The

Monetary Policy Committee of the Bank of England (hereafter ‘the

Bank’), by raising interest rates over the last six months, intends

to play its part in creating a prolonged UK recession. This is not

speculation but a statement of fact. The Bank’s latest forecast,

similar to the one in August that

I

highlighted in an earlier post, suggests negative

growth in GDP in the third quarter of this year, forecasts a further

fall in the fourth quarter, with further falls during the first half

of next year.

Why

does the Bank think it needs to help create a prolonged recession? It

is not because energy and food prices are giving us around 10%

inflation, because a UK recession will do almost nothing to bring

energy and food prices down. Instead what has worried the Bank for

some time is that the UK labour market appears pretty

tight, with low unemployment and high vacancies, and that this tight

labour market is leading to wage settlements that are inconsistent

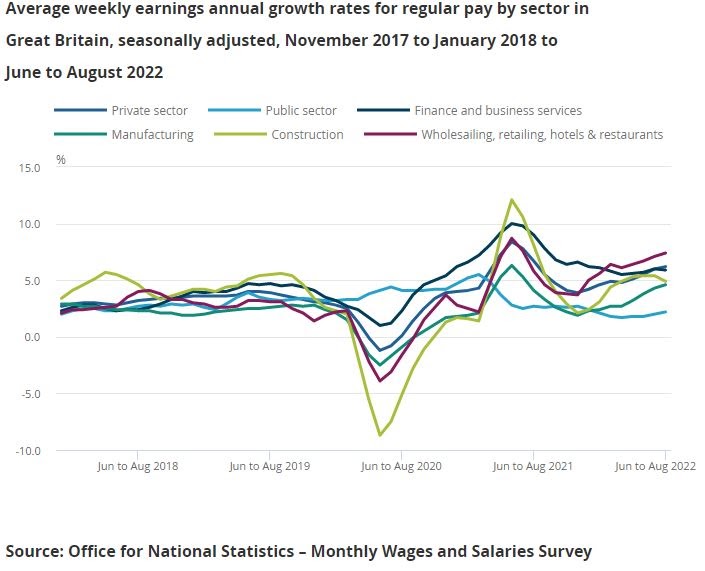

with the Bank’s inflation target. Here is the latest [1] earnings

data by sector.

Earnings

growth is around 7.5% in the wholesale, retail, hotels and

restaurants sector, about around 6% in finance and business services

and the private sector as a whole.

Of

course these numbers still imply large falls in real wages for most.

For many it seems odd to describe the UK labour market as overheated

when real wages are falling. Perhaps the easiest way of thinking

about it is to imagine what would happen if the labour market was

slack rather than tight, and as a result firms had complete

discretion over what wage increases it would pay. Domestic firms are

under no obligation to compensate their employees for high energy and

food prices, over which they have little control and which are not

raising their profits. As a result, if firms were free to choose and

there was abundant availability of labour, they would offer pay

increases no higher than the increases we saw during 2019. The fact

that in the real world firms feel they have to offer more is

consistent with a tight labour market where many firms are finding it

difficult filling vacancies.

Average

private sector earnings running at around 6% are not a problem for

the Bank because it is anti-labour, but because it believes wage

growth at that level is inconsistent with its inflation target of 2%. It’s not the kind of wage-price spiral we saw in the 1970s, but if earnings growth were to continue at 6% over the next few years then the Bank would almost certainly fail to meet its mandate. But earnings growth will slow as the UK recession

bites. The big question for the Bank is whether they are overreacting

to a tight labour market by creating a prolonged UK recession. Are

they using a sledgehammer to crack a nut?

To

try and answer this question, we can look at the Bank forecast based

on no further increases in interest rates. The reason for

looking at this forecast, rather than the ‘headline’ forecast

based on market expectations of further rate increases, is that the

Bank has been explicit in its scepticism about these market

expectations. (Why the Bank cannot tell us how they expect rates to

change in the future remains

a mystery to many of us.)

The

blue line is the Bank’s forecast for year on year consumer price

inflation. It is expected to come back down rapidly, ending up close

to target in mid 2024. The red line is GDP relative to the pre-Covid

peak quarter in 2019. [3] It shows a recession hitting its bottom in

around a year’s time, but then recovering at a snail’s pace

subsequently, so that GDP by the end of 2025 is still below the 2019

peak! This prolonged recession implies steadily rising unemployment,

increasing from current levels of about 3.5% to over 5% and rising by

the end of 2025.

If

we take this forecast seriously, and we presume the Bank does, then

there is little need for rates to increase further than 3%, and we

would expect the Bank to start cutting rates by 2024 at the latest.

The reason to expect this is that inflation is undershooting its

target by the end of 2025, suggesting unemployment of 5% is too high

to achieve stable inflation. We will have gone from an overly tight labour market to one which is overly weak. Interest rates influence inflation with

a significant lag, so to stop this undershooting and get a stronger

recovery interest rates need to start falling by 2024 if not before.

This

observation invites another. Rather than raising rates now, and

creating a significant recession, only to have to cut them again

after a year or two, wouldn’t it be more sensible to not to raise

rates by so much right now? [2] That might mean inflation takes an

additional year to go back to a target, but after a massive energy

price shock that would be more than understandable. If the Bank

thinks their remit requires them to get inflation down below 3%

within two years, that remit looks far too ambitious after double

digit inflation.

Is

the Bank’s forecast of a recession an inevitable result of having

10% inflation today? The short answer is no. To repeat the point made

at the start, the Bank cannot control energy and food prices which

are the main cause of 10% inflation. The correct question is does a

tight labour market now inevitably require a recession to correct it?

In

the 60s and 70s macroeconomists used to think that an economic boom

(in this case an over tight labour market) had to be followed by an

economic downturn (or even recession), because that was the only way

to get inflation back down. It was the logic behind the phrase ‘if

it’s not hurting it isn’t working’. But nowadays

macroeconomists believe it is possible to end a boom and bring

inflation down without creating a downturn or recession, because once

the boom is brought to an end a credible inflation target will ensure

wage inflation and profit margins adapt to be consistent with that

target.

The

Bank might argue that this will only happen if interest rates are

increased now, because otherwise the inflation target loses

credibility. But as Olivier Blanchard observes

here, the lags in the economic system mean a central

bank should stop raising rates while inflation is still

increasing. If a central bank believes it will lose credibility

by doing this, and feels it has to continue raising rates until

inflation starts falling, this will lead to substantial monetary

policy overkill and an unnecessarily recession.

If

that is why central banks in the UK and the Euro area keep raising

interest rates as the economy enters a recession, then the truth is

central banks are throwing away a key advantage of a credible

inflation target. Credibility is not something you constantly have to

affirm by being seen to do something, but something you can use to

produce better outcomes. Furthermore central banks are more likely to

lose rather than gain credibility by causing an unnecessary

recession.

Of

course raising interest rates to 3% is not enough on its own to cause

a prolonged recession. Probably more important is the cut to real

incomes generated by higher energy and food prices, which is enough

on its own to generate a recession. On top of that we have a

restrictive fiscal policy involving tax increases and

failing public services (more on that next week). Both together

should be more than enough to correct a tight labour market. To have

higher interest rates adding to these already large deflationary

pressures seems at best very risky, and at worst extremely foolish.

The question we should be asking central banks is not why they are

raising interest rates in response to higher inflation, but instead

why they are going for inflation overkill by making an expected

recession even worse.

[1]

Data up until September should become available this week.

[2]

A policy of raising rates when you can see a weak recovery and below

target inflation in three years time, because you think you can deal

with those problems later, is a good example of what macroeconomists

call ‘fine tuning’. Fine tuning makes sense in a system where you

have exact control and can forecast accurately, but makes much less

sense for a macroeconomy where neither is true. The danger of trying

to fine tune the macroeconomy is that errors in timing mean the

economic cycle gets amplified.

[3] I chose this way to show GDP because it illustrates just how poor the economy has performed in recent years, reflecting a decline relative to most other G7 countries that began over a decade ago.

{kind=link}