It should come as little surprise that something as simple as identifying the start of a recession would generate controversy. Everything has become politicized. One could point out that the current economic contraction is still quite mild. Or that pandemic mitigation policies of the previous administration were as much (if not more) of a factor in choking off economic growth as the wokism of the current one. One could, if so inclined, point to the Fed’s languorous response to steadily rising prices throughout 2021.

But no. The response has been predictably partisan, challenging the very definition of a recession itself. Postmodernists and lawyers, always a disproportionately large cohort of the very worst people in society, currently hold the high ground of discourse.

Nevertheless, as recessions go the current one is an odd duck indeed. Examples of recessions where the labor market has been strong, let alone as strong as the current one, are essentially nonexistent in recent economic history.

US Unemployment Rate (%) vs.GDP year-over-year, 2012 dollars (1960 – present)

In the post-WWII era, increases in unemployment lag the start of recessions by varying amounts. In twelve economic recessions, the trough of the employment rate has preceded the start of recession by an average six months, with a range of one to sixteen months. Unemployment does not cause recessions; recessions – declining economic growth – cause rates of unemployment to rise. So if history is any guide, a rise in unemployment may be from months or to longer than a year off.

But why is the job market so hot? Doesn’t that clash with notions of an economy in contraction? Possibly, but not necessarily. In light of the unprecedented circumstances wrought by lockdowns, stay-at-home orders, and other commercial depressants over the last few years, alternate or contributing explanations deserve consideration.

Inflation is at levels not seen in 40 years. US equity markets (read: 401Ks and IRAs) had their worst six-month start since 1970 in the first half of 2022. CBSNews summarizes:

[D]ata shared by Morningstar show that the most popular target-date funds — mutual funds that hold a range of investments and that automatically adjust according to a “target” retirement date — have lost between 10% and 22% of their assets under management this year … With the median 401(k) account having a balance of just $17,700 before the pandemic, this year’s market decline would lop off more than $3,500 in value. A would-be retiree with a balance of over $81,000 — which would put them in the top 25% of savers — would see their nest egg shrink to just $64,800.

The specter of a new covid variant causing a return to disease mitigation policies, as well as a growing concern that monkeypox will be the next maladie célèbre, are very much alive. Midterm elections are only a few months away. For those and other reasons, why wouldn’t there be a rush into, or more likely back into, the workforce? As mentioned, the tremendous number of open jobs has been another unusual feature of the post-pandemic and newly-christened recession, accommodating that shift.

Several additional facts support this “flight to jobs” explanation.

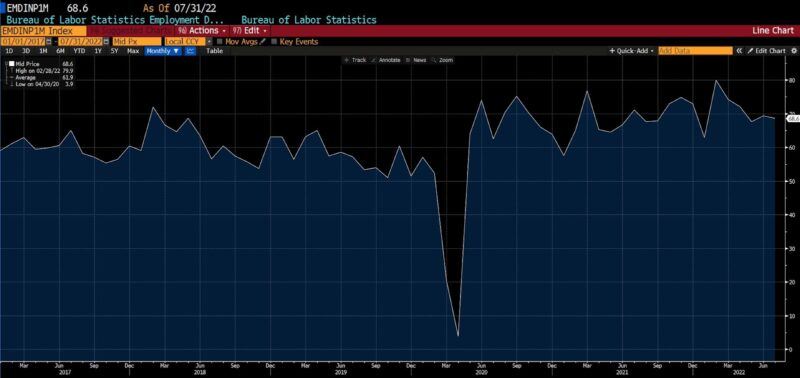

- Not only was last Friday’s jobs report unexpectedly strong, but the previous report was also revised upwards by over 20,000 new jobs. Also, the types of jobs being taken are diverse, ranging from hospitality to such interest rate-sensitive sectors as construction. Employment diffusion, as measured by the Bureau of Labor Statistics (BLS), is currently at 68.6 percent, indicating not only expanding employment, but jobs being taken across a wide range of industries. Thus, the rush into the workforce is broad-based, not driven by factors unique to a particular industry or sector.

BLS Employment Diffusion of Nonfarm Payrolls (2017 – present)

- US average hourly wage growth, year-over-year, had been strong since mid-2021, dropping back a bit since March 2022. But the increase in inflation has vastly outstripped the benefit of pay increases. In just one example, from the start of 2021 through mid-June 2022, the average US price of a gallon of gasoline rose 113%. It has since fallen roughly 80 cents per gallon since then, but is still up 85 percent since the start of last year.

US Average Hourly Earnings year-over-year vs. CPI year-over-year (2012 – present)

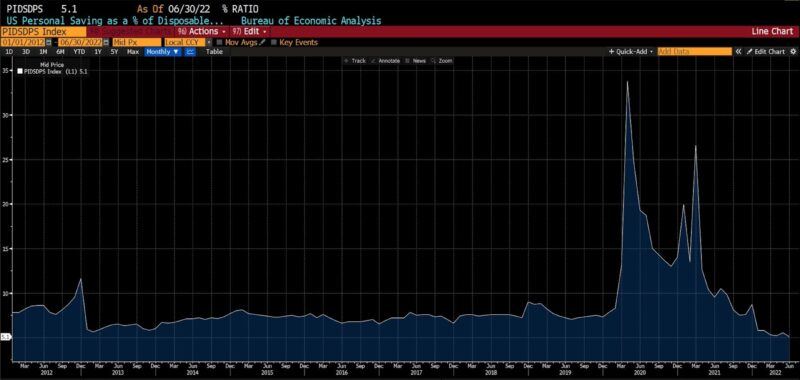

- Rates of saving have fallen to levels lower than they were before the covid pandemic. Between 2012 and the end of 2019, personal savings as a percentage of disposable income averaged 7.4 percent, with a brief low of 5.6 percent in early 2013 as the emaciated recovery from the Great Recession began. As of June 2022, US personal savings sit at 5.1 percent of disposable income, the lowest level since October 2009, shortly after Lehman Brothers collapsed. It bears mentioning that, contrary to currently spiking prices, the former drop in savings took place while a brief deflation was occurring, possibly offsetting the household budget impact of increased spending.

US Personal Saving as a Percent of Disposable Income (2012 – present)

(Source: Bloomberg Finance, LP)

- It is no surprise that the number of Americans with two jobs is rising. The all-time high number of Americans with two jobs was hit in September 2019. While that number has not been reached, the rate of US workers taking second jobs has vaulted. The increase in the number of Americans with two jobs has increased by 1.1 million over the fourteen months since the start of 2021. Prior to the pandemic, it took five to six years (roughly between 2013 and mid-2019) for the same number of individuals to take two jobs. It is additionally likely that this data greatly underestimates the actual number of individuals with two forms of employment, since many (if not most) secondary jobs are on a cash basis, thus “off the books.”

US Number of Multiple Jobholders (2012 – present)

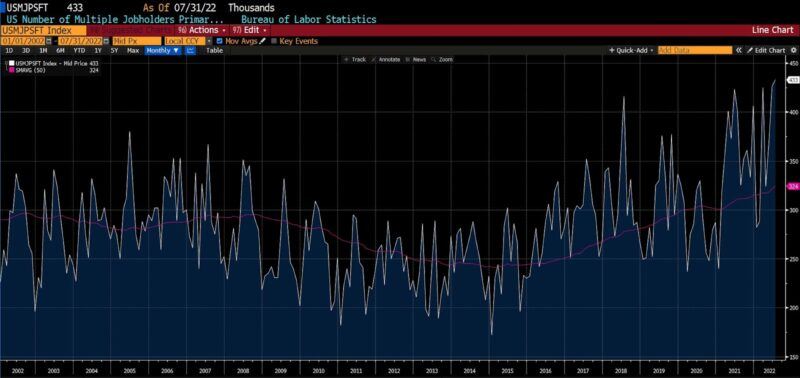

But most surprising of all is that in July 2022, the number of Americans not only working two jobs, but two full-time jobs, reached a record high. (The twenty-year trend and a simple moving average are shown here.)

US Number of Multiple Jobholders with Primary & Secondary Full-Time Jobs (2002 – present)

Growing uncertainty may explain the seemingly discordant labor market. The rapid onset of concern over eroding purchasing power, diminishing retirement prospects, and sagging growth may be jolting passivity into action. Individuals may be responding to mounting financial insecurity by securing, improving, or adding to their employment.

Much of this explanation is at odds with classic manifestations of uncertainty in economics. Typically, dubitation among workers, consumers or producers manifests as delayed consumption, postponed hiring plans, or canceled business expansion plans. The avoidance of irreversible investments is frequently cited. Within the masses currently hustling back into the job market, no doubt, are some of the millions who retired early during the pandemic. Also many of the women who, unable to secure childcare during pandemic school closures, were forced to abandon their jobs.

The Great Reconsideration is likely over. But none of this necessarily implies an impending catastrophe, economic or otherwise. The case presented here is intended to call into question the automatic assumption that the current set of economic circumstances, notably in the job market, nullifies the possibility or even probability of a classic economic recession. Unemployment, for good reason, lags the onset of recessions. And assuming that a widespread burst in employment categorically signifies optimism or portends a quick resumption of economic growth is simply unwarranted.

Peter C. Earle

Peter C. Earle is an economist and writer who joined AIER in 2018. Prior to that he spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area, as well as running a gaming and cryptocurrency consultancy. His research focuses on financial markets, monetary policy, the economics of games, and problems in economic measurement. He has been quoted by the Wall Street Journal, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications. Pete holds an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point. Follow him on Twitter.

Selected Publications

“General Institutional Considerations of Blockchain and Emerging Applications” Co-Authored with David M. Waugh in The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges (forthcoming), edited by Baker, Benedetti, Nikbakht, and Smith (2022)

“Operation Warp Speed” Co-authored with Edwar Escalante in Pandemics and Liberty (forthcoming), edited by Raymond J. March and Ryan M. Yonk (2022)

“A Virtual Weimar: Hyperinflation in Diablo III” in The Invisible Hand in Virtual Worlds: The Economic Order of Video Games, edited by Matthew McCaffrey (2021)

“The Fickle Science of Lockdowns” Co-authored with Phillip W. Magness, Wall Street Journal (December 2021)

“How Does a Well-Functioning Gold Standard Function?” Co-authored with William J. Luther, SSRN (November 2021)

“Populist Prophets, Public Prophets: Pied Pipers of Lucre, Then and Now” in Financial History (Summer 2021)

“Boston’s Forgotten Lockdowns” in The American Conservative (November 2020)

“Private Governance and Rules for a Flat World” in Creighton Journal of Interdisciplinary Leadership (June 2019)

“’Federal Jobs Guarantee’ Idea Is Costly, Misguided, And Increasingly Popular With Democrats” in Investor’s Business Daily (December 2018)

{kind=link}