart). The report states, “According to Business Survey Committee respondents’ comments, companies continue to hire at strong rates, with few indications of layoffs, hiring freezes or headcount reduction through attrition. Panelists reported higher rates of quits, reversing June’s positive trend.“

The Bureau of Labor Statistics’ Employment Situation report for July is due out on Friday, August 5, and expectations are for a gain of 250,000 nonfarm payroll jobs including the addition of 15,000 jobs in manufacturing.

The new orders index sank 1.2 points to 48.0 percent in July. That is the second consecutive reading below neutral and suggests orders contracted at a faster pace (see the bottom of the first chart). The new export orders index, a separate measure from new orders, rose to 52.6 percent versus 50.7 percent in June. The new export orders index has been above 50 for 25 consecutive months.

The Backlog-of-Orders Index came in at 51.3 percent versus 53.2 percent in June, a 1.9-point decline (see the bottom of the first chart). This measure has pulled back from the record-high 70.6 percent result in May 2021 but has been above 50 for 25 consecutive months. The index suggests manufacturers’ backlogs continue to rise, but the pace continues to decelerate.

Customer inventories in July are still considered too low, with the index coming in at 39.5 percent, up 4.3 points from June (index results below 50 indicate customers’ inventories are too low). The index has been below 50 for 70 consecutive months. Insufficient inventory is a positive sign for future production.

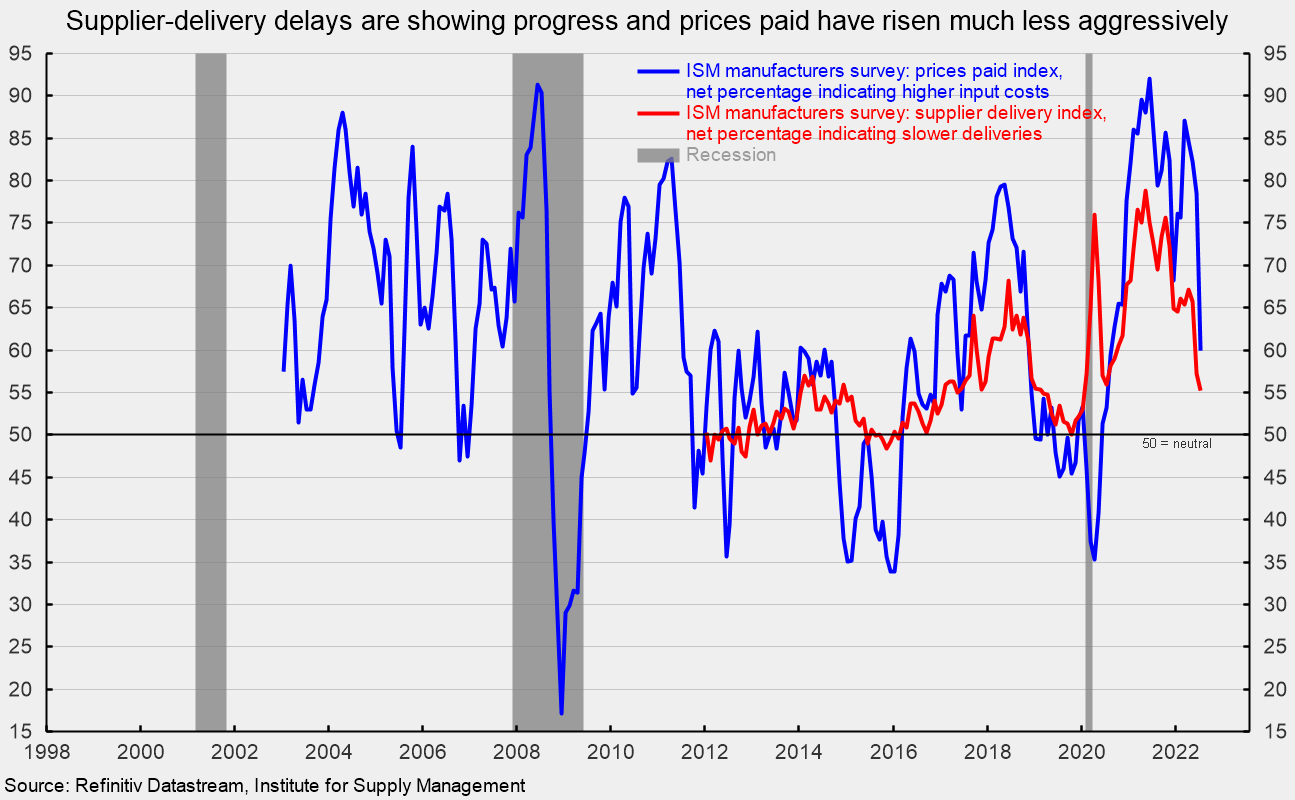

The index for prices for input materials sank 18.5 points to 60.0 in July and is the fourth consecutive monthly decline (see second chart). The index is down from 87.1 percent in March 2022 and suggests price pressures have eased significantly.

The supplier deliveries index registered a 55.2 percent result in July, down 2.1 points from the June result. The index was at 78.8 percent in May 2021. The easing trend over the past 14 months suggest deliveries are slowing at a much slower rate (see second chart).

The report noted, “Prices expansion eased dramatically in July, but instability in global energy markets continues.” In addition, “Sentiment remained optimistic regarding demand, with six positive growth comments for every cautious comment.” But the report also stated, “Panelists are now expressing concern about a softening in the economy, as new order rates contracted for the second month amid developing anxiety about excess inventory in the supply chain.”

Overall, economic risks remain elevated due to the impact of inflation, an intensifying Fed tightening cycle, continued fallout from the Russian invasion of Ukraine, and waves of new Covid-19 cases and lockdowns in China. The outlook remains highly uncertain. Caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}