In the IMRA post comments, I mentioned that Sio Gene Therapies (SIOX) (~$30MM market cap) was a likely liquidation candidate. Sio Gene Therapies is one of the many pre-revenue biotechnology companies — this one was originally focused on gene therapy for Parkinson’s disease — that has given up development and was pursuing strategic alternatives due to poor clinical results and/or tough capital raising conditions. Often these broken biotechnology companies end up doing a reverse merger, but here the company never really had its own IP, they had licensed the IP from third parties and their NOLs are primarily domiciled in Switzerland where corporate taxes are low, thus limiting their value. Other than a public shell, which isn’t in much demand these days when SPACs are all liquidating and the IPO market is fairly quiet, SIOX has little value remaining outside of its cash. This week, SIOX announced the board approved a plan of liquidation (requires shareholder approval).

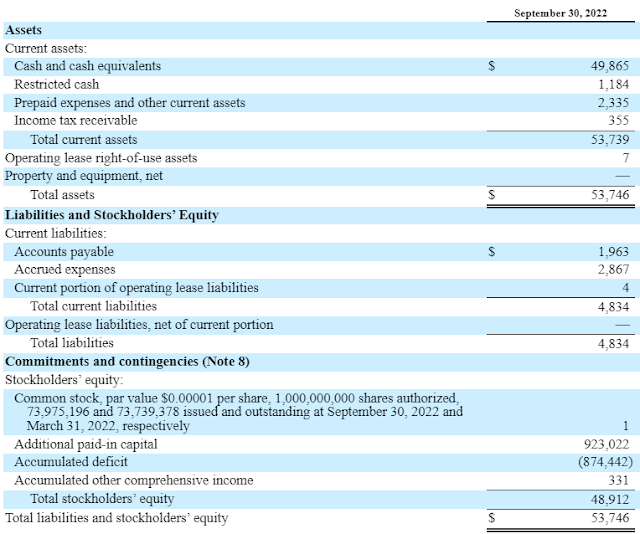

The balance sheet is fairly simple at this point (9/30 10-Q):

They’ve already laid off most of their staff and gotten out of their office leases (no non-current liabilities are remaining), this should be a fairly straight forward liquidation. The remaining cash burn should be limited to some remaining G&A and liquidation costs. They do mention in the same 10-Q that “we continue to conduct one pre-clinical research and development program” but it must be small and likely easy to pause. In addition to the above balance sheet, they do have a CVR-like payment of up to $7MM after their sale of Arvelle Therapeutics, while that’s a nice lotto ticket, it also means the future liquidating trust might be around a while (unclear to me how long these milestone payments extend) which would lower the potential IRR.

Disclosure: I own shares of SIOX