And on we go relentlessly. Another 10 randomly selected Danish stocks, with only 16 more to go. This time, 3 of them made it onto the preliminary watch list. Enjoy !!

151. Nordea

Nordea is a 36 bn EUR market cap “full service” bank and asset manager active in the Nordics. As many other Scandinavian financial institutions, Nordea is doing quite well compared to its European peers, managing ROEs of around 7-11% over the past 10 years.

The longer term share price development is nevertheless quite disappointing, showing little to no value creation:

The biggest attraction is clearly the dividend yield which stands at currently 7% or so. Valuation wise, Nordea trades at 11,5 x P/E and ~1,2x P/B, reflecting its stable earnings. Among the sharholders, the most interesting is Nordic Activist investor Cevian who is on board since 2018.

However not much seems to have changed. I am not yet convinced that investing into banks is the best opportunity right now, therefore I’ll “pass”.

152. Djursland Bank

Djursland Bank is a 110 mn EUR market cap regional bank. With a P/E of 7,4x and P/B of 0,6x, the stock looks cheap, but the dividend yield is only around 2%. Djursland actually managed to increase earnings over the past few years, but still I am not that much interested in regional Danish banks. “Pass”.

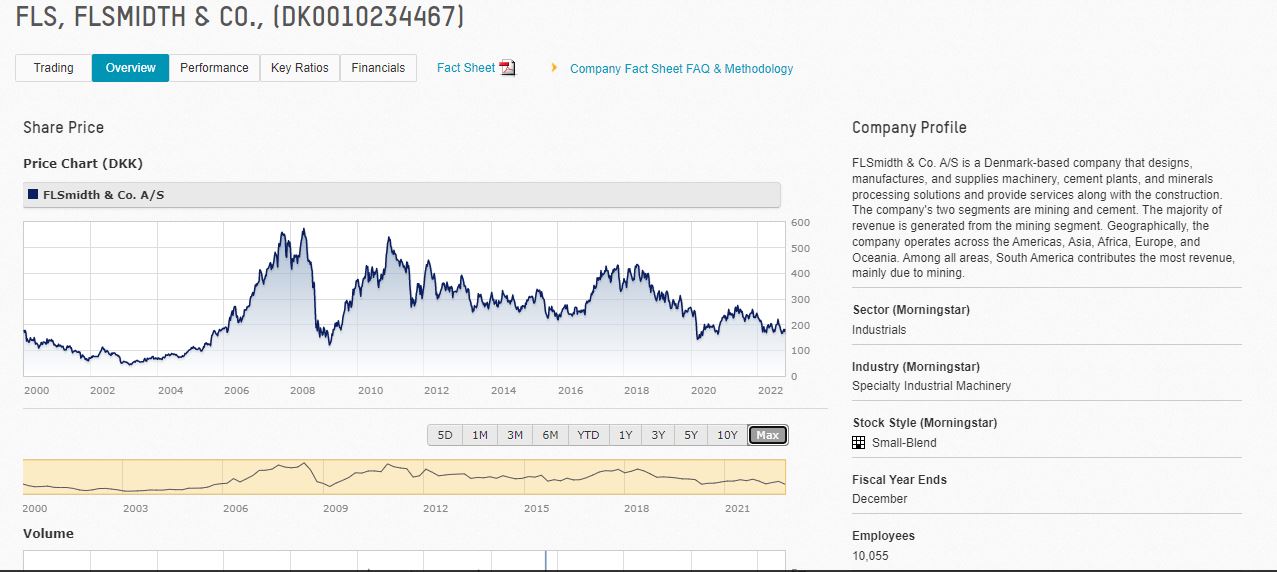

153. FLSmith & Co

FLSmith is a 1,4 bn EUR market cap company that specializes in equipment for the Cement and Mining industry. The long term stock chart looks rather depressing:

The stock currently looks quite cheap at ~10x 2022 earnings. margins in this business are quite low (EBIt margin ~5%) as well as return on capital. Mining is around 75% of the business.

This could actually become interesting again, considering the required mining for the Energy transition/electrification. Another interesting aspect is that FLSmith took over the (loss making) Mining activities from Thyssen Krupp recently.

Overall, despite the relatively mediocre profitability, I think this could be interesting. “Watch”.

154. Hove

Hove is a 10 mn EUR market cap company that develops “advanced lubrication solutions” which sounds like a high tech version of Fuchs Petrolub.

In contrast to other 2021 IPOs, Hove actually has sales and makes a small profit. Their financial reports sow a lot of offshore wind mills and they seem to offer solution for wind.

However, 6M 2022 didn’t look so good and the stock is too small to bother. “Pass”.

155. Nordic Shipholding

Nordic Shipholding is a tiny, 5 mn EUR company somehow active in shipping. Over the last 5 years they only have shown losses. “Pass”.

156. Matas

Matas is a 380 mn EUR market cap retail chain that i”engaged in a retail chain selling beauty, personal care, and health products”. It seems to be active only in Denmark. At a first glance, it looks interesting. Business seems to be quite stable (so far) and the stock looks cheap at 10x P/E.

However, the long term chart doesn’t look very constructive:

As retail is not one of my strong areas, I’ll “pass”.

157. Wirtek

Wirtek is a 15 mn EUR “software outsourcing” company that looked pretty bad for 10 years before it got a second life during Covid:

The company has grown for the last couple of years and is now profitable. As far as I understand it, they are more an outsourcing service provider than a software company that writes its own code. The majority of Employees seems to be employed in Romania. They guide towards 9 mn EBITDA (mid point) which would be ~12x EV/EBITDA, but at a growth rate of 40%. This looks interesting. I’ll put them on “watch”.

158. Intermail

Intermail is an 8 mn EUR market cap company that “that helps its customers create more leads, more sales and make customers loyal, so that customers’ lifetime value increases. The company works with communication on all modern platforms such as Google, Facebook, LinkedIn, Instagram and ensures that market communication across various digital and analog distribution channels creates the greatest possible effect”.

The company actually has some sales and has become profitable, however current revenues are only 1/5 of the level 10 years ago. Doesn’t look very interesting, “pass” for the time being.

159. Københavns Lufthavne

The translation of this company means “Copenhagen Airports” and this is what this 6,6 bn EUR market cap company does. As far as I understand, ~98% are owned by the Government and free float is tiny. Valuation does not make sense at first sight (50x EV/EBITDA). “Pass”.

160. Danke Bank

With a market cap of 14 bn EUR market cap, Dankse Bank is clearly one of the larger Nordic Banks. A quick look at the chart shows, that similar to many other banks there was little value creation over the past 22 years:

At 6,7 xP/E and 0,7x P/B (Trailing), Danske looks cheap, however for 2022, Danske will most likely book a significant loss. This has to do with a scandal from the past: Danske was found guilty to facilitate money laundering mainly via its Baltic subsidiaries in 2017/2018. In 2022 they finally booked a 14 bn DKK reserve to settle the issues. On top, they also wrote down the Goodwill of an acquired Pension business.

On the plus side, the core banking business seems to recover. The biggest shareholder is MP Moeller, the parent company of Maersk with a stake of 21%. Personally, I find this a potentially more interesting case as it could be some kind of “special situation recovery” play, therefore Danske goes on “watch”.

{kind=link}