Executive Summary

The passage of the Affordable Care Act in 2014 introduced many changes to the healthcare landscape in the United States. One of these changes was the ability for children to remain on their parents’ health insurance plan until they reach age 26. In addition to having access to health insurance at a lower cost than they might have on their own, this measure also creates a potentially lucrative planning opportunity for young adults who can be covered by a parent’s High-Deductible Health Plan (HDHP), giving them the opportunity to contribute to their own Health Savings Account (HSA) up to the full family maximum contribution limit ($7,300 in 2022).

Health Savings Accounts (HSAs) are one of the most popular savings vehicles because of their triple-tax advantage: account owners can take an above-the-line tax deduction for eligible contributions, growth in the account is tax-deferred, and withdrawals are tax-free if they are used for qualified healthcare expenses. Notably, funds in an HSA that are withdrawn for any reason other than for qualified medical expenses before age 65 are subject to a 20% early withdrawal penalty. After age 65, though, there is no penalty, and funds can be used for any reason (but are treated as taxable ordinary income if not used for qualified medical expenses).

In return for these significant benefits, the IRS imposes certain requirements for who can contribute to an HSA: The individual must be covered by a High Deductible Health Plan (HDHP) (and have no other health coverage or be enrolled in Medicare) and they may not be claimed as a dependent on someone else’s tax return. Notably, the account owner does not have to be covered under their own healthcare plan, so a young adult who is covered under their parents’ HDHP plan (and who cannot be considered a dependent on their parents’ tax return) would potentially be eligible to contribute to their own HSA. Further, while spouses can only make combined contributions up to the family maximum contribution limit ($7,300 in 2022), non-spouses covered under the same health plan can make contributions to their own HSA up to the family limit as well!

Because HSA owners must be covered under an HDHP in order to contribute, it is important to first consider whether choosing an HDHP is the best choice given a family’s medical expenses and financial situation. This presents an opportunity for advisors to assess whether the tax benefits of HSAs outweigh the costs of opting for HDHP coverage (which typically has lower premiums but higher deductibles relative to traditional health insurance plans).

Ultimately, the key point is that because children are now allowed to remain on their parents’ health insurance plan until age 26, non-dependent children covered under a family HDHP may be eligible to contribute to their own HSAs. And as HSAs offer significant tax advantages, advisors can help clients ensure that opting for family HDHP makes sense financially for the family as a whole!

Healthcare in America saw significant changes due to the passing of the Affordable Care Act (otherwise known as “Obamacare”) in 2010. This legislation was meant to improve the affordability and availability of healthcare to Americans and, among other changes, specified that children would now qualify for coverage under their parents’ own health insurance plan until December 31st in the year when they reached age 26.

For families who contribute to Health Savings Accounts (HSAs), this change is especially notable as adult children covered by their parents’ qualified High-Deductible Healthcare Plans (HDHPs) are now eligible to contribute the full family maximum amount to their own HSAs, which offer several tax advantages (discussed later) as long as they are not able to be claimed as a tax dependent on their parent’s income tax return (even though may still ‘depend’ on their parents for some level of support).

Family Members Can Each Fund Their Own HSA, And Parents Can Still Contribute To Children’s Accounts

In Publication 969 (Health Savings Accounts and Other Tax-Favored Health Plans), the IRS outlines specific requirements that must be met for an individual to be eligible to contribute to an HSA account; these include:

- You are covered under a High-Deductible Health Plan (HDHP) on the first day of the month;

- You have no other health coverage in addition to the HDHP (with certain exceptions);

- You aren’t enrolled in Medicare; and

- You can’t be claimed on someone else’s tax return as a dependent (regardless of whether you actually are claimed or not).

Notably, one thing that is not a requirement for HSA contribution eligibility is for an individual to be on their own healthcare plan. Which means that multiple family members who are all covered by someone else’s plan (e.g., certain adult children and self-employed spouses who are covered by a family HDHP provided by the other spouse’s employer) can contribute the maximum amounts allowed by the family HDHP to their own HSA accounts ($7,300 in 2022, and $7,500 in 2023).

In other words, because the funding maximum is based on the type of plan, not individual status, single non-dependent children are able to fund their own HSAs with the full family maximum contribution limit. And notably, while the HSA funding maximum is a shared limit between married spouses covered by a family HDHP (i.e., in 2022, the total contributions made by both spouses to their respective HSAs, combined, cannot exceed $7,300), non-dependent children can each contribute up to the full maximum amount to their own HSA allowed by the family HDHP plan. (For those with individual HDHP coverage, family members cannot be covered and the HSA contribution maximum is $3,650 for 2022).

Furthermore, like a 529 or after-tax account, anyone can fund an eligible individual’s HSA. This allows parents to directly fund their child’s HSA for the year, using up to $7,300 of their annual gift exclusion for 2022 to do so.

Example 1: Steve and Susan are a married couple and have 2 adult children: Chelsea (age 22) works full-time and is not eligible to be claimed as a dependent, and Chad (age 20) is an undergrad student and is a dependent on his parents’ tax return. Steve and Susan have a family HDHP that satisfies the HSA requirements, and both children are covered by their plan.

Steve and Susan can contribute a combined total of $7,300 to their HSA accounts in 2022 (the $7,300 can be split between their 2 accounts any way they choose).

Because Chelsea is not able to be claimed as a dependent by her parents, she can contribute $7,300 (the family HDHP maximum) to her own HSA and deduct the contribution on her own tax return (regardless of whether her parents contributed to their own HSAs or not). Alternatively, Steve and Susan can contribute to Chelsea’s HSA (in addition to their own HSAs) as long as the total contributions made to Chelsea’s account (regardless of who makes them) do not exceed her own $7,300 (in 2022) family maximum limitation. And regardless of whether the contributions are funded by Chelsea or her parents, Chelsea would still be able to deduct all contributions made (by herself and her parents) to her own HSA on her own tax return.

Even though Chad is covered by his parents’ HDHP, he is also claimed as their dependent, so he is not eligible to contribute to an HSA of his own.

Individuals should fund their own accounts through payroll deductions whenever possible, as contributions set up through payroll deduction are counted as pre-tax amounts that are not only excluded from taxable income but will potentially avoid payroll taxes as well. Whereas contributions made directly to an individual’s HSA may still be income-tax deductible by the taxpayer who owns the HSA, but cannot retroactively receive a deduction for any payroll taxes that were already paid on the dollars that are contributed.

Children Cannot Open An HSA If They Can Be Claimed As A Dependent On Their Parents’ Tax Return

In order for an adult child to open an HSA, they cannot be claimed as a dependent on another’s tax return. Importantly, if the child’s parents don’t – but can – claim them as a dependent, they would still not be allowed to open an HSA. Which means that parents need to be aware of what actually makes a child a qualifying dependent (not just whether the parents are currently claiming the child as a dependent on their tax return).

There are 5 tests that must be met for a child to be considered a qualifying child for parents to claim them as a dependent. These tests, as described by the IRS and listed below, must all be met for a child to be considered a qualifying child, and are based on relationship, age, residency, support, and joint return:

- Relationship: The child must be the taxpayer’s biological or adopted son or daughter, foster child, or descendant of any of these people (they may also be a brother, sister, half-sibling, step-sibling, or a descendant of any of these people);

- Age: As of December 31, the child must be younger than age 19, or younger than age 24 if they are a full-time student. They must also be younger than the taxpayer (and the taxpayer’s spouse, if married and filing jointly) who is claiming the dependent. There is no age limit if they are permanently and totally disabled;

- Residency: Generally, the child must have lived with their parents for more than half the year (children who are away at college are considered temporarily absent and will still be considered to have lived with their parents while in school);

- Support: The child may not have provided more than half their own support for the year; and

- Filing Status: The child may not file a joint return unless the purpose is to claim a refund of withheld or estimated paid taxes.

Importantly, this means that just failing one of these tests will preclude the child from being considered a ‘qualifying child’ and therefore avoid dependent status for the purposes of HSA eligibility; this could be the age test (if they’re aged 24–26), or the residency test (if they don’t live with their parents for the requisite amount of time, not counting time away to attend school), or the Support test (at any age/time based on their own finances).

Furthermore, a taxpayer’s child who is not a qualifying child can still be considered a dependent if they can be considered a qualifying relative. The tests that must be met for parents to claim a child as a qualifying relative dependent when they cannot be considered a qualifying child include:

- Gross Income Test: The child’s gross income must be less than a certain amount ($4,400 for 2022) for the year.

- Support Test: Parents must provide more than half of the child’s total support during the year.

The determination of whether a child is a qualifying relative is primarily relevant when the child is at least 19 years old and not a full-time student (failing the age test, which means they cannot be a qualifying child) but may still be a dependent as a qualifying relative because they still depend on their parents for support (earning less than $4,400 annually).

The above discussion of Qualifying Relative tests is restricted to a taxpayer’s actual child who does not meet the requirements for being a Qualifying Child. There are actually 4 tests that must be met to be a Qualifying Relative; in addition to the Gross Income and Support tests discussed above, a person may not already be a qualifying child, and they must also either be a member of the household (who lives with the taxpayer all year) or be related to the taxpayer in one of several specific ways.

As a result of the above tests, examples of children that cannot be claimed as dependents by their parents, and thus would be eligible to open their own HSA (assuming they are covered by their parents’ HDHP), include:

- George is 18 years old and lives with his parents all year. He works full-time and pays for all of his own food and clothes, and he also pays monthly rent to his parents. [George is neither a qualifying child nor a qualifying relative because he provides more than half his own support by paying for his own rent and food.].

- Angela is 20 years old and lives with her parents all year. She works part-time and earns an annual salary of $8,500. Her parents provide most of her support. [Angela is not a qualifying child because she is not younger than age 19, and even though she is younger than age 24, she is not a full-time student. She is also not a qualifying relative because she earns more than $4,400.]

As noted above, one way that a child can be disqualified as a dependent is for them to provide more than half of their own support. For some adult children with low income levels, parents can even gift their children the annual exclusion amount, up to $16,000/year per giftee for individuals in 2022 ($32,000/year for married couples), to potentially be used by their children to pay for their own living expenses, as ‘income’ from gifts and loans are generally treated as funds that are used by the individual for their own support and not as payments from the parent-donors.

Notably, college expenses, including tuition, can count as support for children, so even if an adult child is in school and works enough to pay for their own daily living essentials, college tuition or other expenses being paid by the parent could potentially account for more than half of the child’s annual support. For example, if parents contributed $32,000 directly to a school for the tuition costs of their child whose other total living expenses were only $20,000, then the child would still be eligible to be their dependent because they would have paid $32,000 (tuition payments) ÷ $52,000 (total education and living expenses) = 61.5%, over half of the total cost of their child’s support, rendering the child ineligible to participate in an HSA.

Conversely, annual gifts made by parents taking advantage of the annual exclusion ($16k/person/year in 2022) do not count as support when given directly to independent children in cash used to pay for their own expenses, including using the gift amounts to pay their own college tuition. So, if parents contributed $32,000 in cash directly to their child in the form of a gift (that the child could then use toward tuition) and the child covered their remaining living expenses of $20,000 with their own income, then the child would be covering 100% of their own support. Which means that even though gifts from parents may be used to pay for a significant amount of a child’s tuition, if the child received no other support from their parents, they may still be able to pay for more than half of their own support’ and thus retain their HSA eligibility.

Contributions Made To A Non-Dependent Child’s HSA Is A Gift, Not a Deductible Medical Expense For Parents

While individual transfers of gifts are generally subject to a Federal gift tax, individuals can have up to $16,000 per giftee (for 2022) excluded from taxable gifts made to an unlimited number of people each year (excluding spouses, whose gifts are generally not considered a taxable transfer in the first place).

Notably, while the direct payment of an individual’s medical expenses is generally not subject to gift taxes, dollars used to fund another person’s HSA account are not exempt medical expenses; instead, HSA contributions are included as taxable gift amounts. This means that a parent’s contribution made to their child’s HSA will count as a gift and not a deductible medical expense, though no gift taxes will likely be due as the gift is still eligible to be covered under the $16,000 annual gift exclusion ($32,000 if gift-split between both parents).

The Impact Of HSA Eligibility On A Family’s Healthcare Plan Choices

Choosing the best healthcare plan can be a difficult decision for many households. Important factors like expected healthcare costs, deductibles, and premiums all weigh into the choice; however, an additional factor to consider for some individuals will be the availability of an HSA for their eligible children through their healthcare plan. And now that children can be covered by their parents’ healthcare plan until they reach age 26, this factor makes the use of HDHPs even more compelling for certain families with young adults under age 26 still in the household.

The Benefits Of HSAs For Young Adults With Long Time Horizons

The three main tax advantages of an HSA are among the most significant of any savings account: contributions are tax-deductible, growth is tax-deferred, and withdrawals used to pay for (qualified) healthcare expenses are tax-free. In contrast, most retirement accounts only offer 2 of these advantages (pre-tax contributions and tax-deferred growth for traditional accounts, and tax-deferred growth and tax-free withdrawals for Roth accounts), which make HSAs an attractive ‘triple-tax-benefit’ option to those who are eligible.

In exchange for the tax benefits offered by an HSA, there are specific rules and penalties for not adhering to them. The most important rule is that while all withdrawals used for qualified medical expenses are tax-free, regardless of age, withdrawals made for any other purpose will be taxed as ordinary income. Additionally, withdrawals made before age 65 for anything other than qualified medical expenses will incur an additional 20% penalty in addition to ordinary income taxes (whereas all withdrawals made after age 65 from an HSA are penalty-free and simply taxable as ordinary income, similar to an IRA).

As a result of the ACA changing the maximum age of independent children qualifying for coverage under their parents’ health care plans to 26, adult children who may not have had access to a High-Deductible Health Plan (HDHP) in the past – or to any healthcare plan at all – can now participate in their parents’ family HDHP, enabling them to contribute to one of the most tax-advantaged accounts available up to the full family contribution limit ($7,300 in 2022 and $7,750 in 2023) for 6+ additional years (from when they would have previously been disqualified after age 19 under prior rules, until age 26 under current rules). Which is important because not only can those adult children claim a deduction for contributions made to their own HSAs, but the tax-deferred growth throughout that individual’s lifetime can also be a key factor in the decision between different healthcare plans.

Importantly, healthcare expenses are expected to remain high in the future, meaning more dollars will need to be spent (especially in retirement) on healthcare needs. Creating and funding an HSA account early and then leaving it to grow during the child’s working years can create a ‘retirement healthcare’ spending account. In the scenario of an adult child who has the capacity to fund their HSA account every year (either by themselves or with the help of other family members), the tax-advantaged account balance that can build up while covered under a parent’s HDHP can be significant, especially given that they are allowed to stay under their parents’ coverage until age 26.

Notably, HSAs may provide the most benefit when they are invested heavily in equities and are allowed to grow over time (similar to strategies often used for Roth accounts) because the dollars will never be taxed as long as they are withdrawn to pay for medical expenses.

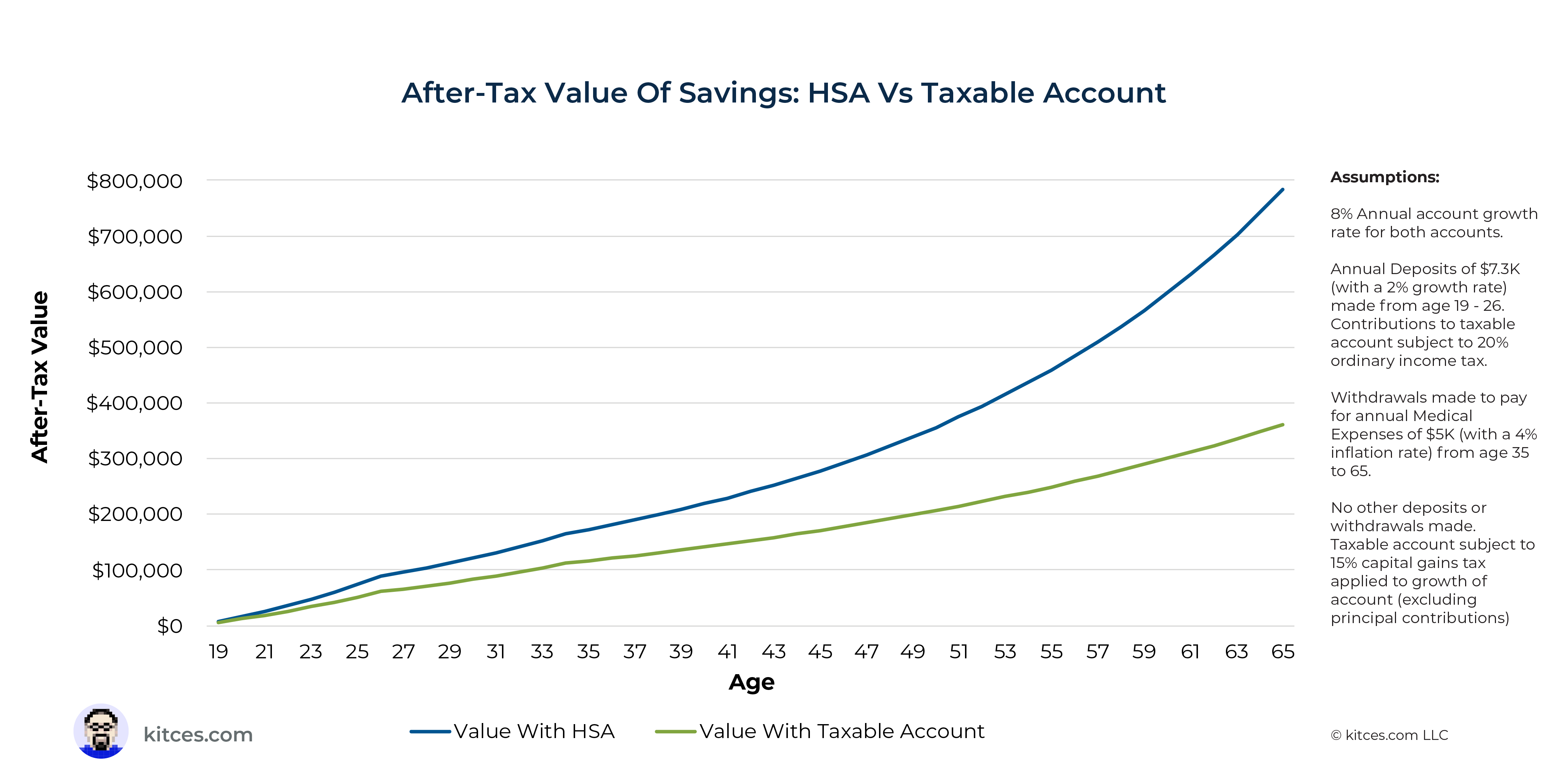

For example, the illustration below compares the after-tax value of savings in an HSA versus a taxable account for a child who saves the equivalent of maximum HSA contribution amounts from age 19 to 26 and incurs annual (medical) expenses of approximately $5,000 each year from age 35 to 65, with no other deposits or expenses made to either account.

Keeping the child’s tax rates constant over time (20% ordinary income and 15% capital gain/dividend rate), the account balance of the HSA account is more than 3 times the balance of the taxable account by age 65!

Furthermore, because adults tend to be healthier when they are younger, they can often expect to have fewer medical expenses, which means they are more likely to be able to save their HSA contributions and growth for health expenses later in life when medical expenses can be expected to rise. And if the account owner contributes the maximum amount to their HSA every year starting at an early age, they could potentially accumulate tens of thousands of dollars by age 26, continuing to compound on a tax-deferred basis for as long the individual owns the account, covering out of pocket medical expenses for decades thereafter with the growth!

Example 2: Dawn is 19 years old and is covered by her parents’ HDHP. She cannot be claimed as a dependent (because she’s over age 18 but not a full-time student, rendering her ineligible to be a qualifying child dependent) and has opened her own HSA.

With the help of her parents, Dawn is able to contribute $7,300 (the maximum amount allowed by her parents’ family HDHP in 2022) to her HSA every year for 7 years until she is no longer eligible to be covered by her parents’ plan once she’s past age 26.

Assuming a 6% return on her invested principal, Dawn can expect to have a total balance of about $61,275 by age 25.

If she stops contributing after age 25 and leaves the funds to grow with no withdrawals until she reaches age 65, her balance would reach nearly $594,600 (assuming the same 6% return). This balance would be available, penalty-free, for anything Jamie would like to spend it on, and tax-free for any of her qualified medical expenses (before or in retirement)!

When Choosing A Family HDHP For A Non-Dependent Young Adult Can Make The Most Sense

Deductible HSA contributions that come with HDHP coverage are an attractive feature given the upfront tax deduction, ongoing tax-deferred growth, tax-free withdrawals used for qualified medical expenses, and potential tax savings from payroll contributions (when permitted). The value they add can sometimes make the choice of a healthcare plan lean heavily in favor of an HDHP, especially for healthy individuals and when multiple family members can open and contribute to an HSA.

Example 3: Mary and Steve are married and have one 19-year-old daughter, Wendy. The whole family has HDHP coverage provided by Mary and Steve’s employer, Kensington Gardens Nursery.

Wendy recently got her first full-time job and is able to provide all of her own support. Because her own employer does not offer HDHP coverage, she opts to stay on her parents’ health insurance plan because she wants to open an HSA account to start saving for future medical expenses. She contributes $5,000 to her HSA, and her parents gift her an additional $2,300 to maximize her contributions for the year.

Mary and Steve also contribute the maximum amount to their own HSAs through payroll deduction, contributing a total of $3,650 each ($7,300 total) for the year.

When they file their income tax returns, Wendy can make an above-the-line deduction of $7,300 for her HSA contribution (even though some of it was funded by her parents), and Mary and Steve, who file jointly, can also deduct $7,300 for the contributions made to their HSAs.

However, the pricing and affordability of healthcare can vary dramatically for different individuals depending on their state of residence, personal health history, and employer. Two major healthcare plan options that are commonly available to employees are High-Deductible Health Plans (HDHPs) and Preferred Provider Organizations (PPOs) which typically have lower deductibles (rendering them ineligible to be HDHPs).

The most basic way to distinguish between the two plans is by comparing deductibles, premiums, and out-of-pocket expenses beyond deductibles. While HDHPs normally have higher deductibles, lower premiums, and higher out-of-pocket maximum costs, PPOs are the opposite, with lower deductibles, higher premiums, and lower out-of-pocket maximum costs.

Additionally, HDHPs tend to be less restrictive with respect to the healthcare providers they will cover, while PPO plans can sometimes have fewer ‘preferred’ providers in their service networks for individuals to choose from.

While HDHPs can be an attractive option for healthy individuals, especially when they can benefit from the tax advantages of HSA contributions, they are not always the best choice. For example, some individuals, particularly those who may not be in the best health or who expect to make frequent doctor visits, may end out benefiting more from PPOs with their lower deductibles and out-of-pocket expenses. However, those who do have ample dollars to fund HSAs can significantly reduce the net cost even with higher deductibles through the tax savings that HSAs offer, especially when the HSA can be maximally funded.

Example 4: Jack and Morgan are married with 3 dependent children. Jack is a teacher at a local high school, and Morgan is an investment analyst. They are in the 22% tax bracket, with a combined income of $250,000. Their expected annual healthcare costs are $20,000, and they want to choose the healthcare plan with the lowest net cost.

Jack is offered a family PPO through his school with no deductible and a $10,704 annual premium, while Morgan is offered a family HDHP plan with a $6,000 annual deductible and $5,000 annual premium for a maximum annual cost of $11,000.

However, since the HDHP also allows the family to make an annual deductible HSA contribution of $7,300, the Federal tax deduction will save them $7,300 (HSA contribution) × 22% (Federal tax bracket) = $1,606. Which means that the net cost of the HDHP plan is actually $11,000 (annual maximum) – $1,606 (tax deduction) = $9,394.

Thus, because of the tax savings resulting from their HSA contribution, they will come out ahead by using the HDHP even though its annual cost (of the deductible and premium) is higher than that of the PPO plan.

Naturally, most of the information needed to choose between healthcare plans is very specific to an individual’s situation. Some of the questions to ask in the decision-making process for choosing the best healthcare plan include the following:

- How much are the premiums and deductibles?

- What are the expected annual healthcare costs (and will the deductible be met?)

- What is the participant’s tax bracket and, if they can contribute to an HSA, what are the expected tax savings?

There is a significant amount of personal information to take into account when choosing a healthcare plan, so for advisors who want to help clients make the best healthcare insurance decisions, it is important to take a holistic view of all aspects of the client’s circumstances (including their current health and family history) and available options to choose the best strategy for long-term growth. Because ultimately, the same plan will not necessarily be the best strategy for everyone.

Implementing HSA Strategies For Clients With Adult Children

The logistics of opening an HSA for clients are relatively simple: the advisor can either open one on behalf of the client or provide instructions to the client that explain what they need to do to sign up on their own with any number of low-cost options available online.

Some important factors for advisors to consider when helping clients find HSA providers include annual fees (many HSAs have no annual fees), minimum opening contributions, account minimums for investment (some require a minimum amount to be left in cash), and the menu of investment options (especially for HSAs expected to remain invested for multi-decade periods of time where long-term growth rates really matter). The growth difference between a diversified investment portfolio and an account kept in cash is dramatic, so ensuring that an HSA provider allows for investing inside the plan is imperative to take advantage of the full tax benefits of an HSA.

For instance, Fidelity HSAs have no fees or minimum contributions to open the account, and options for either a self-directed brokerage account (with no monthly fees) or a Fidelity-managed account (with no monthly fees for account balances under $10,000, a $3 monthly fee for balances up to $49,999, and a 0.35% annual fee for balances over $50,000).

While there is a wide range of commission-free ETF options to choose from on the Fidelity platform, some transactions may involve trading fees. Lively HSAs are another option that require no monthly fee or cash minimum for individuals to open an account. Like Fidelity, there is an option for a self-directed HSA (through a TD Ameritrade brokerage account, with no monthly fees) or an HSA Guided Portfolio (through Devenir, for a 0.50% annual fee for invested assets).

Identifying Clients With Adult Children Who Can Use HSA Strategies

For advisors who have CRM software that allows them to identify the ages of their clients’ children, screening for clients with children between the ages of 18 and 25 can provide a list of those who can potentially benefit from establishing an HSA contribution strategy. Asking about children’s healthcare coverage for clients who are able to participate in a high-deductible health plan and are eligible to contribute to an HSA would also ensure that advisors do not skip over any clients if their CRM systems don’t include this information. These can include a number of scenarios, some of which may include the following:

- Clients who can gift funds to their adult children who have their own HDHP coverage to help them fund their HSAs;

- Clients with adult children who are not dependents and don’t have their own HDHP but could join their parents’ HDHP to get access to an HSA; or

- Clients who can gift funds to their adult children to help them support themselves in order to make them not claimable as dependents on the parents’ tax returns so that the parents can add children to their HDHP to get access to an HSA.

Next, making a note to ask about clients’ healthcare plans at the next meeting will help to filter out which clients would qualify for this strategy. Similarly, client balance sheets can also help advisors identify those with HSA accounts to ask if they claim their children as tax dependents and if their children are still on their healthcare plans (or could be added).

It is again important for clients to understand that whether or not they can still claim their children as dependents is not always easy to determine without referring to specific IRS tests (and again, the question of whether the child is eligible to open their own HSA boils down to whether the parents can claim them on their tax return, not whether or not they actually do). High-net-worth clients can often still have children older than age 19 who are dependents, as they may be either Qualifying Children (because they are full-time students if they are under age 24) or Qualifying Relatives (because of their low income and high amount of parental support the child received, regardless of age). Which is problematic as, again, if the children are dependents, they cannot participate in an HSA.

Once advisors identify the specific clients whose households include children in the targeted age range and who also qualify for an HSA plan, creating touch points with both the clients and their children can provide more value… not only by introducing a useful strategy for gifting HSA contributions but also by building stronger relationships through the involvement of family members in the financial planning process!

Determining If Clients Will Benefit From Choosing HDHPs To Implement HSA Strategies

When discussing HSA contribution strategies for clients’ children, advisors can first evaluate whether the client has access to a family HDHP in the first place (either through work or to be established by a small business owner), then determine the premiums and deductibles for the HDHP and any other healthcare insurance options available to the client, and finally discuss the family’s typical medical expenses and identify any large medical expenses anticipated in the future. This information is needed for an accurate comparison to be made.

To make the best decision for the right healthcare coverage strategy, it is important to evaluate the available plans with specific numbers. If the client is able to provide an estimated annual medical spending amount, those numbers can be useful for choosing between plans. Additionally, the client’s (and child’s) tax rates are also important to help the advisor better understand the impact of HSA savings over time.

If the client is already either saving into an after-tax account or spending more than $7,300 each year on qualified healthcare expenses, then comparing the HDHP costs (factoring in the HSA contribution deductions) against the costs of a PPO or other available healthcare plan can help to visualize the impact of the benefits of an HSA.

Example 5: David is a lawyer making $500,000 and is married to Charles, who stays at home. Their daughter, Samantha, is 21 and is eligible to be covered by her parents’ healthcare plan. She cannot be claimed by them as a dependent.

David has two plan types available, each with a spouse-only option (that would only cover David and Charles) and a family option (which would cover David, Charles, and Samantha), while Samantha also has her own health insurance PPO option offered through her own employer. The health plans available to the family are as follows:

- David’s PPO Plan – $1,000 annual deductible

- Spouse-Only Option: $300 monthly premium to cover David and Charles

- Family Option: $400 monthly premium to cover David, Charles, and Samantha

- David’s HDHP Plan – $4,000 annual deductible

- Spouse-Only Option: $150 monthly premium to cover David and Charles

- Family Option: $200 monthly premium to cover David, Charles, and Samantha

- Samantha’s PPO Plan – $2,000 annual deductible

- Individual Option: $100 monthly premium to cover Samantha only

The family’s primary goal is to choose a healthcare strategy that will protect everyone in the family at the lowest total net cost. They have access to an HSA plan that accommodates contributions through payroll deduction, which would allow contributions made by David and Charles to avoid FICA taxation.

Both parents and Samantha are all very healthy and expect low healthcare costs.

To decide which plan(s) to choose, they break down their options by plan type to assess the total cost and tax savings of each:

While David’s Family PPO option initially seemed to be the least expensive option, the family realized that if they instead chose the Family HDHP option and contributed to HSAs, they could each benefit from Federal income tax savings (and that David and Charles could take advantage of additional FICA tax savings since David would make contributions through payroll deduction).

After estimating the after-tax net cost of each strategy, they decided to go with David’s Family HDHP option as the least expensive option after factoring in tax savings from HSA contributions.

Notably, for individuals who do not take full advantage of maximizing annual HSA contributions for themselves or their children, the net value of choosing HDHP coverage can potentially be reduced. While the cost of coverage will remain the same, not fully funding the HSA can increase the after-tax net cost of an HDHP plan relative to a maximum-funded HSA (with the maximum tax deduction). Which means that it is important to assess the intended contribution levels for each HSA plan for an accurate picture of the true costs of each option.

For instance, in Example 5 above, if Samantha were not interested in contributing to an HSA, and her parents were only able to contribute $1,300 into their HSA, the estimated tax savings from the contribution would be $1,300 × (37% Federal + 7.65% FICA tax) = $580. Which means the total after-tax net cost would be approximately $6,400 (Family HDHP cost) – $580 = $5,820… more than the cost of David’s family PPO option. In this case, the family may benefit more from choosing David’s family PPO plan instead of the HDHP option.

With the Affordable Care Act’s provision allowing children to stay on their parents’ healthcare plans until age 26, parents and their non-dependent adult children who can access family HDHPs have new tax-planning opportunities involving family HDHP coverage and HSA contributions.

As while HSA accounts are very tax-advantaged, their benefits can often sway a family’s decision in favor of a family HDHP, especially when multiple family members can be covered by the HDHP and contribute to their own HSAs.

{kind=link}