Company Overview:

Inox Green Energy is a major wind power operation and maintenance (“O&M”) service provider within India. The Company is engaged in the business of providing long-term O&M services for wind farm projects, specifically the provision of O&M services for wind turbine generators (“WTGs”) and the common infrastructure facilities on the wind farm which support the evacuation of power from such WTGs. It also enjoys synergistic benefits as a subsidiary of Inox Wind Limited (IWL), which is principally engaged in the business of manufacturing WTGs and providing turnkey solutions by supplying WTGs and offering a variety of services including wind resource assessment, site acquisition, infrastructure development, etc. The company’s presence is spread across Gujarat, Rajasthan, Maharashtra, Madhya Pradesh, Karnataka, Andhra Pradesh, Kerala, and Tamil Nadu.

Objects of the Offer:

- To repay or prepay certain borrowings of the company including redemption of Secured NCDs in full

- General corporate purposes

Investment Rationale:

Strong Portfolio Base: As of June 30, 2022, the portfolio of O&M contracts (consisting of both comprehensive O&M contracts and common infrastructure O&M contracts) covered an aggregate of 2,792 MW of wind projects spread across eight wind-resource-rich states in India with an average remaining project life of more than 20 years. The counterparties to O&M contracts feature a mix of independent power producers (“IPP”) (approximately 72%), public sector undertakings (“PSU”) (approximately 14%), and corporates (approximately 14%), as on June 30, 2022. Further, certain individual wind project sites which the company has developed in collaboration with IWL have significant capacity to support the installation of additional WTGs which will further grow the portfolio base.

Financial Track Record: The company has reported revenue of Rs.165.32 crore, Rs.172.25 crore, and Rs.172.17 crore for FY20, FY21, and FY22, respectively. There has been no significant growth in revenue during this period. EBITDA for FY20, FY21, and FY22 reported by the company was Rs.95.35 crore, Rs.77.27 crore, and Rs.100.26 crore, respectively. The EBITDA margin for the same period was 55.39%, 41.48%, and 52.70%, respectively. In the last three financial years, the company has reported losses. For FY20, FY21, and FY22, IGESL reported a loss of Rs. -52.26 crore, Rs. -153.52 crore, and Rs. -93.20 crore, respectively. The performance continued to be weak in fiscal 2022 primarily owing to the continued impact of the Covid-19 pandemic.

Linkages with IWL: IGESL (Inox Green Energy Services Ltd.) is the O&M arm of IWL and undertakes O&M of projects post-commissioning. It has strong operational linkages with IWL as often, the projects have all three components: material supply, engineering, procurement and construction (EPC), and O&M. The company receives strong financial support from IWL via intercorporate deposits and optionally convertible debentures. Moreover, the entities have a common treasury. IWL is a leading wind-turbine manufacturer in India. Its revenue has grown at a compound annual rate of around 40% between fiscals 2015 to 2017, garnering a market share of 15%. Driven by the strong experience of the promoter and the healthy order book, IWL should witness a turnaround in its operations from fiscal 2023.

Key Risks:

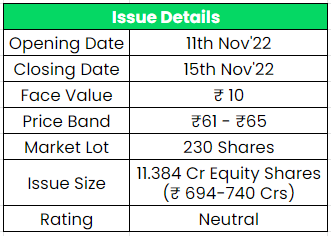

OFS – The IPO is a mix of offer for sale (OFS) and Fresh issue with OFS being 50% of the overall issue size. In the offer for sale (OFS), the promoter IWL will offload up to 5,69,23,077 equity shares. The company will not receive any proceeds from the OFS segment.

Dependency and Profitability – The company is currently entirely dependent on Inox Wind Limited (Promoter) for their business and if they were to choose another service provider for the operation and maintenance services of their wind turbine generators, IGESL’s business will be impacted. The company has reported losses for the last three financial years, and there is no surety when the company will turn profitable.

Outlook:

According to the company’s RHP (Red Herring Prospectus), There are no listed companies in India that are comparable in all aspects of business and services that the company provides. At a higher price band, the listing market cap will be around ~Rs.1900 crs. Since the company is loss-making, arriving at a P/E ratio is of no use. With the current debt levels, the Enterprise Value of the company will be around ~Rs.2690 crs (taking the listing market cap). The EV/EBITDA ratio for the company based on FY22 EBITDA will be at 27x which is high when compared with the general healthy EV/EBITDA ratio of 10-12x (Lack of Peer comparable). On the other side, the company is also planning to grow its portfolio through the entry of new long-term O&M contracts with customers who purchase IWL’s WTGs and also provide O&M services for WTGs which are not manufactured by IWL. Based on the above views, we provide a ‘Neutral‘ rating for this IPO.

If you are new to FundsIndia, open your FREE investment account with us and enjoy lifelong research-backed investment guidance.

Other articles you may like

Post Views:

69

{kind=link}