Company Overview:

With an illustrious history of over 100 years, Tamilnad Mercantile Bank is one of the oldest private sector banks in the country. It was incorporated as “Nadar Bank Ltd” in 1921 and subsequently changed its name to Tamilnad Mercantile Bank in 1962. As on March 31, 2022, the bank has approximately 509 branches, 282 CRMs, 1,141 ATMs, 101 E-Lobbies, and 4,792 PoS across India. They are headquartered in Tamil Nadu and have a strong presence in the state with 72.50% (369) of the Bank’s total number of branches and 83.17% (949) of ATMs. The overall customer base is approximately 5.08 million as of March 31, 2022 and 4.05 million or 79.78% of the customers have been associated with the bank for a period of more than five years and have contributed to ₹35,014.24 crs or 77.93% to the bank’s overall deposits and ₹ 21,902.23 crs or 64.90% to the overall advances portfolios as of March 2022.

Investment Rationale:

Dominant Position: During the last three Fiscals, the overall deposit base of the bank has increased from ₹36,825 crs in FY20 to ₹40,970 crs in Fiscal 2021 to ₹ 44,933 crs in FY22, owing to an increase in both term deposits and CASA deposits. CASA deposits as a share of total deposits have increased from ₹9,518 crs or 25.85 % in FY20 to ₹11,685 crs in Fiscal 2021 or 28.52% to ₹13,705 crs in FY22 or 30.50% with a CAGR of 20.00 % from FY20 to FY22. Bank’s CASA portfolio is diversified and has low concentration with 2.91% of deposits from the top 20 deposit holders and 4.75% deposits from the top 50 depositors as of March 31, 2022.

Consistent Financial Performance: The bank’s reported total income increased at a CAGR of 7.99% from ₹3,992.5 crs in 2020 to ₹4,656.4 crs in FY22. The NIM(Net Interest Margin) has consistently grown over the years with an increase from 3.64% to 4.10% from FY20 to FY22 at a CAGR of 6.13%. The cost-to-income percentage has reduced from 46.10% in FY20 to 42.12% in FY22. TMB reported the second highest Net Profit amongst its Peers of ₹821 crs in FY22 at a CAGR of 41.99% (FY20-22) and a Return on Assets (RoA) of 1.66% which is higher compared to a median RoA of 0.80% for the Peers. In fiscal 2022, TMB reported a low GNPA(Gross Non-Performing Asset) of 1.69% compared with 4.40% for its peers (median). It’s NNPA(Net Non-Performing Asset) is also comparatively low at 0.95%, while its peers clocked a median of 2.10%. At 87.92%, the bank also had the second-highest provision coverage ratio among peers.

Strong Loan Portfolio: TMB’s advances portfolio primarily consists of lending to (a) Retail customers; (b) agricultural customers and (c) MSMEs (“RAM”). During FY20, FY21, and FY22, MSMEs(Micro Small and Medium enterprises) contributed 37.92%, 39.08%, and 37.38% respectively to the total advances with a CAGR of 8.55% from March 31, 2020 to March 31, 2022. For the same period, agricultural customers contributed 24.77%, 27.41%, and 29.70% respectively to the total advances with a CAGR of 19.70% from March 31, 2020 to March 31, 2022.

Key Risks:

RBI curbs on expansion – The roots of the curbs on TMB date back to January 2016, when its shareholders decided to raise its authorized share capital to ₹500 crs. The RBI noted in June 2019 that the bank did not raise its subscribed capital to at least half of the authorized capital as required, prompting it to impose restrictions, including on opening new branches. While some curbs were removed in March 2021, the one on branch expansion remains.

Legal Proceedings – According to the bank’s disclosures, 37.73% of its paid-up equity share capital or 53.59 million equity shares are subject to outstanding legal proceedings pending at various forums. In connection with these shares, regulatory authorities, including the RBI and the Directorate of Enforcement, have initiated proceedings against the bank.

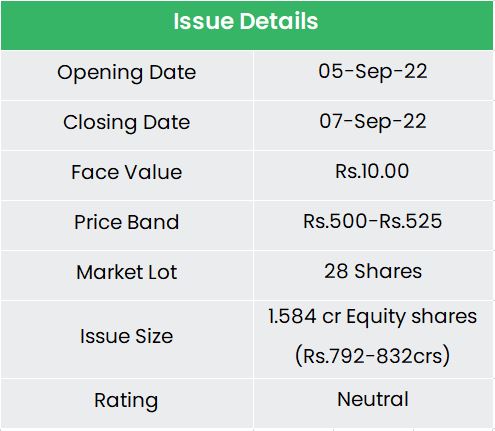

Outlook:

A professionally managed bank, Tamilnad Mercantile Bank does not have a promoter or members that form part of a promoter group. Additionally, it also does not have any shareholders who individually or as a group control voting rights of 15% or more in the bank. Like most banks, Tamilnad Mercantile Bank also needs to perpetually raise capital to maintain its Tier-1 capital ratio. That is the main purpose of this fresh issue. In addition, since Tamilnad Mercantile Bank is currently unlisted, they would also be looking at deriving the benefits of listing in the form of better visibility, reach, and a more market-based valuation for the bank. The total indicative market cap of Tamilnad Mercantile Bank post issue would stand at around ₹8,313 crs and the stock will be trading at a 9.10x P/E on FY22 EPS of Rs.57.67, considering the upper price band of ₹525. Though the company has a strong financial performance than its peers, the RBI-related and other management issues remain key risks. Hence, we provide a ‘Neutral’ rating for this IPO.

Other articles you may like

{kind=link}