Investing regularly has many benefits, and most of us want to start as early as possible.

But, then life happens.

We put off the decision to start investing as there is always some major expense coming up.

More often than not, we feel our salary is too low and we can’t save much. Given the paltry amount that we can save, why bother spending time and energy looking for an appropriate mutual fund or investment opportunity?

We convince ourselves that over time we will gradually reduce our expenses to save up for investing, or when our salary grows we will have large enough monthly savings to start investing.

Unfortunately, as all of us would have experienced, our expenses somehow always grow much faster than our salaries!

Eventually, we keep perennially postponing our decision to invest. It’s the same story for most of us.

But here comes the real question…

Leaving the financial gyan aside, does it really matter if there is a delay of a few years?

What big difference does it really make if I wait for my savings to improve before I start investing?

What’s all this fuss about investing early?

Let’s find out…

Your monthly savings are too low. Should you postpone investing till your savings increase or start investing immediately?

Most of us keep postponing our investments as we feel the amount of money that we can save every month is too less. How big of a difference can it make?

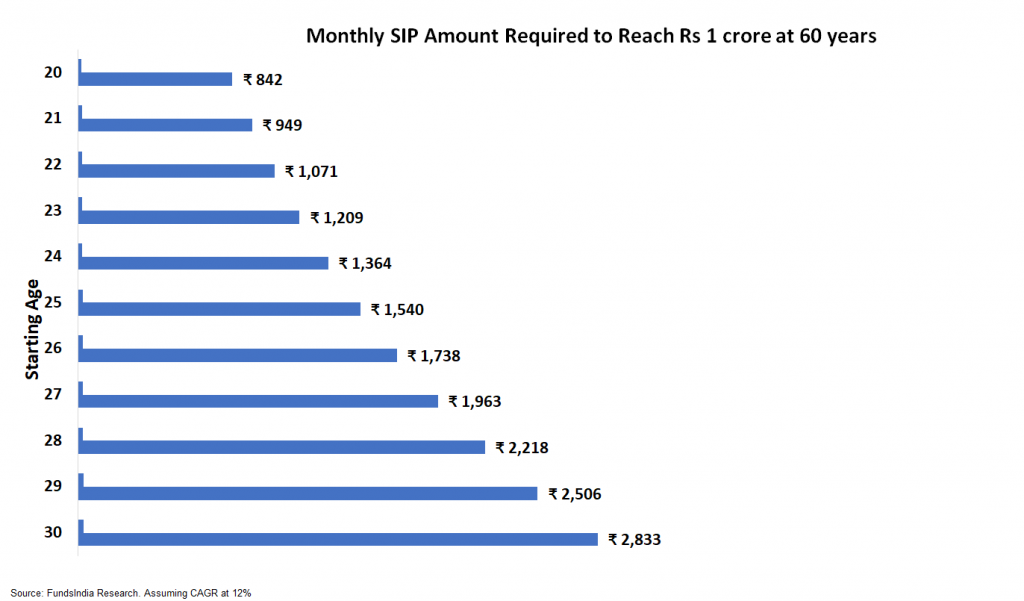

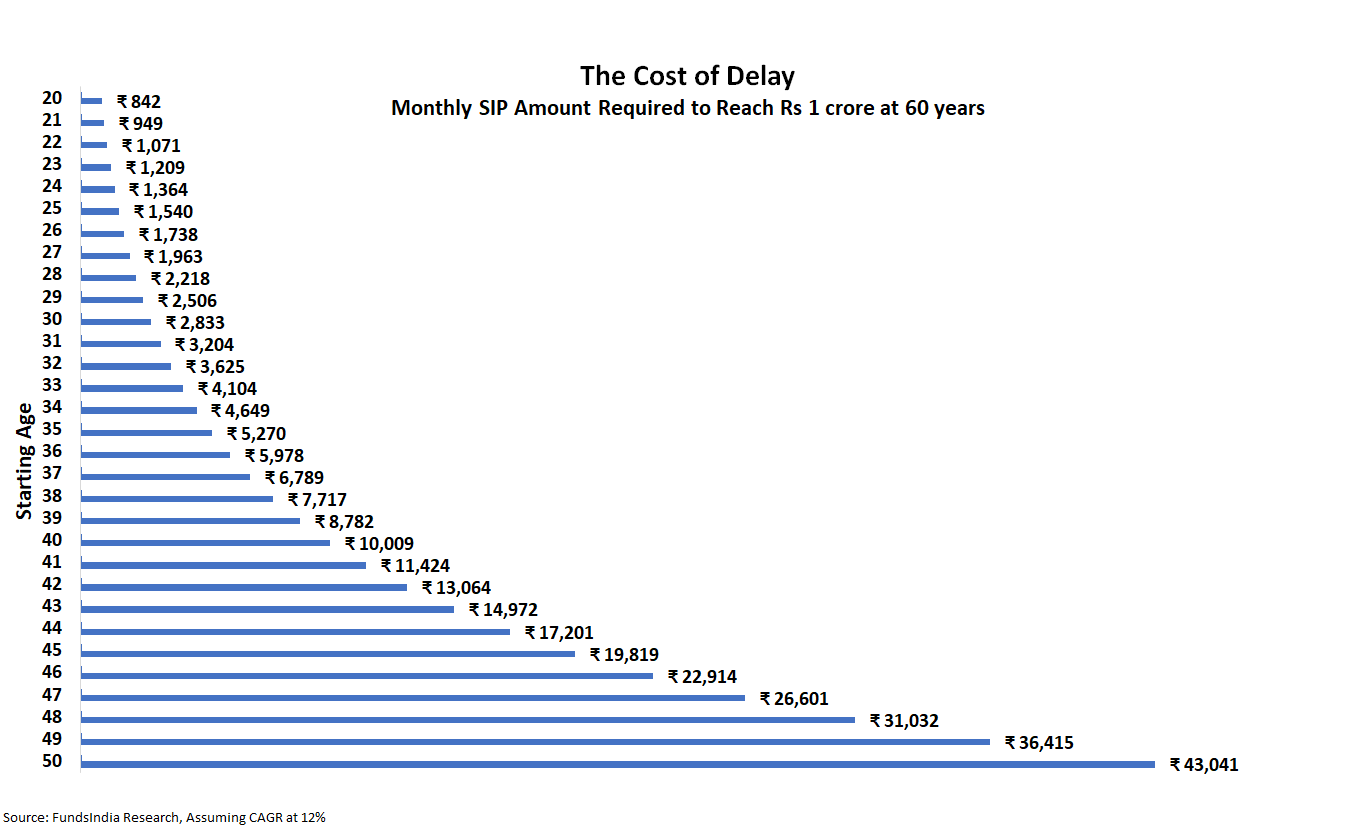

Assume you are in your early 20s. If you need to save up Rs 1 crore at the age of 60 when you retire, can you guess what is the rough monthly amount required to be invested (at 12% portfolio returns)?

Hold your breath. An amount as low as Rs 1,000 to 2,000 per month will get you there!

That’s around 30-70 bucks per day – less than what you pay for your daily chai!

Yes, if you had started investing early, around the age of 20 – 25 the monthly amount required to have a corpus of Rs 1 crore at the age of 60 is around Rs 1000 to Rs 2000.

And if you had started around the age of 25 – 30 the monthly amount required to have a corpus of Rs 1 crore at the age of 60 is around Rs 2000 to Rs 3000.

Insight 1: Even a small amount makes a big difference if you start early

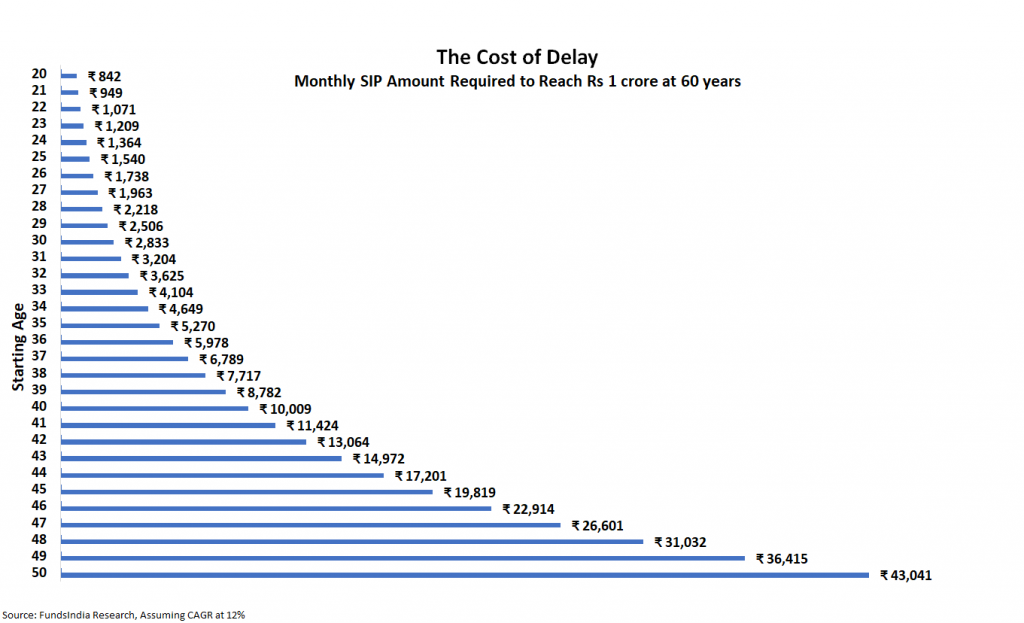

What happens when you delay this decision?

When we delay, the amount required to build the same corpus increases with every delay.

Sample this. If you had started investing,

- At the age of 35 the monthly SIP increases to Rs 5,000, this is 5X more the amount required at the age of 20

- At the age of 40 the monthly SIP increases to Rs 10,000, this is 10x more the amount required at the age of 20

- At the age of 45 the monthly SIP increases to Rs 20,000, this is 20x more the amount required at the age of 20

Can you guess what would be the monthly SIP required if you started at the age of 50?

- At the age of 50 the monthly SIP increases to Rs 43,000, this is a whopping 43x more than the amount required at the age of 20

Insight 2: More the delay, higher is the amount required for the same corpus

Hang on…But why does this happen?

You may have guessed this by now…COMPOUNDING.

What is compounding?

Compounding is the process in which interest is calculated on an initial principal sum of money and then further interest is earned on the accumulated interest as well.

Compound interest can be thought of as “interest on the interest”, or in the case of investment funds, as “return on the returns”.

I get it. This sounds very theoretical, but let’s see what this really means to you.

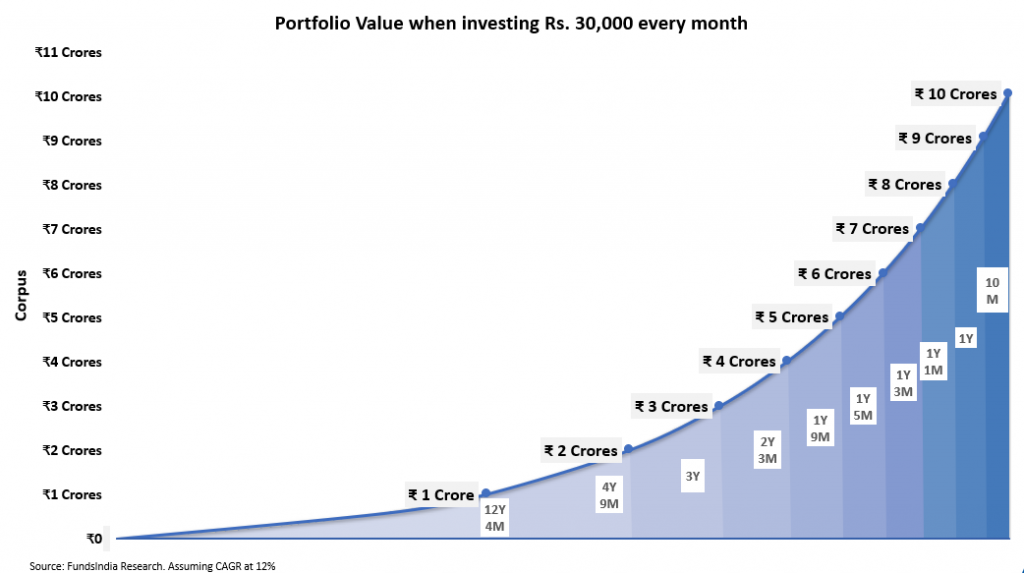

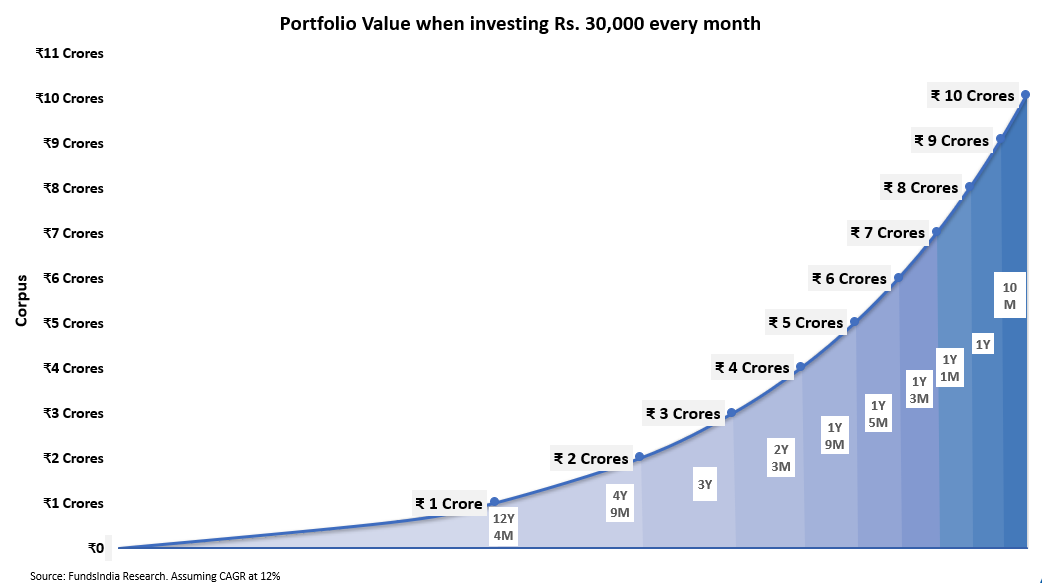

Assume you are investing Rs 30,000 monthly at 12% annual returns.

It takes a painstakingly long 12 years to reach the first crore.

The 2nd crore takes another 5 long years.

And then the power of compounding starts to kick in…

The 3rd crore takes only 3 years!

The 4th crore takes only 2 years and 3 months

And here comes the killer…

… 5th crore takes less than 2 years!

Insight 3: The Power of Compounding happens slowly and then suddenly!

Summing it up

If you’re deciding when to start investing then the answer is simple: START ASAP!

- Don’t wait until your savings become reasonably large to start investing. If you start early, even a small amount can make a huge difference in the long run.

- More the delay, higher is the money to be saved every month for building the same corpus.

- Increase your SIP every year as soon as you get your salary hike.

Remember that…

Power of Compounding is super counterintuitive – it happens SLOWLY and then SUDDENLY!

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}