Semiconductors have gone from being an essential component of computers to being an essential component of almost everything. Machinery, cars, light systems, household appliances, virtually all modern military equipment, and many more, all rely on semiconductors to function. For example, the average modern car use no less than 1,200 chips[1].

Unsurprisingly, the semiconductor industry is making a massive amount of money. That attracts investors, but many are deterred by the highly technical terminology and the sheer complexity of the industry. Investing in semiconductors is challenging.

Let’s take a closer look at some key considerations for investing in semiconductor companies.

Semiconductors Explained

What Are Semiconductors

Instead of giving a scientific explanation (you can read one here), I will give you a more practical one. Semiconductors provide instructions or computing power to electronic components. They are made from silicon wafers, which are engraved to create the final chip.

How are They Made?

The production of semiconductors requires extreme precision. Many modern chips are manufactured at the nanometer scale (one-millionth of a meter). This means working literally at the atomic level, and in a situation where one atom at the wrong spot can spoil the whole chip.

This work needs to be done in a “clean room” environment with absolutely no dust or pollutant of any kind. Keeping such conditions requires very expensive facilities.

This also requires very specific machinery, each working at one step of a very long and complex process. In this context, R&D and manufacturing are the hard part: the raw material costs count for almost nothing.

A key metric in the manufacturing of chips is yield. This is the measurement of how many functional chips are made from each wafer. While this is inevitable that a few chips have defects, high yields are crucial in keeping a facility productive enough to keep costs low.

Types of Chips

Semiconductors have been around since the 50s. Over time, the trend is miniaturization, with more and more transistors (the base component of a chip) pilled up in one spot. The industry operated under the empirical Moore’s law: transistor density doubles every 2 years.

For this reason, chip generations are traditionally labeled according to the scale at which the manufacturing is done. The smaller, the more advanced the chip. So a 28nm chip is a lot less sophisticated than a 10nm or 7nm chip. Also, the smaller the chip, the harder it gets to reach the next step and keep Moore’s law valid.

Currently, most of the chips being used outside of IT and the computer industry are from older generations, chips in the 28nm range or more. This is because those chips deliver enough computing power for most applications, while also being older and much cheaper technology.

More advanced chips, at 14nm and lower are considered the most advanced. The industry peak is currently 5nm chips, with massive efforts made to reach the 3nm or even 2nm level and manage to mass produce these ultra-small chips[2].

The most advanced chips require new and unique manufacturing techniques, notably Extreme Ultraviolet Lithography (EUV). This is currently the monopoly of only one equipment manufacturer, the Dutch ASML.

Export of this technology to Chinese manufacturer have been banned under the Trump administration, in order to keep China lagging behind and dependent on Taiwan’s chip manufacturers for applications like AI, cloud computing, or self-driving cars.

This ban is still ongoing and is being reinforced under the Biden administration, making it a bipartisan consensus position. Currently, China is judged to be lagging several years behind the US and Taiwan in chip technology.

Still, China seems to have managed to produce a 7nm chip without EUV technology. There is some doubt over whether they can produce these chips at any scale. Still, the race for semiconductor dominance is clearly on between the two superpowers.

Despite these breakthroughs, China remains the world’s leading importer of semiconductors, and China spends more on importing semiconductors than they do on importing oil. This reversal of China’s typically export-intensive economic base underscores the dependence of manufacturing industries on a steady supply of semiconductors.

Overview of the Semiconductor Industry

The Semiconductor Value Chain

Over time, the actors in the semiconductor industry have specialized in just a few steps of the whole value chain. It can be summarized as such:

theoretical research > machinery > design > foundry

theoretical research > machinery > design > foundry

Theoretical research is something done either at the university and research institute level and/or in partnership with the industry. The sector is spending a lot on R&D and is highly competitive. Many patents and intellectual property rights are currently held by the US government or American companies.

The machinery used to manufacture semiconductors is produced by a few specialized companies that sell their equipment to all the manufacturers, subject to restrictions from governments that increasingly see chipmaking as a strategic industry that requires export restrictions.

The chip design industry is split between two types of companies.

- Design-only or “fabless” companies like AMD or Nvidia focus exclusively on the design and subcontract all production to specialist foundries. These are often companies that specialize in a specific sub-sector of the chip sector, like Nvidia for graphic cards/parallel calculations.

- Design+foundry companies, like Intel, design and manufacture chips. They may handle all of their own manufacturing or outsource some to specialist foundries.

The trend in many major companies has been toward the fabless model. For example, AMD spun off its manufacturing business into a new entity, Global Foundries, in 2008, and has been fabless ever since.

Finally, the foundry segment is the actual manufacturing of the chips. The companies doing only manufacturing are called “Pure-play” foundries. Some of them might even offer just a part of the steps needed to produce a chip, outsourcing the rest of the process to another company.

When companies are both designers and manufacturers, they are called Integrated Device Manufacturers or IDMs. This includes for example Samsung, Intel, or Texas Instruments.

The Semiconductor Industry Structure

Because making chips is so complex and expensive, this is an activity that benefits immensely from economies of scale. This has led the industry to turn into essentially an oligopoly, with a few companies holding a dominant position.

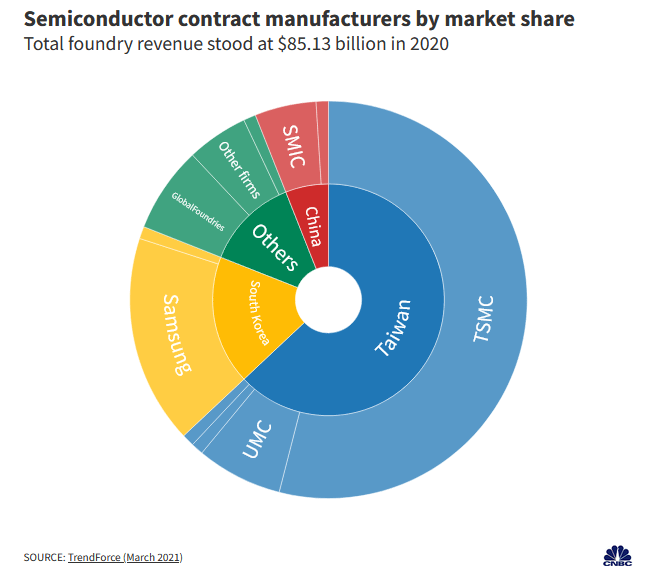

The elephant in the room regarding semiconductors is TSMC (Taiwan Semiconductor Manufacturing Company). By revenue, it controls more than half of the total income of all foundries. The rest of the foundry business is controlled by a few other firms in Korea, Japan, and China, with Western countries lagging far behind.

Semiconductor Geopolitics

As mentioned before, semiconductors have become a geopolitical topic, with the US ban on advanced technology exports to China serving as a prime example But if the US can use semiconductors as a weapon in its rivalry against China, two can play this game.

Currently, most of the world’s semiconductor manufacturing capacity is in Taiwan, an island nation that China officially considers a breakaway province that will be reunited with the mainland sooner or later, peacefully or not. An island which just a few days ago, the USA has warned would be defended by US troops if needed.

So the new big thing for investors in semiconductors is not a new technology, but the need to take geopolitics into account or risk being hurt the way investors in Europe were hurt by the Russian invasion of Ukraine.

92% of 10nm or smaller chips are made by TSMC in Taiwan. The same chips are required for the production of military equipment like satellites or F-35 fighter jets. So Chinese threats on the island are making the Pentagon nervous. A recent naval drill simulating a complete blockade of the island made it worse.

In his meeting with U.S. Defense Secretary Lloyd Austin on the sideline of the Singapore conference, Wei (China’s defense Minister General) declared, “If anyone dares to split Taiwan from China, the Chinese army will definitely not hesitate to start a war no matter the cost.”

He further vowed that China’s People’s Liberation Army (PLA) would “smash to smithereens any Taiwan independence plot and resolutely uphold the unification of the motherland.”

Source: The Federalist

One consequence of this mounting tension is the push to restore chip production to the West. To make it happen, the US Congress voted in August 2022 the CHIPS act, allocating $280B to solve the problem.

On a side note, this is why the Stock Spotlight report of this month is focused on a leading company in the semiconductor industry with production facilities out of Taiwan, that would benefit in the case of a worsening situation.

On a side note, this is why the Stock Spotlight report of this month is focused on a leading company in the semiconductor industry with production facilities out of Taiwan, that would benefit in the case of a worsening situation.

Investing in Semiconductors

The sheer complexity of the product and the process make investing in this industry a daunting task for investors. There are a few strategies that can help you overcome this obstacle.

Focusing on a Narrower Section of the Industry

Short of being an engineer with extensive knowledge about semiconductor manufacturing, it will not be possible for an investor to truly understand the industry as a whole.

It is however possible to learn enough about a subsegment. Maybe focus on learning how just one type of chip (memory, processor, graphic cards, etc.) works and who makes them best. Or focus on a specific level in the value chain. This does not make the learning process much easier, but it’s possible to gain a better understanding than most investors this way, which gives you an edge.

This will also make the competitive analysis a lot simpler, as each of the sub-segment of the semiconductor industry tends to be dominated by 2 to 5 companies at most.

Investing in Semiconductors as a Whole

Because the whole sector is growing strongly, “semiconductors” as a general investment idea can be a winning strategy. Plenty of ETFs and funds offer diversified exposure to the industry. Some will be focused on only US manufacturers, some on Asia, and some on global.

In the same way, you can build a portfolio including all the major actors and count on the winner(s) to be part of your portfolio.

Betting on the Strongest Horse

The industry has a strong flywheel rewarding past success with even more success.

More efficiency or better design lead to more money. The money can be reinvested in more efficient factories or more R&D than the competition. This leads to an even stronger competitive advantage, generating even more profit.

The cycle can repeat again and again until just a few companies are standing.

Such a strong moat makes a compelling argument for investing only in the market leaders.

Conclusion

At first, investing in semiconductors might feel too complex to be analyzed by individual investors. Constant innovation makes it even harder to keep up.

On a second glance, the sector is very structured around just a few key companies, with a strong winner-take-all dynamic. This is together with persistent growth for the industry as a whole for decades past and to come. So investing in semiconductors could prove very rewarding for the patient and astute investor.

Because the industry is so strong, the upside is ultimately taken care of by the growing demand for chips.

Avoiding risk should be the main task of investing in semiconductor companies. Avoiding geopolitical risk means diversifying beyond China and Taiwan. Avoiding technology risk means not betting everything on just one company or one innovation. Avoiding financial risk means balancing the oligopoly structure of the industry with moderate valuation, and avoiding overpaying.

Industry Primers

The process of analyzing a company varies considerably from industry to industry. Many industries have their own vocabularies and specific concerns that investors need to consider. This series of articles looks at specific industries and at industry-specific factors that affect investments. The goals are to highlight specific risks, clarify confusing terminology and explain industry-specific metrics for valuation. These methods complement the usual evaluation process, they don’t replace it.

{kind=link}