The final September results from the University of Michigan Surveys of Consumers show overall consumer sentiment was little changed from August and remains at historically low levels (see first chart). The composite consumer sentiment increased to 58.6 in September, up from 58.2 in August. The index hit a record low of 50.0 in June down from 101.0 in February 2020 at the onset of the lockdown recession. The increase for September totaled just 0.6 points or 0.7 percent. The index remains consistent with prior recession levels.

The current-economic-conditions index rose to 59.7 versus 58.6 in August (see first chart). That is a 1.1-point or 1.9 percent increase for the month. This component is just a few points above the June low of 53.8 and remains consistent with prior recessions.

The second component — consumer expectations, one of the AIER leading indicators — was unchanged for the month, holding at 58.0. This component index has shown the strongest bounce over the last two months but is still consistent with prior recession levels (see first chart).

According to the report, “Buying conditions for durables and the one-year economic outlook continued lifting from the extremely low readings earlier in the summer, but these gains were largely offset by modest declines in the long run outlook for business conditions.” The report adds, “…sentiment for consumers across the income distribution has declined in a remarkably close fashion for the last 6 months, reflecting shared concerns over the impact of inflation, even among higher-income consumers who have historically generated the lion’s share of spending.”

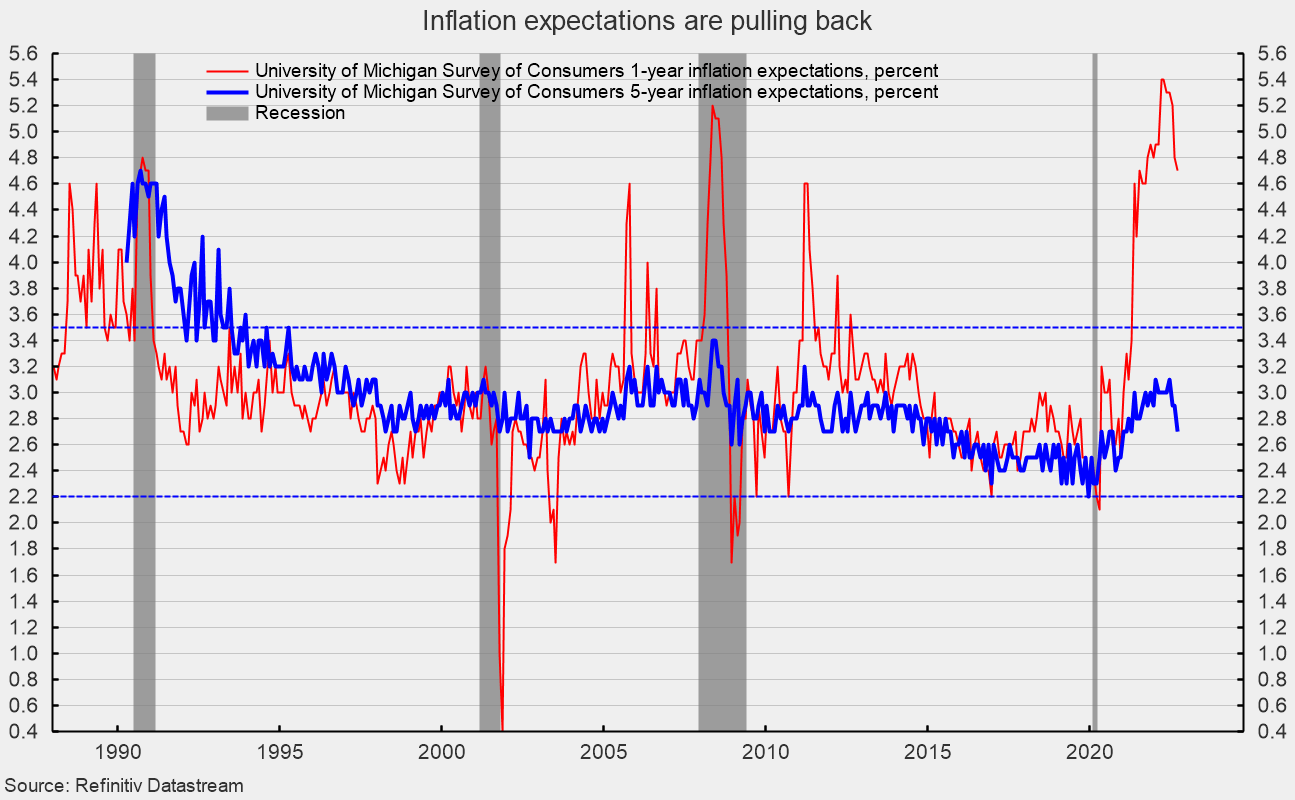

The one-year inflation expectations fell again in September, dropping to 4.7 percent. That is the fourth decline in the last five months since hitting back-to-back readings of 5.4 percent in March and April. The latest reading is the lowest since September 2021 (see second chart).

The five-year inflation expectations also ticked down, coming in at 2.7 percent in September. That result is well within the 25-year range of 2.2 percent to 3.5 percent and the lowest reading since April 2021 (see second chart). The report states, “Inflation expectations are likely to remain relatively unstable in the months ahead, as consumer uncertainty over these expectations remained high and is unlikely to wane in the face of continued global pressures on inflation.”

Pessimistic consumer attitudes reflect a confluence of events, with inflation leading the pack. Persistently elevated rates of price increases affect consumer and business decision-making and distort economic activity. Overall, economic risks remain elevated due to the impact of inflation, an aggressive Fed tightening cycle, and continued fallout from the Russian invasion of Ukraine. As the midterm elections approach, the ramping up of negative political ads may also weigh on consumer sentiment in the coming months. The economic outlook remains highly uncertain. Caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}