The topic du jour lately has been a housing market on the edge of disaster.

But no one can quite agree whether it’s an affordability crisis, home price normalization, a housing correction, or an even-worse impending housing crash.

The takeaway is that home price gains are cooling, and could in fact begin falling as well, after some record years of appreciation.

This isn’t a huge shock, given the fact that the 30-year fixed basically doubled since the start of the year.

It doesn’t take a genius to figure out that the combination of sky-high home prices and much higher financing costs will dent demand. But is a housing crash really coming?

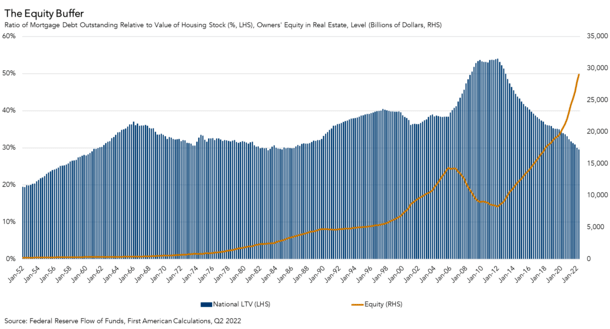

The National Loan-to-Value Ratio (LTV) Is a Ridiculously Low 29.5%

As I’ve pointed out for a while, pundits and casual observers love to compare now to 2006-2008, when the housing market last crashed.

After all, why not just say history is repeating itself, and look to the most recent example to make your argument.

But there are stark differences between now and then, which I’ve shared on several occasions recently.

For example, back then most home buyers (and existing homeowners) had a loan-to-value ratio (LTV) of 100% or more.

Yes, or more. Because many homeowners also elected to take out pay option ARMs, which allowed negative amortization. That is, borrowing more than the home was worth.

We all seem to remember what happened next, since a lot of folks are now calling for the same widespread destruction.

But consider this. As of the second quarter of 2022, the national LTV was just 29.5%, the lowest number since 1983, per First American economist Odeta Kushi.

In other words, the average homeowner only held a mortgage balance worth about 30% of their current property value.

So on a $500,000 property, we’re talking a $150,000 outstanding loan balance. That sounds like a pretty good buffer.

Even if home prices were to fall 10-20%, whatever the number, they’d have quite the cushion to weather the storm.

Say that same $500,000 home falls to $400,000. That $150,000 loan balance still works out to an uber-low 37.5% LTV.

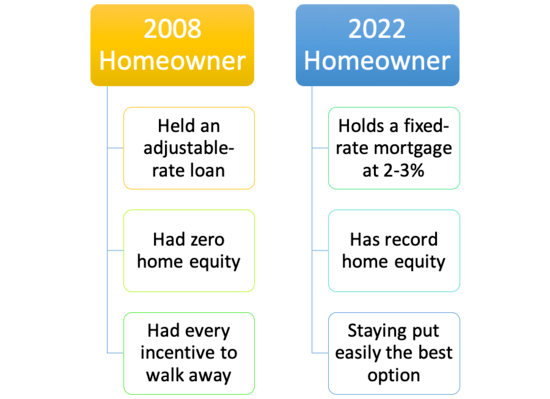

Oh, and this hypothetical homeowner likely has a 30-year fixed-rate mortgage in the 2-3% range. In other words, an ultra-low monthly payment and something they will want to surely hang onto.

Compare this to the homeowner in 2008 who had an option ARM with an adjustable rate that adjusted higher and zero (or even negative) home equity.

Today’s Homeowner Is Not Your 2008 Homeowner

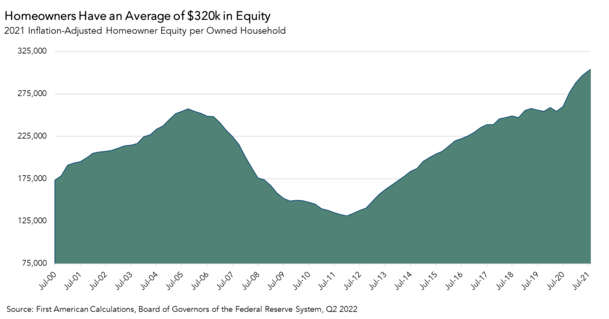

The Average Homeowner Has All-Time High Home Equity

Speaking of home equity, Kushi also shared a chart that revealed the average homeowner had $320,000 in inflation-adjusted equity as of Q2 2022.

This is an all-time high, and the annual growth from Q2 2021 was also “historically high,” despite recent slowing.

But again, this shows you the absurd amount of home equity most homeowners are sitting on at the moment.

And yes, if home prices do drop, their home equity will decline as well. However, it would take a pretty severe downturn to create problems for most.

This isn’t to say that recent home buyers are in the same boat – they might be in more precarious positions if they bought at/near the “height of the market.”

For them, they might not have much home equity, especially if they put little down. These are the homeowners who are probably most at risk if a housing downturn materializes.

But they likely represent a small proportion of the overall market, which as illustrated above, is in pretty good shape.

Still, the housing bears will say this sky-high home equity is fleeting, and destined to disappear, soon.

Of course, it would take something big to erase all that equity, and again, these homeowners also have ridiculously cheap 30-year fixed mortgages at their disposal as well.

Two huge things working against the 2008 housing bear logic. This isn’t to say home prices don’t “correct” or “moderate” or whatever you want to call it.

But a housing crash seems a far-out prediction at the moment. If all the single-family home investors decide to sell en masse for some reason, then maybe you have more downward pressure.

Still, today’s homeowner is in a great spot, even if they are forced to sell unexpectedly.

{kind=link}