What is Effective Tax Administration?

Effective tax administration (ETA) cases are one area where tax professionals really get to put their negotiation skills to work. This type of Offer in Compromise comes into play when a client doesn’t dispute the amount of tax owed, and even has the money to pay, but has an extraordinary reason for not paying.

In order to get your effective tax administration case accepted, you’ll have to convince the IRS that accepting the offer will ultimately be more beneficial than collecting the tax.

The IRS splits potential ETA offers into two different situational categories—economic hardship, and public policy or equity grounds. To help you understand acceptable ETA offers that would fit into each of these categories, we’re going to look at potential scenarios provided directly by the IRS.

Economic Hardship

Economic hardship is a consideration for clients who have the ability to pay their tax debt in full, but doing so would place them in severe economic hardship.

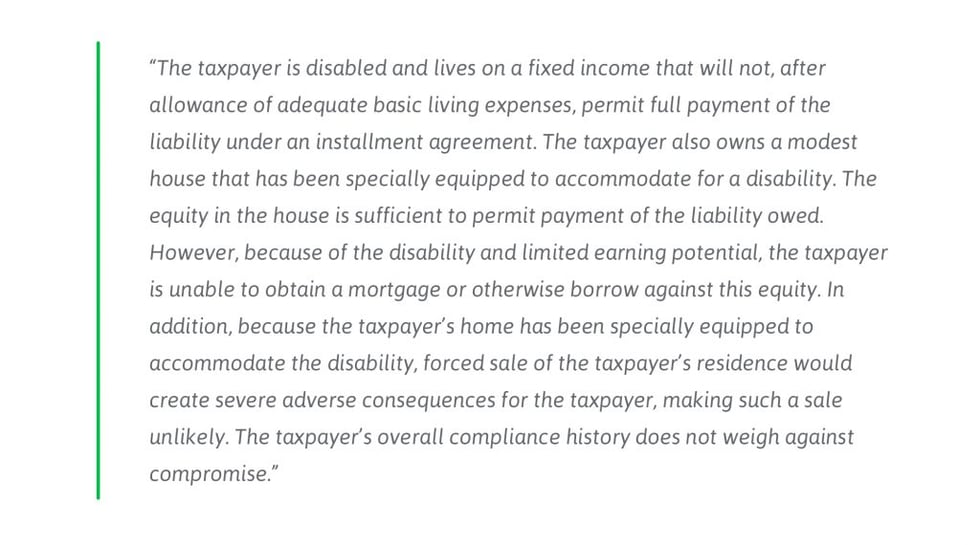

Example:

—IRM 5.8.11.2.1

Public Policy or Equity Grounds

Public policy and equity offers are for situations when “collection in full would undermine public confidence that the tax laws are being administered in a fair and equitable manner.” Effective tax administration offers should reflect the situation laid out in the offer and cannot be $0.

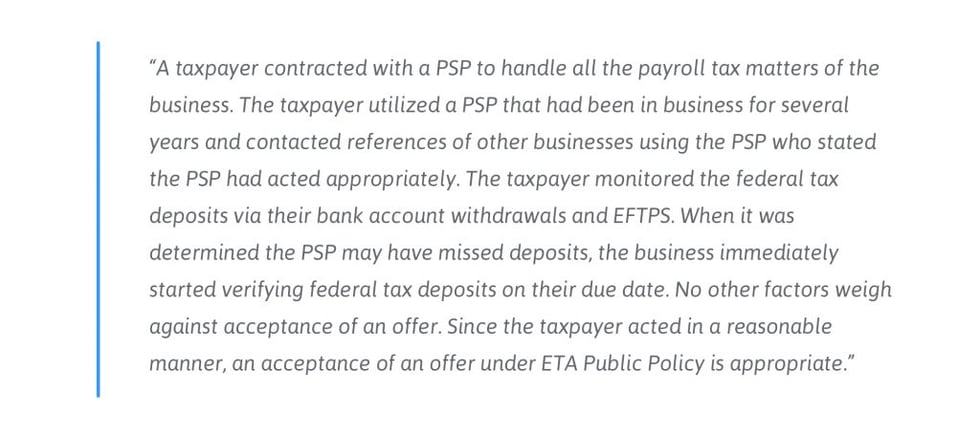

Example:

—IRM 5.8.11.2.2

Now that you understand ETA, you’re well on your way to being an Offer in Compromise expert.

{kind=link}