Throughout the spring of 2021, the prices of Pokémon trading cards and boxed sets were soaring. Sales of the cards exploded to nearly 600 percent over the previous year’s level. Not only did this take place during the franchise’s 25th year anniversary, but also amid pandemic mitigation policies where individuals around the world began rediscovering their childhood collections. Noticing the prices and wanting to jump into the hype, nostalgic individuals joined the trading community armed with stimulus payments, CARES Act unemployment boosts, Payroll Protection Program (PPP) funds, and lockdown savings.

Professional card graders responded to the surge in prices and trading interest, providing valuations for cards of varying qualities. These valuations, indicative though they were, provided a basis for speculative fervor and led to growing participation in the mania.

How Bubbles Inflate

When determined via market processes, interest rates give producers clues regarding consumers’ preferences for current versus future consumption. Changes in the rate of interest, among other factors, influence the decisions of entrepreneurs and business executives alike. A falling interest rate generally signals the accumulation of savings, which primarily spurs production and the lengthening of production processes.

When central banks adopt expansionary policies, interest rates tend to fall. Business owners may misinterpret the monetary policy-driven decline in interest rates for an increased propensity to save. The latter suggests a declining bear-term time preference among consumers, and consequently a higher propensity to consume in the future. Producers responding to this interpretation of falling interest rates (or firms that compete with those that do) are inclined to initiate new projects or invest in longer term production processes in anticipation of future consumption. As the expansionary policy continues, firms bid up factors of production. Over time, asset prices in familiar markets (such as that of stocks and bonds) and in more speculative activities (such as involving collectibles and engaging in gambling) rise.

This, however, is an artificial boom. It grows out of monetary policy and not consumers’ shifting inclinations towards future consumption. Monetary-policy-fueled booms end when the credit expansions end. This results in the characteristic cluster of error: the sudden appearance of precipitously falling prices, stalled projects, and firms going out of business. Unemployment usually rises as economic output falls. Plans initiated as a result of misleading signals of expansionary policies may be canceled, truncated, or sold to other firms. While lamentable, the exposure and liquidation of malinvestment is a healing process. And just as prices of collectables, whether art, vintage autos, luxury sneakers, or trading cards, surge in tandem with burgeoning economic fortunes during the boom, prices of these items collapse during the bust.

The Covid Credit Expansion

The current inflationary draft began early in 2021 on the heels of 2020’s colossal fiscal and monetary policy programs. Pandemic mitigation policies, including lockdowns and stay-at-home orders (to “flatten the curve”), threatened a massive economic contraction. Consequently, a wide variety of programs intending to supplement lost income, maintain consumption, and provide liquidity to financial markets were put into action.

As the credit expansion proceeded throughout 2020 and into 2021, the prices of financial assets grew rapidly. The S&P 500 rose 16.26 percent in 2020 and 26.89 percent in 2021. The NASDAQ Composite rose 42.48 percent in 2020, 21.4 percent in 2021. Starting from roughly $5,000 in March 2020, the Bitcoin price surged to an all-time high of $65,000 in November 2021. During 2021, home prices also rose 16.9 percent to their highest level in over 20 years. Spending on non-fungible tokens (NFTs) rose over 37,000 percent as $106 million in purchases skyrocketed to over $40 billion in 2021. As chronicled at the time, a series of engineered short-squeezes via retail brokerages captured the attention of financial news media beginning in the early months of 2021 and continuing throughout the year.

As widely reported, Pokémon cards and box sets saw prices catapulting into the tens and even hundreds of thousands of dollars.

The Update

The first and second quarters of 2022 showed 1.6 percent and 0.6 percent contractions in US GDP, signaling the start of a recession. Yet even before the Federal Reserve began raising interest rates in March 2022, contracting credit to combat the most alarming increase in inflation in 40 years, asset prices began falling.

Year-to-date, the S&P 500 is down over 20 percent; the NASDAQ Composite index is down 28 percent. Bitcoin has fallen from $65,000 to below $19,000. Furthermore, regarding the NFT market, the Washington Post reported a handful of anecdotes during the past summer, suggesting a widespread contraction in prices of the digital assets.

An NFT of Twitter founder Jack Dorsey’s first tweet, purchased last year by an Iranian crypto investor for $2.9 million, was put up for auction in April, with bids topping out at $280. A token of a pixelated man with sunglasses and hat that sold for roughly $1 million seven months ago brought just $138,000 on May 8. A digital token of an ape with a red hat, sleeveless T-shirt and multicolored grin — part of the popular Bored Ape Yacht Club — purchased for over $520,000 on April 30, was sold for roughly half that price 10 days later.

Moreover, suspicions that the 2021 froth in NFTs was derivative of the 2020-2021 crypto bubble have been voiced:

[M]ultiple crypto experts have also noted that the precipitous drop in cryptocurrency has caused the market for high-end NFTs — ones that sell for thousands or even millions — to stall. Fewer bitcoin millionaires, they said, means less spending on luxury purchases like high-priced NFTs.

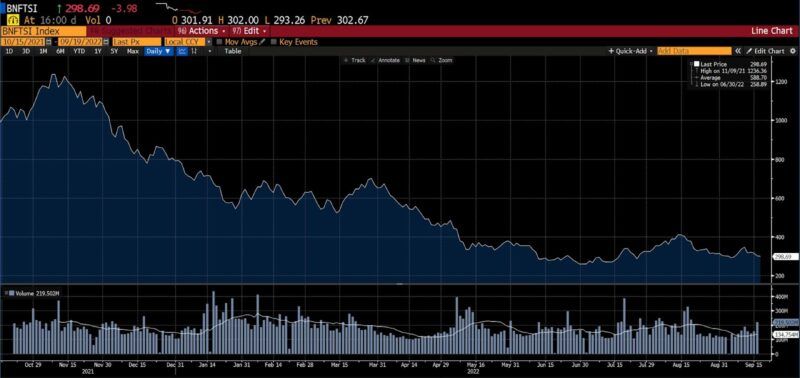

While there are no indices exclusively tracking NFT prices, the BITA NFT and Blockchain Select Index shows a decline of 68 percent between the September 2021 establishment of the index (900.57) and early this week (288.23).

BITA NFT and Blockchain Select Index (Oct 2021 – present)

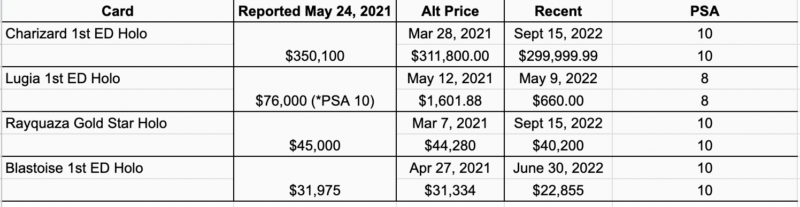

This leads to an update of the March 2021 article Pocket Monsters Meet Animal Spirits. Owing to inconsistent pricing and unreliable dating of Pokémon cards, prices reported in the original article have been checked and alternate estimates added. Nevertheless, there are strong indications that both the appraised and realizable values have slipped substantially along with other assets as demonstrated in the following tables.

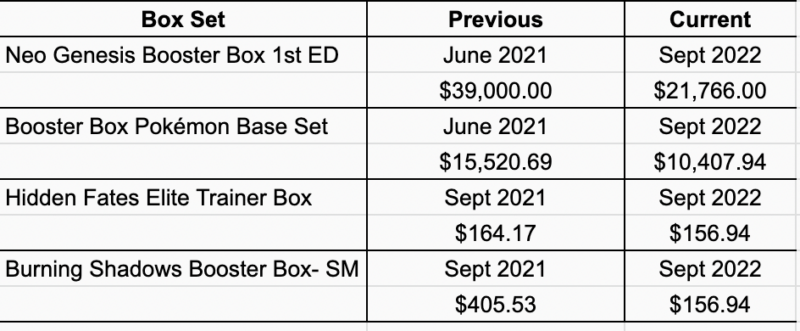

The decreasing price trend in Pokémon card valuations are visible in box sets as well.

Further, in early 2021 McDonald’s released limited-edition Pokémon cards in their Happy Meals, through which individuals could discover cards such as a Holographic Pikachu worth $51.07 in March of that year. Now, that same card is worth $16.88, a 67 percent decrease in value.

Manifestations of even higher risk appetites within the Pokémon card collecting realm, including prices of fractional “shares” of physical cards, should be watched closely as well. (Questions regarding the starting valuations of the cards divided into fractional shares have been raised as well.)

Central banks around the world are still in the midst of their hiking cycle, and the current persistence of inflation suggests that the rate hiking cycle could take substantially longer than originally estimated. The market assessed implied policy rate for the Federal Reserve, as of this writing, is 4.50 percent six months from now. That contemplates a substantial ratcheting up of the current credit contraction.

6 Month Market Implied Policy Rate (Sept 2021 – present)

With respect to the topic at hand, certain Pokémon cards may retain their value longer than others, owing to scarcity and other vagaries in that market. This article serves only to bring the original up to date. It appears that at this time, the effect of contractionary monetary policies upon asset prices is being reflected in Pokémon cards, boxed sets, and related collectables.

Peter C. Earle

Peter C. Earle is an economist and writer who joined AIER in 2018. Prior to that he spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area, as well as running a gaming and cryptocurrency consultancy. His research focuses on financial markets, monetary policy, the economics of games, and problems in economic measurement. He has been quoted by the Wall Street Journal, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications. Pete holds an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point. Follow him on Twitter.

Selected Publications

“General Institutional Considerations of Blockchain and Emerging Applications” Co-Authored with David M. Waugh in The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges (forthcoming), edited by Baker, Benedetti, Nikbakht, and Smith (2022)

“Operation Warp Speed” Co-authored with Edwar Escalante in Pandemics and Liberty, edited by Raymond J. March and Ryan M. Yonk (2022)

“A Virtual Weimar: Hyperinflation in Diablo III” in The Invisible Hand in Virtual Worlds: The Economic Order of Video Games, edited by Matthew McCaffrey (2021)

“The Fickle Science of Lockdowns” Co-authored with Phillip W. Magness, Wall Street Journal (December 2021)

“How Does a Well-Functioning Gold Standard Function?” Co-authored with William J. Luther, SSRN (November 2021)

“Populist Prophets, Public Prophets: Pied Pipers of Lucre, Then and Now” in Financial History (Summer 2021)

“Boston’s Forgotten Lockdowns” in The American Conservative (November 2020)

“Private Governance and Rules for a Flat World” in Creighton Journal of Interdisciplinary Leadership (June 2019)

“’Federal Jobs Guarantee’ Idea Is Costly, Misguided, And Increasingly Popular With Democrats” in Investor’s Business Daily (December 2018)

April Liu

April is a Research Intern at AIER. She graduated from Mount Holyoke College in May 2022 with a double major in Economics and International Relations. Her research interests lie in data privacy at global and local scales.

{kind=link}