Have you recently ordered your credit report? Fabulous — awareness is a great first step toward financial health.

Your credit report is a deep look into your financial history. You might see regular mortgage payments, car loan payments, and even a record of your first credit card.

But what do revolving accounts, inquiries, and public records mean? How does all this fit in with your credit score?

Sit back and let us walk you through the ins and outs of your credit report.

*Note: Some of the images used below were taken from an Equifax credit report and are only meant to be used as helpful examples. Yours might look slightly different if you obtain your report from TransUnion.

What is a Credit Report?

A credit report is a multi-part statement about your loan history, credit activity, and credit account status. Lenders can access your credit report to help them decide whether you’re reliable enough to lend to. Additionally, some employers may access your credit report if you give them permission.

What Does Your Credit Report Include?

Your credit report contains the following insights into your historical and current credit scenario:

Inquiries

Remember when you applied for a mortgage or car loan? Or perhaps you just logged into Equifax to see your score? These are called inquiries. Your credit report shows a list of each inquiry made, the date, and the person or company who made them.

We’ve heard the age-old tale: doesn’t checking my report affect my credit?

Equifax answers the question for you on each inquiry, with a Yes or No column on whether it affects your score.

A pre-approval or personal inquiry won’t affect your credit score. These are called soft inquiries.

But a lender assessing your creditworthiness for a mortgage or car loan? That’s a hard inquiry, and it would affect your credit slightly.

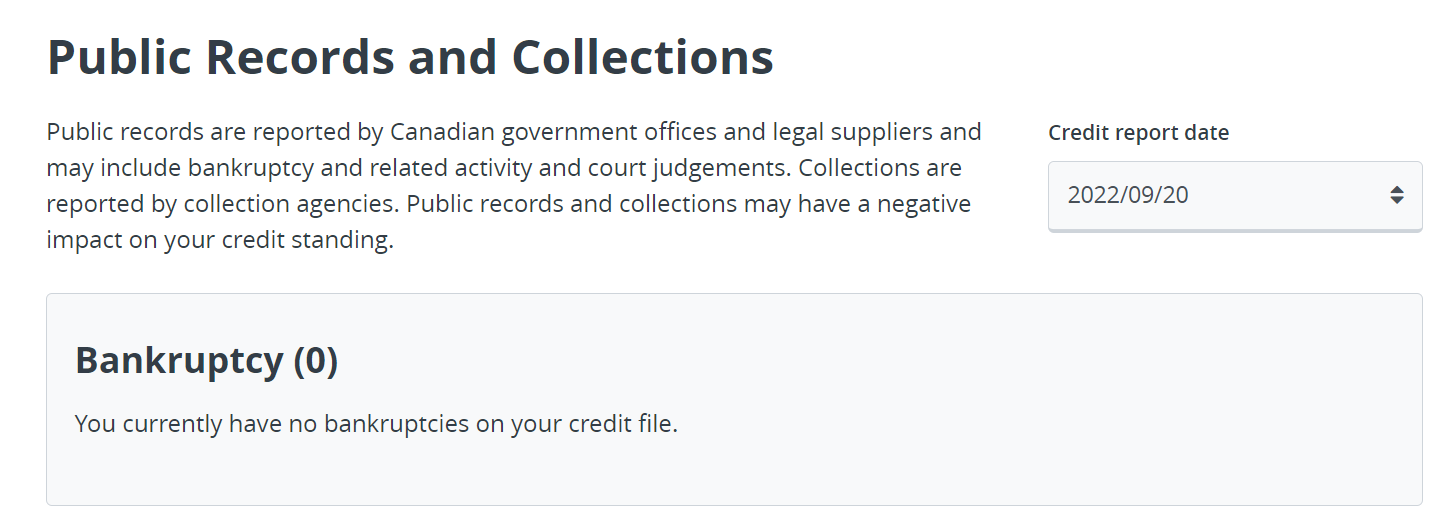

Public Records

Ever filed for bankruptcy? That’ll show up here. Public records are credit-related legal matters viewable by the public. We’re talking:

- Bankruptcy: A legal process in which someone seeks complete relief from every debt at the expense of a damaged credit score and greater difficulty borrowing in the future.

- Liens: A lender’s legal claim on something in your possession (car, real estate property) if you default on a loan.

- Collections: Any debts that went unpaid long enough for a lender to send it to a collections agency.

- Judgments: A legal decision by the courts demanding you repay a debt.

Most of these items will stay on your credit report for a minimum of 6 years.

Secured Loans

Secured loans are loans with collateral. Perhaps you pledged your car or expensive jewellery to obtain a personal loan. If you default, the lender has a legal claim on your collateral. Those loans appear on your credit report.

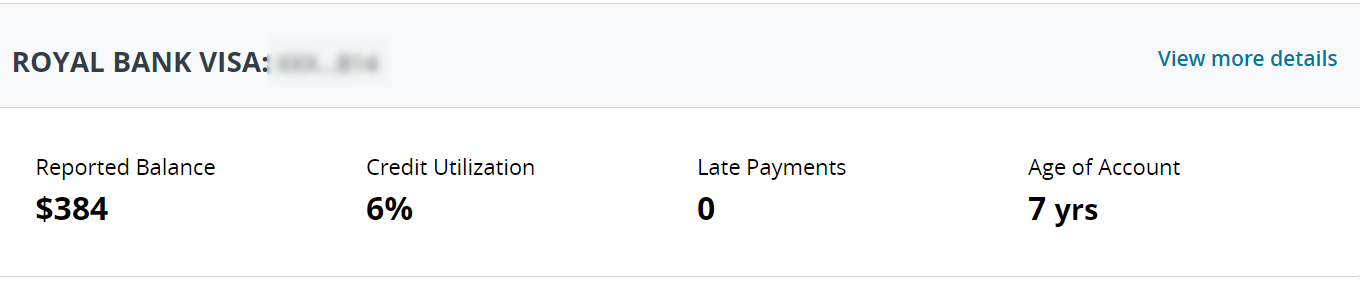

Accounts

Accounts include personal loans, lines of credit, mortgage loans, credit cards, installment loans, and other credit accounts. A history of payments for each one will show up in this section of your credit report.

You’ll probably see the most accounts under the “Revolving Credit” section. These accounts have a limit and minimum payment. If you’re late on your credit card payment, you’ll see it here.

Notice the credit utilization ratio? We’ll talk more about that later.

Personal Information

Credit bureaus have personal details such as your phone number, email addresses, reported addresses, birthdate, and full name. All this shows up on your credit report.

Credit bureaus consider each aspect when calculating your credit score. But some activity affects your score more than others. We already discussed hard inquiries vs. soft inquiries, but what else do credit bureaus consider in calculating your credit score?

How is Your Credit Score Calculated?

Here’s the thing: credit bureaus don’t offer a public formula about how they calculate your credit. However, they do state certain factors that could affect your score:

- Credit history length: Do you only have a series of revolving credit accounts all under two years old? Longer credit history generally improves your credit score.

- Payment history: Late payments could negatively impact your score. Similarly, a long history of on-time payments boost it.

- Credit utilization ratio: This ratio compares your account balances to limits. If you’re stretching every account to the max, your score could dip.

- Public records: Judgments, consolidated debt, and bankruptcy have more negative and long-lasting impacts on your score.

- Inquiries: Multiple hard inquiries can worsen your score.

Review Your Credit Report with a Certified Credit Counsellor

Understanding your credit report is a great way to improve your financial health.

Notice a particularly high credit utilization ratio? Now you’ll be more conscious of using that account.

See a debt that doesn’t seem accurate? You can report it to the credit bureau.

But if your credit report makes you feel overwhelmed, we’re here to help. Our certified credit counsellors have decades of combined experience helping people regain financial freedom after periods of high debt and even bankruptcy.

Our services are completely free. Book a consultation today!

{kind=link}