Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

Bears are beating the bulls this year, but don’t bulls always win?

As share prices continue to fall faster than earnings in almost every country, at some point investors have to say: “OK, things are bad, and in the short term, they might get worse—but these assets and future earnings streams are still worth a lot of money, right?

“Just how much are the assets and future earnings streams worth?” is the real question, when it comes to determining the appropriate current value for a company.

The two charts below were released by Yardeni Research and they illustrate just how low valuations have sunk, relative to future earnings.

I mean, you know it’s rough times when investors are pricing the average P/E (price-to-earnings ratio) of the Big Six Canadian banks at close to 9x.

When you compare where we are today versus how incredibly depressing things looked during the absolute depths of the pandemic or in 2008, I can’t conclude anything other than pessimism might have a little too much control over the steering wheel.

Sure, market bears point to high inflation rates, the China slowdown and the war with Russia in Ukraine. But, realistically, as important as those things are, how does that compare to early 2020? Back when we were experiencing a virus that was on track to kill tens of millions of people? No one could travel, and shopping for groceries was considered a health risk. We were worried about healthcare systems collapsing and unprecedented unemployment numbers—now we have more job openings than workers!

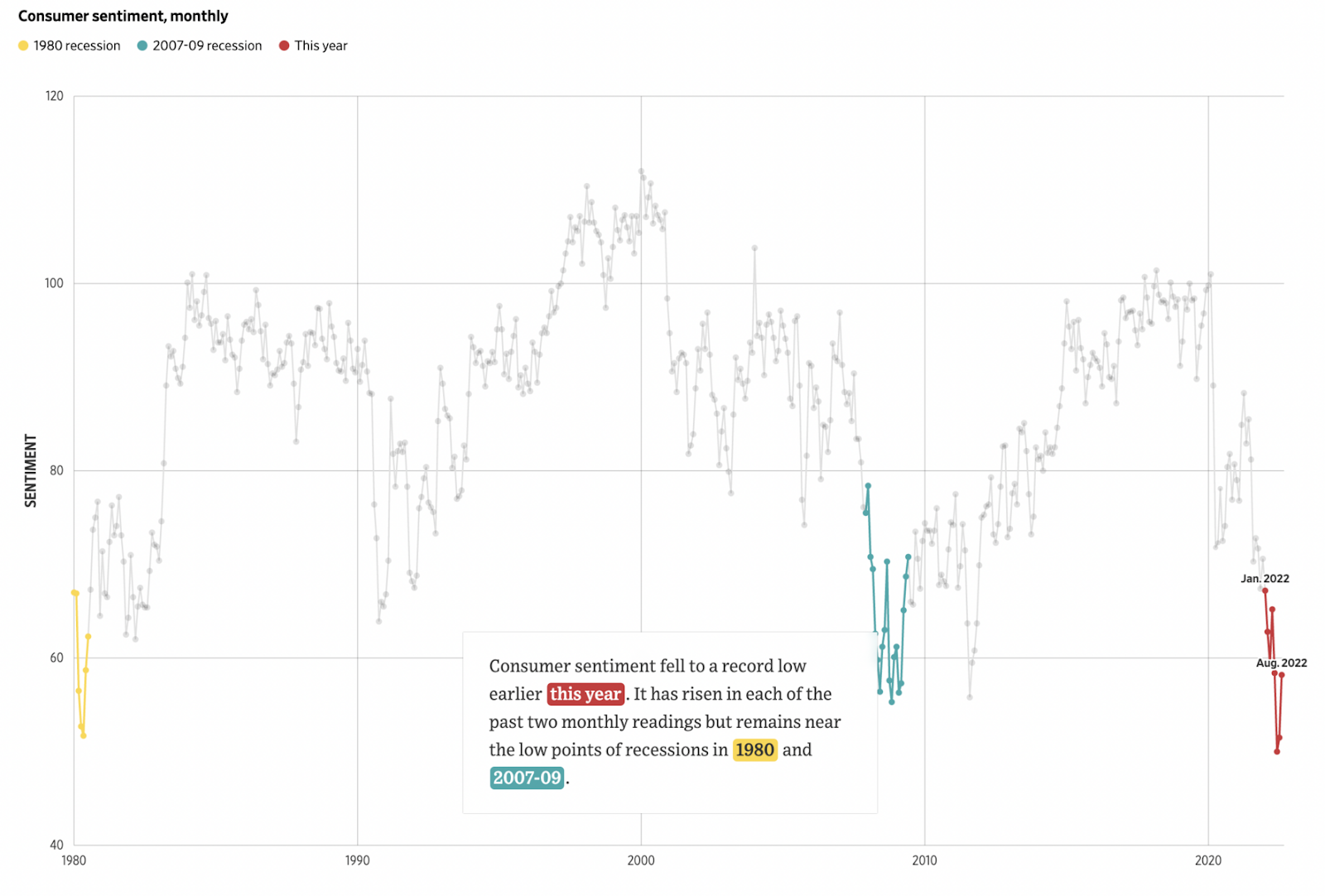

The chart below from The Big Picture illustrates the negative sentiment in the U.S., and I have to think—given the valuations of Canadian stocks—we must be in a similar mindset.

All this negativity and compressed valuations have my contrarian alarm bells going off.

It is incredibly difficult to predict what any market will do in the next six to 12 months. But I do know that 4% interest rates and the prospect of a year of stagnating earnings are not as scary as a novel virus killing one in 30 people.

I’m fairly certain the long-term value of Canada’s giant market-protected companies should be much closer to its average than it currently is, no matter what sort of recession is around the corner. At this point, the share prices of very solid profitable (read: boring, predictable) companies are getting crushed right alongside the riskier tech companies of the world.

Historically speaking, when that kind of thing happens, it’s typically the best time to be confident with Canadian stocks.

Of course, Canada isn’t the only market where investors are expressing doom and gloom. Legendary investing author Jeremy Siegel told CNBC he felt the U.S. Federal Reserve was being too aggressive in raising interest rates so quickly.

“Honestly, I think Chairman Powell should offer the American people an apology for such poor monetary policy that he has pursued, and the Fed has pursued, over the past few years.”

I believe this counts as “calling someone out” in the zipped-up world of academia!

Note: You can hear my in-depth thoughts on the current bear market at the 2022 virtual Canadian Financial Summit, beginning on October 12. I’m joined by esteemed MoneySense colleagues Jonathan Chevreau, Lisa Hannam, Justin Dallaire and Dale Roberts, as well as 30-plus other Canadian financial experts. It’s free to view as a MoneySense.ca reader. But there are limited spaces, so don’t delay in reserving your spot. Read more about the MoneySense sessions.

Wait, what? Blackberry is still worth $4 billion!?

While the days of Crackberry and Blackberry (BB/TSX) looking like a threat to Apple are long gone, the Canadian company is still surprisingly relevant.

Enjoy this ad from Blackberry’s heyday. (Quick note for Millennial and Gen Z readers, Blackberry used to be called Research in Motion and was once Canada’s most valuable company.)

“We must not only know how to ask the right questions… but know how to answer them quickly too.”

“You not only need long-term projects, but the ability to act in a second.”

“You not only need to see the big picture, but also understand it at a glance.”

If my surgeon ever looked at my X-ray on his Blackberry as we headed into the OR—I’m out.

Ironically, Blackberry’s managed to stay somewhat relevant by going in the opposite direction of “Work Wide,” by focusing instead on cyber security and vehicle-related tech.

At its earnings call on Tuesday, Blackberry revealed that while it lost CAD$0.05 per share, this drop was better than the CAD$0.07 loss predicted by analysts. Revenue also came in higher than analysts forecasted, at CAD$168 million (versus CAD$161.45M predicted).

Executive chairman and CEO John Chen cited cybersecurity and Internet of Things (IoT) (the computing of everyday items, such as activity tracker watches and home security doorbells) as growth vectors going forward for the tech company. Blackberry shares were up 2% on Tuesday leading up to the announcement but were down slightly in after-hours trading.

Of course, share prices are still finding their equilibrium after being shot into the stratosphere by last year’s meme stock craze.

Personally, I think there is still a bit of a hangover effect going on in terms of the current share price not really being indicative of the true value of the company. Blackberry might be well on its way to long-term profitability, but I don’t need to pay that much to be along for the journey.

Nike just did it, and Bed Bath & Beyond just did not

Nike (NKE/NYSE) had news on Friday that might reveal more about the fragile psychology of the current market than it does any inherent weakness in the company. It was a tough day nonetheless.

The Swoosh started its day by announcing a strong quarter with earnings coming in at USD$0.93 (versus USD$0.92 predicted) and revenues rising 4% year-over-year to USD$12.69 billion (versus USD$12.27 billion predicted).

With results like these, one might think the market would have a pretty neutral response. Instead, citing high inventories and a crushingly-high U.S. dollar, investors sold off shares to the tune of 3.41% throughout the day, and then the share price collapsed 9.36% in after hours trading. So much for meeting anticipated sales and income targets!

On the other hand, even though Bed Bath & Beyond (BBBY/NASDAQ) substantially underperformed, relative to expectations, investors didn’t punish the retailer with their final verdict. With losses per share plunging to USD$3.22 (versus a USD$1.47 loss predicted), and revenues sinking 22% year-over-year to USD$1.44 billion (versus USD$1.47 billion expected) the market only saw fit to hand shareholders a 4.18% loss with shares down another 1.6% in after hours trading.

One thing appears to grow more certain, as these big retailers build up massive inventories, Black Friday and pre-Christmas sales should be incredible this year, as companies are looking to liquidate products from their overstuffed warehouses. Perhaps this will help households on the inflation front.

“The sky is falling!” Where can I buy a piece?

It’s no secret that 2022 has been a rough year for stock market investors, but the widespread asset class damage in the Investopedia graphic below really caught my eye.

As bad as a 21.2% drop for equities has been year to date, it’s still somewhere in the neighbourhood of expected for the stock market to throw a fit like this every once in a while.

What really hurts is the damage to fixed income, as well.

My three main takeaways in looking at this graph of asset class returns in 2022 are:

- So much for the U.S. “printing too much money” and killing their currency. The U.S. dollar has never looked like more of a safe haven asset in my investing lifetime.

- The sentiment that “Bitcoin is an inflation hedge because of scarcity, duh, fiat money is for losers” hasn’t aged well.

- Timing the market is incredibly difficult, but it’s tough not to think that, in addition to being a good time to buy equities, this may be an ideal time to look at fixed-income products. It’s very unlikely that fixed-income investments will keep realizing these types of steep losses. Interest rates would have to skyrocket 10%-plus levels for that to be the case. For folks contemplating setting up a guaranteed investment certificate (GIC) ladder, or perhaps an annuity, this might be a great entry point.

Personally, when I see asset prices plunge like this and headlines becoming more dire, that’s when I get excited about buying and adding to my portfolio. I might be wrong, but I’m much more confident now than I was in December 2021.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

The post Making sense of the markets this week: October 2 appeared first on MoneySense.

{kind=link}