Sales of new single-family homes bounced higher in August, jumping 28.8 percent to 685,000 at a seasonally-adjusted annual rate from a 532,000 pace in July. The August gain was only the second increase in the last eight months, leaving sales down 18.4 percent from the December 2021 level and 33.9 percent from the August 2020 post-recession peak. August sales are close to the 50-year average selling rate (see first chart).

However, the surprising result is unlikely to be sustained in the coming months. The National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in September, coming in at 46 versus 49 in August. That is the ninth drop and the second month below the neutral 50 threshold. The index is down sharply from recent highs of 84 in December 2021 and 90 in November 2020.

According to the report, “In another sign that the slowdown in the housing market continues, builder sentiment fell for the ninth straight month in September as the combination of elevated interest rates, persistent building material supply chain disruptions and high home prices continue to take a toll on affordability.” The report adds, “In another indicator of a weakening market, 24% of builders reported reducing home prices, up from 19% last month. Builder sentiment has declined every month in 2022. Due to tightening monetary policy, mortgage rates increased above 6% last week, the highest level since 2008, which is pricing buyers out of the market. In this soft market, more than half of the builders in our survey reported using incentives to bolster sales, including mortgage rate buydowns, free amenities and price reductions.”

All three components of the Housing Market Index fell again in August. The expected single-family sales index dropped to 46 from 47 in the prior month, the current single-family sales index was down to 54 from 57 in August, and the traffic of prospective buyers index sank again, hitting 31 from 32 in the prior month.

In August, sales of new single-family homes were up in all four regions. Sales in the Northeast, the smallest region by volume, rose 66.7 percent, sales in the South, the largest by volume, rose 29.4 percent, sales in the West increased 27.5 percent, and sales in the Midwest rose 16.7 percent for the month. Over the last 12 months, sales were down in two of the four regions, led by a 24.0 percent fall in the West while sales were off by 21.9 percent in the Northeast. Gains from a year ago were seen in the South (10.4 percent) and in the Midwest (5.0 percent).

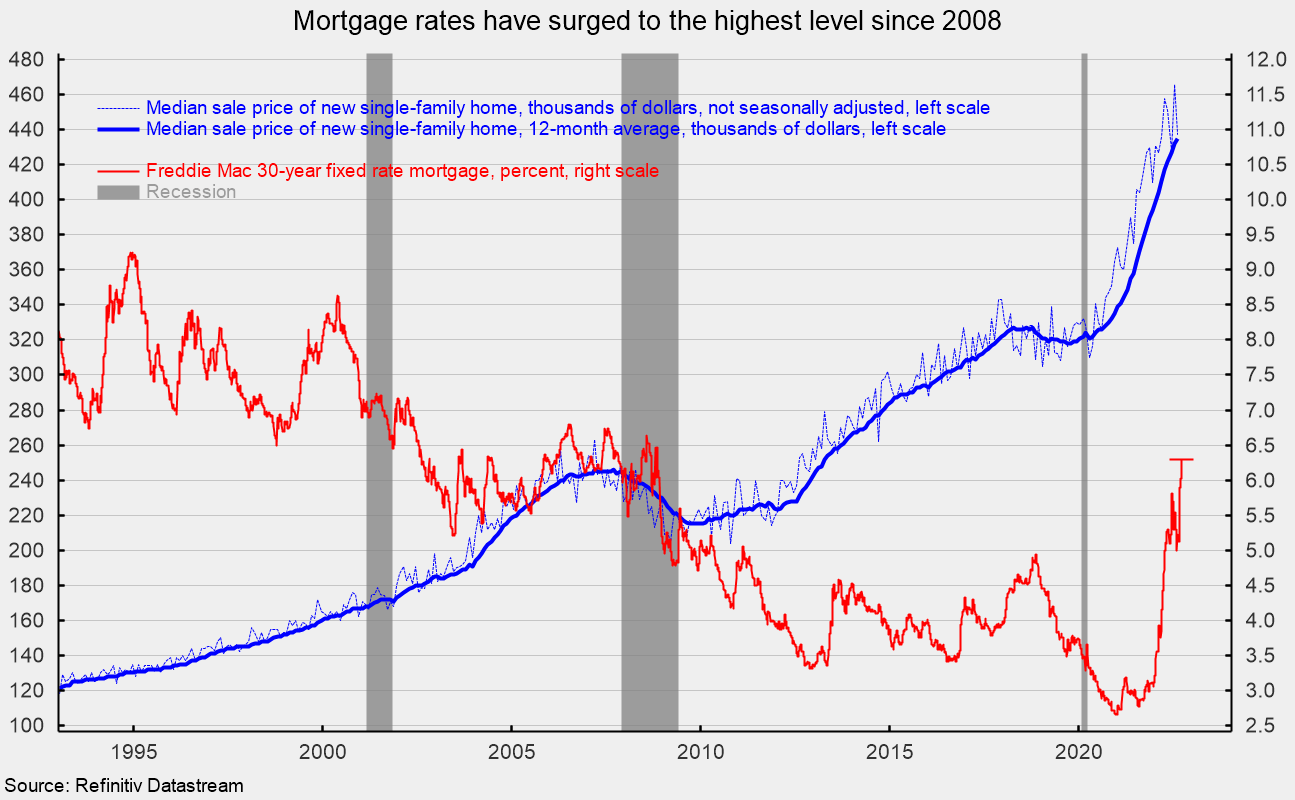

The median sales price of a new single-family home was $436,800 (see second chart), down from $466,300 in July (not seasonally adjusted), putting the 12-month average price at a record high $435,000 (see second chart). Meanwhile, 30-year fixed rate mortgages were 6.29 percent in late September (and around 5.13 percent in late August), up sharply from a low of 2.65 percent in January 2021. The combination of high prices and rising mortgage rates reduces affordability and squeezes buyers out of the market.

The total inventory of new single-family homes for sale rose 0.4 percent to 461,000 in August, the highest since March 2008. That puts the months’ supply (inventory times 12 divided by the annual selling rate) at 8.1, down 22.1 percent from July, but 24.6 percent above the year-ago level. Inventory and the months’ supply remain very high by historical comparison (see third chart). The high level of prices, elevated inventory, and surge in mortgage rates should continue to weigh on housing activity in the coming months and quarters. However, the median time on the market for a new home remained very low in August, coming in at 1.7 months versus 2.4 in July.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}

{kind=link}