Something crazy just happened. FTX, formerly the second-largest cryptocurrency exchange, collapsed overnight. It went from a valuation of around $16 billion to a negative valuation due to a liquidity crunch and debt. How did this happen?

FTT, a crypto coin that the FTX exchange issued, plummeted in value because Binance, the largest cryptocurrency exchange, said it was liquidating FTT. FTT then proceeded to plummet in value, thereby causing a crisis of confidence in FTX as clients withdrew billions of dollars.

Binance, which caused the panic in the first place, then said it had signed a non-binding Letter of Intent to purchase FTX. But after reviewing FTX’s books, Binance backed out and has left FTX to collapse, thereby eliminating one of its largest competitors.

Given it’s an exchange, it’s difficult to understand how FTX could collapse. Apparently, FTX now owes billions to its clients and doesn’t have the money to pay up. Where the hell did its customers’ funds go?

Supposedly, FTX’s founder, Sam Bankman-Fried’s hedge fund, Alameda Research, owned a bunch of FTT, the coin FTX created. FTT was posted as collateral which enabled FTX to use its client’s funds to invest in something else. When FTT collapsed, FTX was left with a massive liability.

This is akin to Charles Schwab using your cash and investments to invest in something speculative in a Schwab family sister company. You wouldn’t allow it unless you gave permission and were paid a high-enough fee.

Shaken Investor Confidence In Crypto

I’m not sure how the cryptocurrency market comes back from the FTX and FTT meltdown. Sam Bankman-Fried was supposed to be the “savior,” according to early investor Sequoia.

Bankman-Fried is also thought to have invested $40 million in the midterm elections, which means he was supposed to have become a puppet master of politicians. Maybe a bailout is coming, but I doubt it. Bankman-Fried’s net worth is now potentially negative after being worth about $16 billion last week.

If regulators uncover fraud, then things could get even worse for Bankman-Fried. His power has faded and celebrity endorsers and politicians will now stay as far away from him as possible. Funny how people lose status very quickly once their money disappears.

Although I’ve only got one remaining crypto-related investment, HUT, in my portfolio, I no longer want to spend any time in the space. Just within the past 12 months, LUNA went to $0. 3AC went from $18 billion to $0. Celsius and Voyager went bankrupt. And now FTX and FTT have collapsed.

At this moment, cryptocurrency seems completely uninvestable. Here are SBF’s thoughts on the whole situation, which is still playing out.

Lessons Learned From The FTX Collapse

Now is as good a time as any to review some lessons learned and the lessons we should learn from this debacle.

1) Keep speculative investments to no more than 10% of your investment portfolio.

A speculative investment can range from investing in a startup to investing in a head-scratcher, such as an NFT. If you lose all your money, at least you still have around 90% of your remaining portfolio left. However, if you make it big, having up to 10% of your portfolio in such assets is enough to move the needle.

Speculative investments can also include micro-cap growth stocks, high-yield junk bonds, and of course, crypto. But sometimes, investments you think aren’t speculative will also collapse like some of the most speculative investments. Examples include Facebook, Redfin, Affirm, and Upstart.

Due to investing FOMO, chasing the next hot investment is inherent. But we must maintain control of our risk exposure and our emotions.

As such, diversification is important for capital preservation. You want to diversify your net worth so that when one asset class declines, another asset class increases or at least significantly outperforms. I wouldn’t allocate more than 50% of your net worth to one asset class.

2) Turn funny money into real assets.

One of my classic posts is called, How To Get Rich: Turn Funny Money Into Real Assets. I originally wrote the post in 2014 to remind readers and myself to occasionally spend our investment gains on real assets and experiences. It was five years after the global financial crisis and the good times had returned.

Funny money is any investment that has no utility. Funny money is essentially anything you can’t touch that also doesn’t generate income or provide utility. Stocks, cryptocurrencies, and even bonds are considered funny money. Although stocks and bonds that generate income are less so.

Real assets, on the other hand, are any asset that you can touch that also provides utility and potential income. The most common real asset is real estate. If you’ve ever wondered why some really rich people buy $100 million mansions with 18 bathrooms, it’s because they are trying to enjoy and protect their wealth.

Given much of their net worth was built upon funny money, they also know their wealth can easily evaporate overnight like Bankman-Fried’s did. Hence, rich people end up buying lots of real estate, fine art, expensive wine, yachts, rare books and other collectibles to protect and enjoy their wealth.

Remember, money is meant to be spent so you can increase your lifestyle. Hence, if you can spend your money on something you can enjoy that also has the potential to increase in value, you’ve got yourself a winner.

The money I invested in 2020 to buy our existing home is much more rewarding than every other intangible investment I’ve made since. As a father, it makes me proud to be able to shelter and provide for my family. The potential price appreciation of the house is secondary.

3) Debt can be a killer

With manageable debt or no debt, you will most likely always be fine in a recession. It’s the people who violate my 30/30/3 home buying rule, go on excess stock margin, and have a lot of revolving credit card debt that tend to get crushed.

Even if your stock goes down 50%, you’re fine if you’re not on margin. But if you’re on 50% margin and your stock goes down 70%, you lose everything and now owe the brokerage.

One guy I played softball with in 2021 bought at least $250,000 worth of Tesla stock on margin when the stock was much higher. The thing is, he already had $700,000 worth of Tesla stock. As a result, his $700,000 is now worth closer to $250,000.

But what’s worse, he didn’t properly quantify his risk tolerance. He makes about $100,000 a year, which means he has to work about 55 months to make up for his Tesla losses. As someone who just had his first kid, taking this type of risk was excessive.

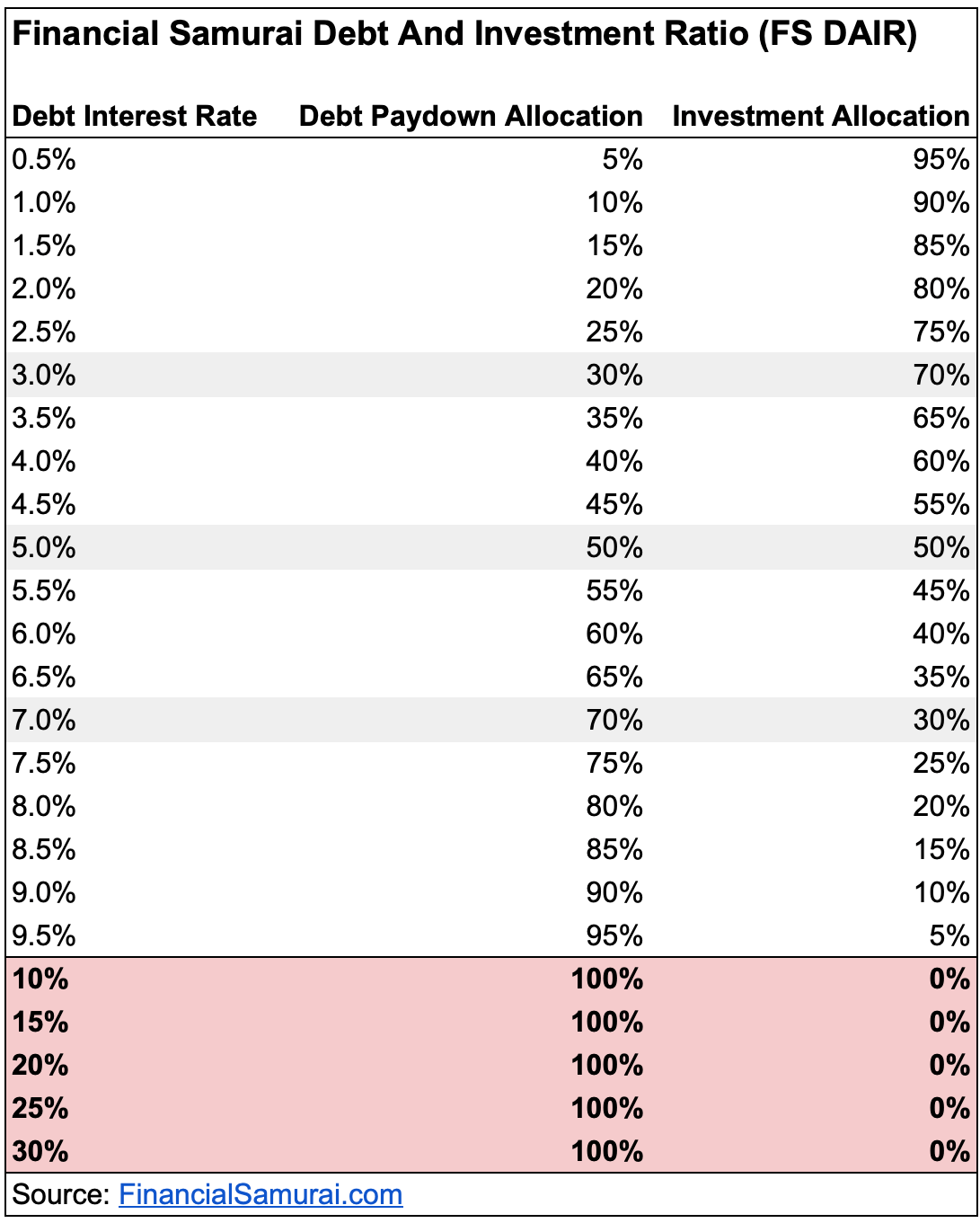

On your financial independence journey, please continuously work on paying down debt and investing using my FS-DAIR formula. If you’re always paying down debt and investing, you’re always winning no matter the economic situation. For folks who paid down debt instead of investing in the stock market at the beginning of 2022, they are winning by at least 25%.

4) Lots of cash creates lots of temptation to do stupid things

The more cash you have, the more temptation you might have to spend it on unwise things. This temptation is why you should always pay yourself first by investing as much as possible before spending.

Paying yourself first is one of the main reasons why buying a house with a mortgage tends to build more wealth than the average renter who is supposed to save and invest the difference. Automatic mortgage payments build equity as home prices generally rise over time.

One of the reasons why I’ve been aggressively buying Treasury bonds is because I’m forced to transfer the funds to my brokerage account. Once the funds are in the brokerage account, I can’t use the money to buy anything wasteful. Instead, I buy various Treasury bonds which get locked up between three months and three years.

If you own a business and have a lot of cash on the company balance sheet, you may also be tempted to misappropriate funds. It’s best to reinvest the money in your business or pay the money out to employees and shareholders as distributions.

Example Of An Almost Terrible Investment Due To Having Some Cash

In mid-2022, I stumbled across my dream home. It had a gated front yard for my kids to play in. The lot was over 9,000 square feet, which is 3.5X larger than the average lot size in San Francisco. The home was recently remodeled and spanned about 4,300 square feet.

I was feeling some intense real estate FOMO because a buddy of mine was looking at even nicer homes. I figured, if he was looking for nicer homes, so should I!

Buying this home would have been incredibly stressful because I would have had to take out a huge loan. Further, I would have had to convince my family to move after just two years of living in our current home. I didn’t even have the full 20 percent down payment. I would have had to borrow money from a friend, which is always dicey.

If I had bought the home for asking, I would be down about 5% just five months later. The house was overpriced to begin with, but I really wanted it. Being down plus having all the extra debt would sour my daily mood. Finally, due to the house’s floorplan, it might have been too noisy for me to peacefully write.

Thus, to eliminate my constant addiction to buying single-family homes, I only keep six months’ worth of expenses in cash. Only when I envision our family seriously needing a new home within two years will I start raising more cash.

5) Trust is everything in investing, and FTX lost everybody’s trust

One could argue that FTT and all other cryptocurrencies are Ponzi schemes. Even Sam Bankman-Fried inferred his yield farming business was a Ponzi scheme on the Odd Lots podcast earlier this year.

Once trust is lost, businesses tend to unravel. Nobody dares to deposit any funds with FTX due to what has transpired. Clients thought their assets were safe, but apparently they were not. It’s kind of like Bernie Madoff all over again.

If you stomp on a business’s demise and then share internal e-mails publicly with an “I told you so” attitude, like the CEO of Jefferies did on Twitter, you also likely won’t garner the trust of prospective clients. Keep private communication private.

With Financial Samurai, if I don’t write from firsthand experience, it’s harder to believe what I say. If I just write about how everything is hunky dory on my financial independence journey, would you really believe me? Probably not because life is full of ups and downs.

Related posts:

Perpetual Failure: The Reason Why I Continue To Save So Much

The Negatives Of Early Retirement Nobody Likes Talking About

6) Invest in only what you understand

If you don’t know what a company or product does and can’t easily explain your investment thesis to a friend, then you probably should not invest in it.

It is very hard to wrap my head around how FTX could be worth so much one day and then implode overnight. From the creation of crap coins to the process of yield farming, it’s hard to explain what exactly is going on.

You can certainly take a punt on a speculative investment with a small portion of your portfolio (lesson one). But having a core position in something you don’t fully understand is unwise. If you do such a thing, you are leaving your investment returns entirely up to luck.

Either thoroughly understand the investment or invest with someone you trust who thoroughly understands the investment. We’ll still get some of our investments wrong. But that’s the price we pay to earn returns.

Related post: The Recommended Split Between Active And Passive Investing

FTX’s Collapse Is Scary Stuff

I haven’t been this shaken by what seems like financial fraud since Bernie Madoff’s $50 billion Ponzi scheme was exposed in December 2008.

I’m pretty sure we’re going to look back on 2021 as the most bubbliscious time in recent history. 2021 was crazier than 1999, 2000, or 2007. Now the hope is the overall downturn won’t be as deep or as long.

But based on the declines in stock prices like Facebook and other tech companies, and the collapse in FTX and other crypto-related assets, the downturn has already been just as bad for many.

Let’s just hope investors aren’t so rattled by FTX’s collapse that they drag the stock market don’t further. The silver lining of this bear market, besides an easier time to generate more passive income, is more investors embracing the concept of turning funny money into real assets.

As a result, I continue to prefer real estate as my favorite asset class to build long-term wealth. Sure, real estate prices can and will decline as the economy slows down. But I’ll be looking to buy more real estate at more attractive prices in the future.

Finally, as I wrote in my most bullish indicator article, I think the worst of this bear market is over. Time will tell if I’m right or not.

Readers, what are your thoughts about FTX’s sudden collapse? How could something like this happen so quickly? What are some other lessons we should learn from the FTX debacle? What are your thoughts on the future of cryptocurrency now?

For more nuanced personal finance content, join 50,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

{kind=link}