So it seems like everyone around you has been talking about SGS Bonds and T-bills lately. What are they, and should you follow the crowd who have invested their savings into it? Here’s what you need to know before you make any move.

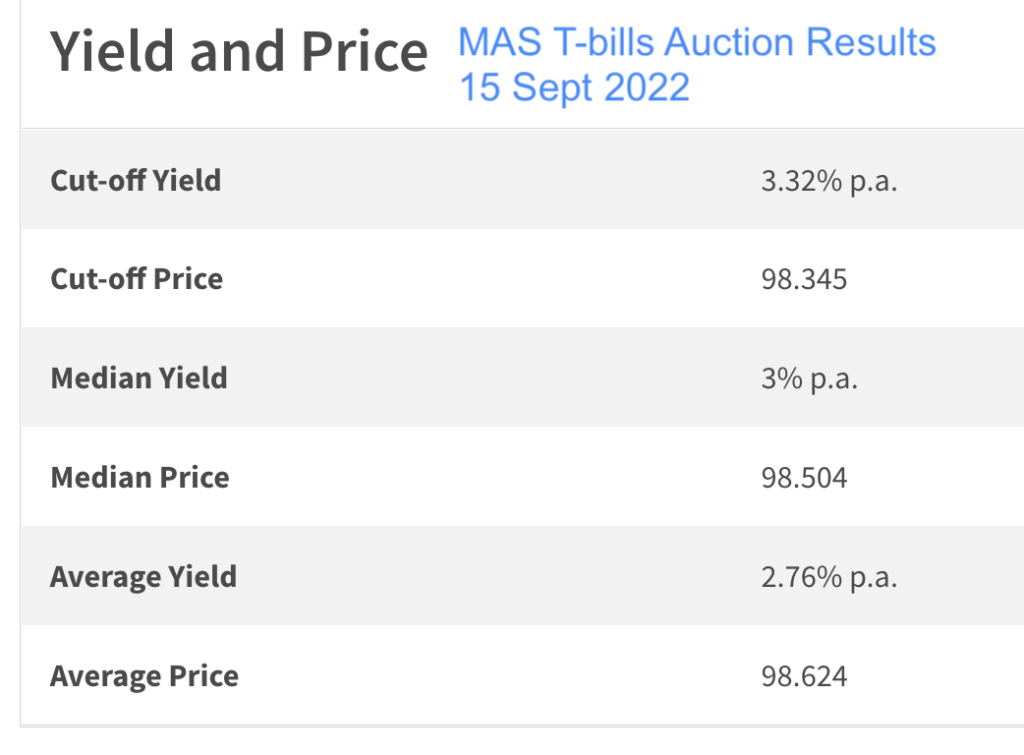

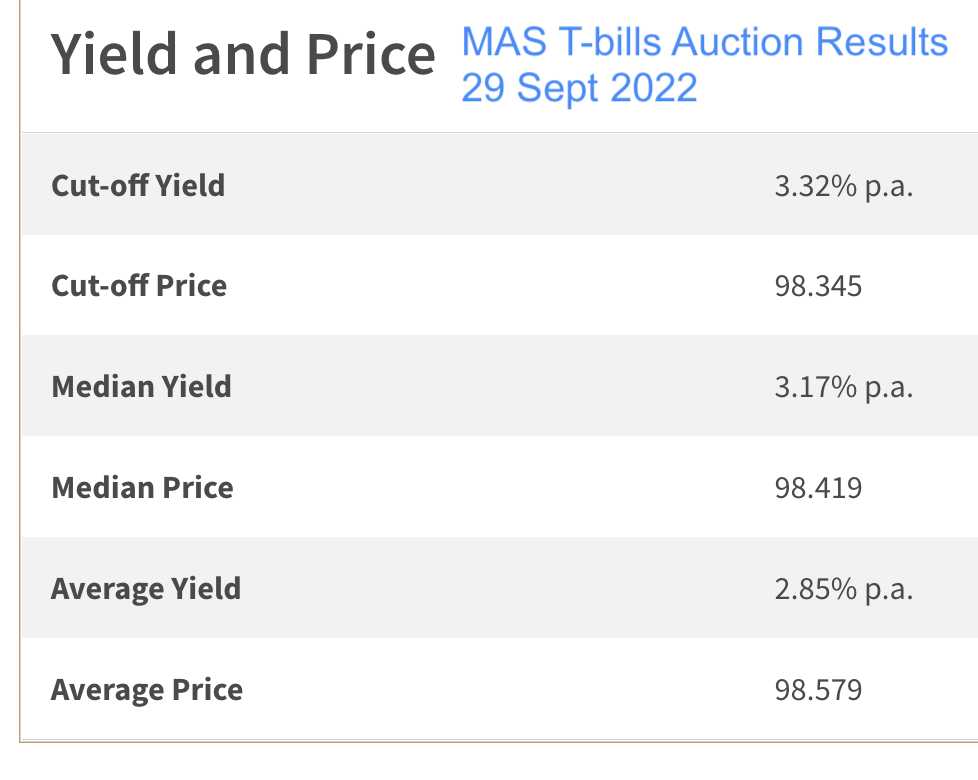

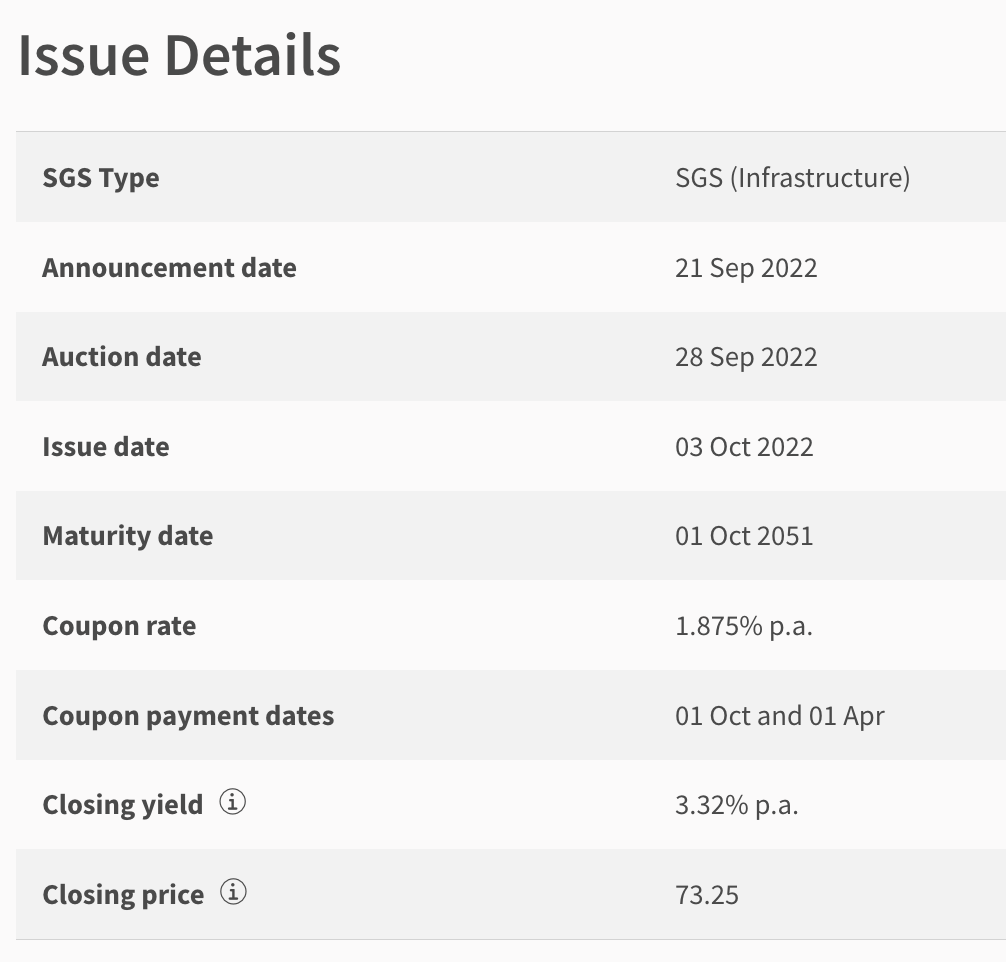

With the latest MAS T-bills cut-off yield at 3.32% p.a., Singapore’s financial scene has been buzzing with talk of it, even among non-investors and folks who have never bought bonds before.

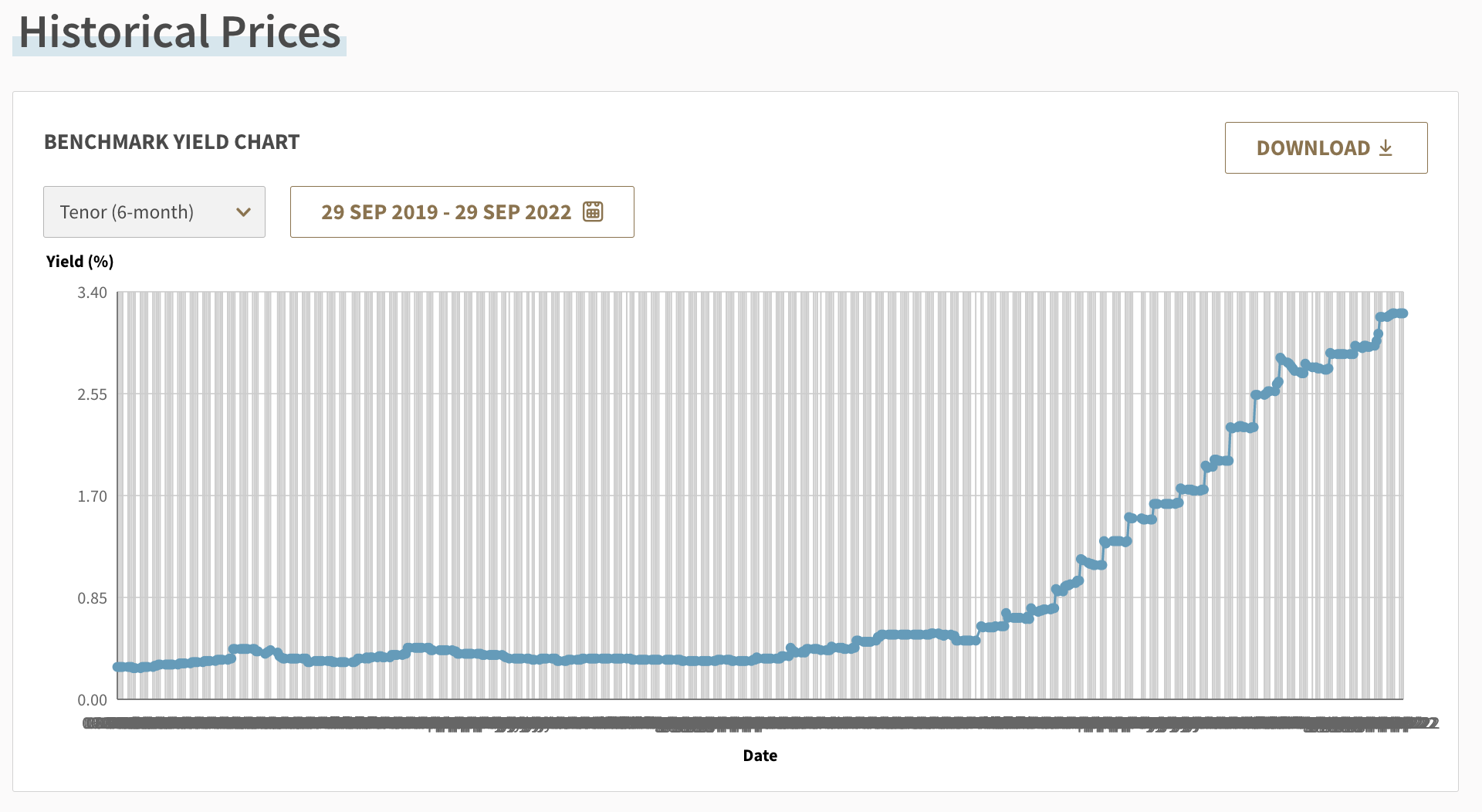

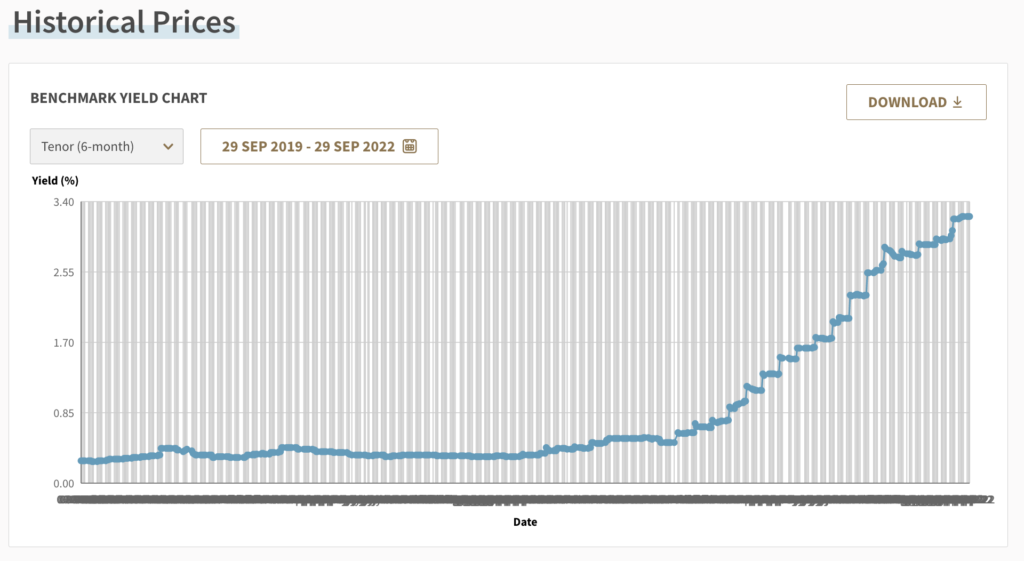

And with rates this high, it is no surprise that almost everyone seems to be excited over the latest T-Bills, where yields have gone up from 0.61% in January to 3.32% p.a. for the latest auctions in September.

At these rates, even the most competitive fixed deposit look like a weaker offering in contrast, especially with a longer lock-up period too. For instance, the highest rate now is 2.8% p.a. offered by RHB Bank for a minimum $20k placement for 24 months, whereas Hong Leong is offering 2.75% p.a. on a deposit of at least $50k for a year.

And as it is, the local fixed deposits are already at their highest since the end of the Asian financial crisis almost 24 years ago.

What are Treasury Bills and Is It Worth Investing In?

Singapore’s Treasury Bills (T-bills for short) are short-term government securities issued at a discount to their face value, in the form of 6-month and 1-year T-bills. As an investor, you receive the full face value at maturity, which means your yield can be calculated as the difference between your bid price and the maturity price.

Simplified Explainer: If you successfully bid for and secured a 6-month T-bill at the rate of 3.32%, your $100k capital would now become $10k + $1,660 after 6 months. If you managed to secure a 1-year T-bill at the same rates, you would have effectively “earned” $3,320. In reality, what would have happened is that you would have paid $96.68 for the bond and gotten $100 upon maturity i.e. you would have paid $96,680 and received $100,000 after 6 months / 1 year, which is where your 3.32% yield comes from.

There hasn’t been much interest in T-bills prior to this year and for good reason: the yields on our local T-bills have remained fairly flat all along (and for the last 3 years), but started rising steeply from the start of this year (in line with the global Fed’s interest rate hikes):

My Take: If T-bill yields continue rising and there’s no news about CPF interest rates being revised higher, I may start to use my CPF funds to buy into some T-bills once yields cross the prevailing CPF rates.

You can easily find out how to apply for T-bills online, so I won’t cover that in this article. However, what are the risks that come with investing in T-bills?

Risks of Investing in T-Bills

Now, if you intend to buy and hold T-bills until maturity, then your risk is almost none – since these T-bills are fully backed by the Singapore government and are to be held for only 6-months or 1-year at most. Unless you think the Singapore government is going to go bankrupt or bail on you within this short time frame…a risk which I think is almost close to zero.

However, if your personal financial circumstances changes abruptly during this (short) period and you suddenly need the cash (before maturity), you will then have to sell them in the secondary market.

This can be done by going to any of the local banks and getting a quote from them.

Continuing on the above example, imagine you have $96,680 locked up in a 1-year T-bill, but you cannot wait until its maturity in 2 months time to get $100,000 because you need the money urgently now. Your bank quotes your $98 (instead of the $100 you were hoping for) and you take it, because you’re desperate. You now get $98,000 instead of the $100,000 you were expecting, taking a $1,320 “profit” instead and letting your bank earn $2,000 because you had to let it go earlier than expected.

T-bills vs. Singapore Government Securities (SGS)

At any rate, T-bills with their shorter maturity are a much better option than SGS bonds, which have maturities ranging from 2 – 50 years.

And while you can technically sell your SGS bonds on the secondary market i.e. SGX by yourself (no need to go through your bank), the market is extremely illiquid i.e. it is harder to find buyers than you think.

T-bills vs. Singapore Savings Bonds

Another option would be to consider Singapore Savings Bonds (SSBs), which are similarly backed by the Singapore government but offer more flexibility i.e. you can redeem your SSB units at any time.

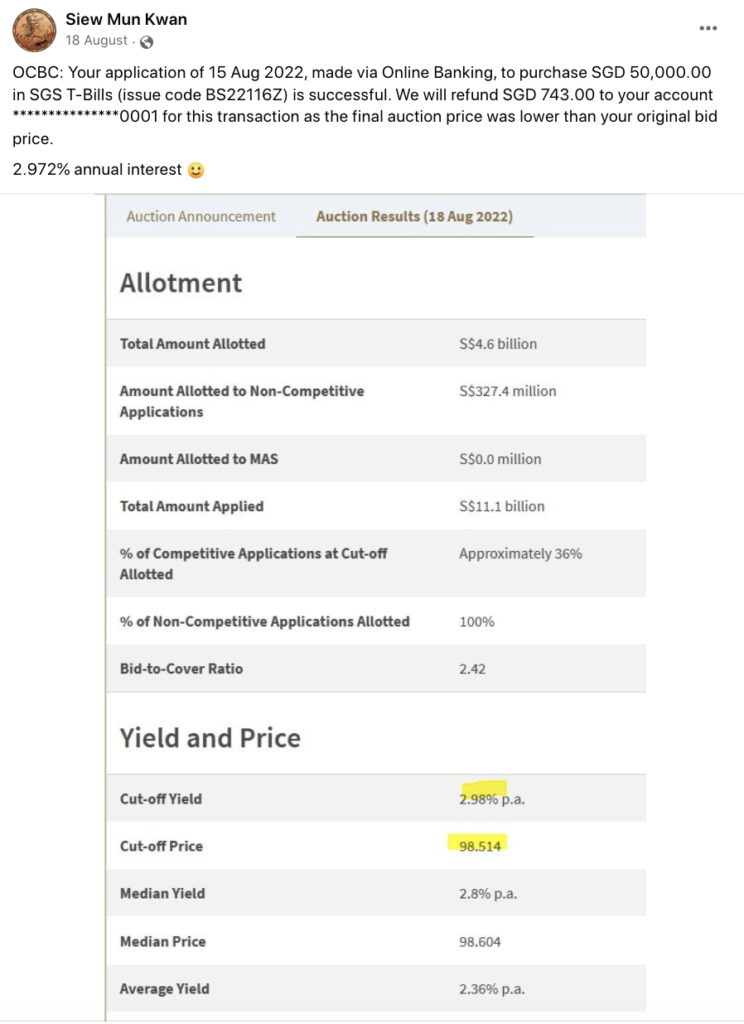

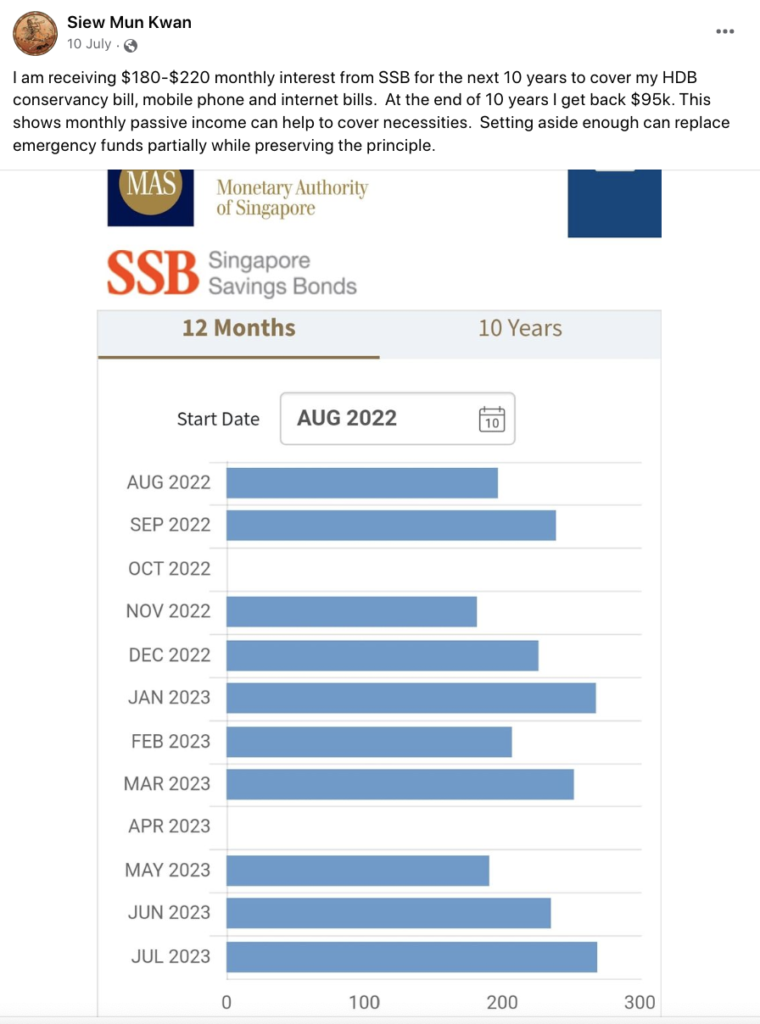

Hardworking folks can try their hands at building a SSB ladder i.e. replicating what this other low-risk investor, Siew Mun, has done:

I started talking about SSBs when they were first launched in October 2015, but as rates were low then (<1% for the first 1-2 years), there was little incentive to really build a SSB ladder back then as it felt like too much work for too little gains.

Today, with rates starting at 2.6% for the first year of SSBs, low-risk investors who prefer to go for safe investments (i.e. no risk of capital loss) can consider this.

However, even holding SSBs for 10 years (currently 2.99%) may no longer be enough to beat inflation. Hence, you may want to diversify into other financial tools instead.

While T-bills are definitely attractive at this point in time, the yields are constantly changing and you have to bid at each auction i.e. there’s no guarantee that you will get it.

If you do, hooray!

And if you tried but haven’t been successful at your prior auctions, another investment tool you can consider are cash management funds – (also known as Money Market Funds (MMFs) – instead.

No, they’re not backed up by the Singapore government, but they generally offer a higher return than fixed deposits while giving you the flexibility to redeem your money anytime with no penalty.

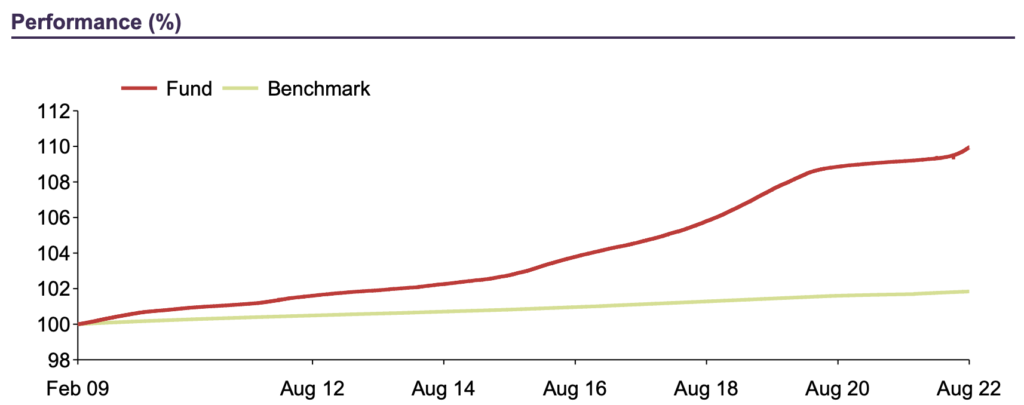

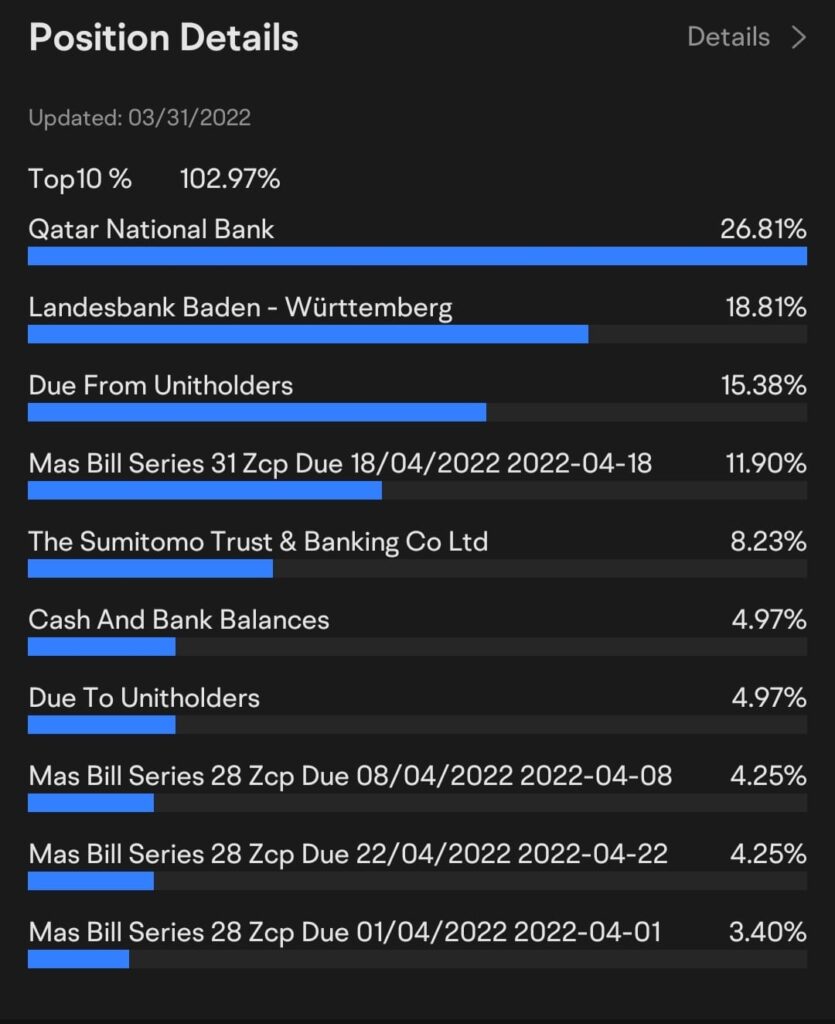

One of the most attractive cash management funds available to Singaporeans is the Fullerton SGD Cash Fund, which is the largest domestic cash fund here and with a proven track record of having consistently beaten its benchmark since its inception in 2009. Despite the risk of price volatility, the fund has never had a negative monthly return throughout its entire operating history.

How has it fared throughout 2022 – the year when growth stocks crashed and of Fed rate hikes? It held up well, as you can see:

Why was this so? The answer can be found in its holdings, as the Fullerton SGD Cash Fund mainly invests in short-term Singapore-dollar deposits with reputable financial institutions. For those who understand ratings, you’ll be pleased to note that these are only instruments with a minimum rating of F-2 by Fitch, P-2 by Moody’s or A-2 by Standard and Poor’s.

Unfortunately, retail investors cannot buy this fund directly – but moomoo has changed this by offering folks like you and me an easy way to invest in the Fullerton SGD Cash Fund – via its moomoo Cash Plus.

And if you’re looking for a USD-based cash management fund instead, check out if the CSOP USD MMF would fit your needs better.

Who’s suitable for T-bills vs. Cash Management Funds?

There are a few main groups of people who would be suitable for such instruments, and I’ve categorized it below:

T-bills

- Beginners who don’t know how to invest, and are dissatisfied with their current savings returns

- Conservative folks who want a safe investment / almost-zero risk options

- Investors who want something backed by the Singapore government

- Investors who do not need the cash in the next 6 – 12 months

Cash Management Funds

- Beginners who don’t know how to invest, and are dissatisfied with their current savings returns

- Folks who want low-risk options, and without the high volatility of equities or forex

- Investors who want to reserve the option of withdrawing their cash at any time with zero penalties

- Seasoned investors who are looking for a flexible place to temporarily hold their warchest cash, while waiting for opportunities in the stock market to appear

To find out more about cash management funds like moomoo Cash Plus, check out this article here, where I dive into a more detailed review of how they work and what you need to know.

And if you’ve always been someone with spare cash who only looked at fixed deposits, check out T-bills and/or cash management funds instead – you might just find that they’re a better, more rewarding option for you.

Important note: Cash management funds like moomoo Cash Plus are NOT the same as T-bills, and their core differences have been outlined in this article. Each instrument has its pros and cons, and it is your responsibility to do your own due diligence further before deciding what to do with your money.

Message from our Sponsor Start investing in funds from S$0.01, with the flexibility to withdraw anytime you want to. With $0 commission, no fees for fund subscription and redemption and $0 platform fees, choose moomoo to help you start your fund investments easily today!

The moomoo app is an award-winning trading platform offered by Moomoo Technologies Inc., a subsidiary of Futu Holdings Limited (NASDAQ:FUTU) and backed by Tencent. Moomoo Financial Singapore Pte. Ltd. is regulated by the Monetary Authority of Singapore and is the first digital brokerage to have received all 5 memberships from the SGX Group for the securities and derivatives markets.

Disclosure: This post is brought to you in conjunction with moomoo SG. All views expressed in this article are my own independent opinions. Neither moomoo Singapore or its affiliates shall be liable for the content of the information provided.

Please feel free to click on my affiliate links if you’ll like to sign up for an account!

This advertisement has not been reviewed by the Monetary Authority of Singapore.

{kind=link}