Private residential construction spending declined 0.5% in November, as spending on single-family construction plunged 2.9%. Private residential construction spending fell for the six consecutive month, standing at an annual pace of $868 billion. However, this total remains 5.3% higher compared to a year ago.

The monthly decline is largely attributed to lower spending on single-family construction, which has also declined for six straight months. Compared to a year ago, it is 10.2% lower. A surge for interest rates cooled the housing market in 2022. The average 30-year Freddie Mac fixed mortgage rate reached 7% in October for the first time in 20 years.

Multifamily construction spending increased by 2.4% in November, after an increase of 2.4% in October. This was 10.7% over the November 2021 estimates, largely due to the strong demand for rental apartments. Private residential improvements rose by 1.3% in November and was 27.6% higher over a year ago. The remodeling market continues to overperform the rest of the residential construction sector.

Keep in mind that construction spending reports the value of property put-in-place, so it is a measure of property value placed in service at the end of the construction pipeline.

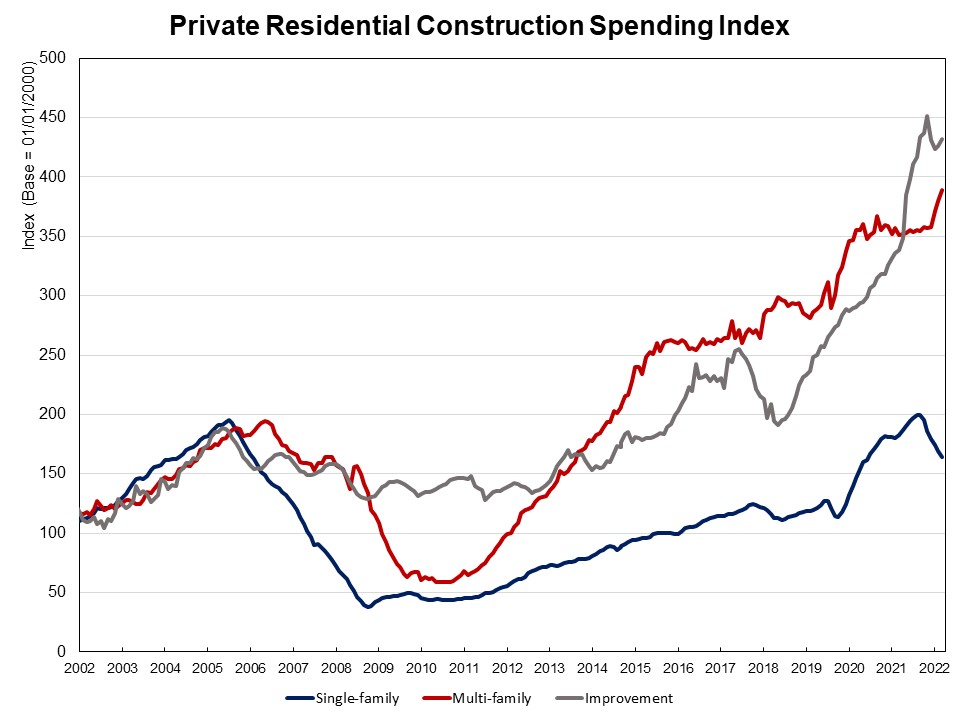

The NAHB construction spending index, which is shown in the graph below (the base is January 2000), illustrates how construction spending on single-family has slowed since early 2022 under the pressure of supply-chain issues and elevated interest rates. Multifamily construction spending has had a solid growth in recent months, while improvement spending has increased its pace since early 2019. Before the COVID-19 crisis hit the U.S. economy, single-family and multifamily construction spending experienced solid growth from the second half of 2019 to February 2020, followed by a quick post-covid rebound since July 2020.

Spending on private nonresidential construction increased by 1.7% in November to a seasonally adjusted annual rate of $558.3 billion. The monthly private nonresidential spending increase was mainly due to more spending on the class of manufacturing category ($7.6 billion), followed by the power category ($1.2 billion), and the transportation category ($0.5 billion).

Related

{kind=link}