You work hard to ensure your client’s businesses do well. But, many accounting professionals struggle with an unreliable cash flow when clients pay late or forget to pay. The good news is your firm doesn’t have to suffer. Want to make sure your firm gets paid? Read on to learn how to get clients to pay on time.

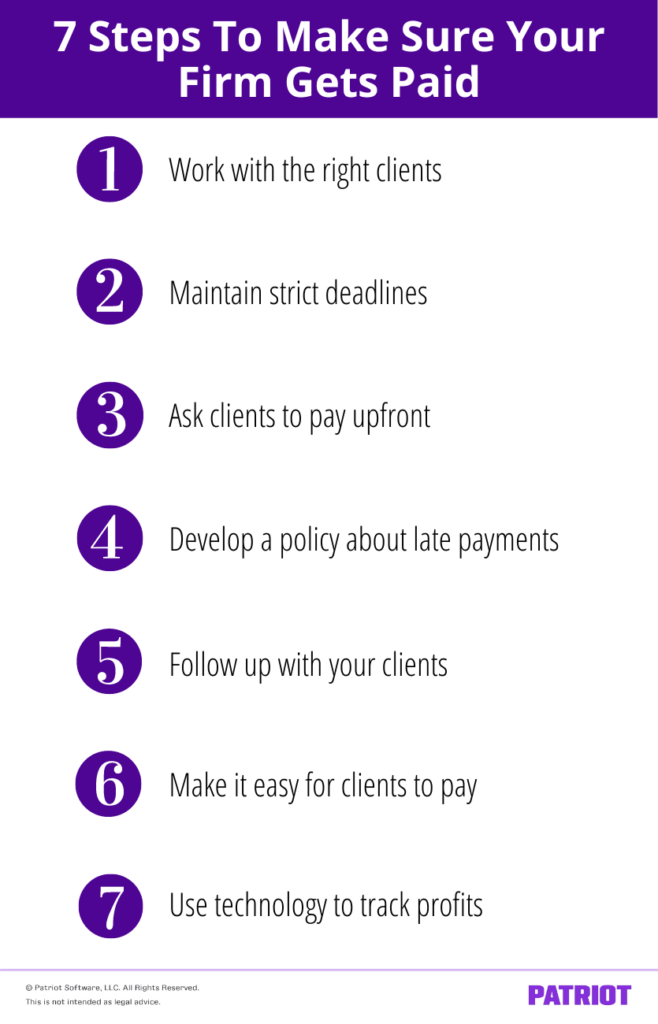

How to get clients to pay on time in seven steps

There’s no single solution to stop late payments from happening. But you aren’t helpless. Read on to learn how to get clients to pay on time.

1. Work with the right clients

Not all clients are the same, especially when it comes to getting paid on time. Some clients will surprise you with late payments or a disappearing act when you least expect it. Before you start researching how to get more clients, create a client acceptance criteria and evaluation process to make sure you know exactly who your client is before doing business with them.

Here are some steps you can include in your client acceptance and evaluation process:

- Interview prospective clients. Whether you are meeting in person or online, getting to know your client can help you make the best decision.

- If the client is switching CPAs, find out why. Ask them if this happens often or is just a one-time occurrence. A prospective client refusing to answer may be a red flag.

- Perform a credit check to learn the client’s ability to pay on time.

- Research to find any pending or past lawsuits with previous professional advisors.

2. Maintain strict deadlines

If you want your clients to pay on time, make sure that you meet your deadlines. If you can’t deliver by the deadline you set, your client could easily take it personally. Clients could think that their business isn’t important to you or that you aren’t as professional as they thought. Whatever they think about your firm, it won’t be good. And, you should expect some late payments to quickly follow.

Bill clients as soon as you finish. The longer you wait to send a bill, the greater the chance they’ll wait to pay.

3. Ask clients to pay partially or fully upfront

You may find that no matter what, invoicing your clients still leads to some late payments. Think about asking for upfront payments.

An upfront payment asks clients to pay part or all of your fees before you do the work. This can reduce the risk of clients not paying you and increase your cash flow.

4. Develop a clearly stated policy about late payments

Despite your best efforts to stop late payments, they may still happen. Plan accordingly. Develop a clear policy about late payments so that clients know exactly what to expect.

Your policy could include:

A timeline for late payments

How late is too late? Define late payments on your terms. For instance, Net 30 is an invoicing term referring to the number of days (30) the client has to pay the outstanding balance of a bill. Net 30 gives the client a specific amount of time to make their payment. Depending on your needs, you can use different timelines, such as Net 10, 20, or 60.

An early payment discount

Early payment discounts can encourage clients to pay early. For example, you could offer a 5% discount for early payment or use a sliding scale depending on how early clients pay their bill. With a sliding scale, the discount is higher the earlier clients pay. So if clients pay immediately, they could receive a 10% discount. And, they could receive an 8% discount if they pay within five days.

A recurring payment option

If you’re planning on working with your client long-term, a recurring payment option can keep bills paid on time and let you both focus on work. You can even automate this process by using accounting software with a recurring invoice feature.

A late payment fee

Late payment fees shouldn’t come as a surprise to clients. Make sure to put the late payment fee start date at the top of the invoice so clients know what to expect. Your late payment fee should be simple to understand. You can charge a flat rate or a percentage of the bill’s total.

5. Follow up with your clients

If you consistently struggle with how to get a client to pay an invoice on time, remember that your clients are regular people, just like you. And sometimes, it’s easy to overlook payment deadlines.

As soon as you notice an overdue payment, send a friendly reminder. Chances are, it just slipped your client’s mind, and they’ll be happy to pay.

6. Make it easy for clients to pay

Is your payment process as easy as it could be? Checks work great, but they can take a long time to make it to your bank account. Accepting credit cards or online payments are great ways to meet customers where they are and receive payments as soon as possible.

If you send your clients an electronic invoice, add payment links to make things as easy as possible. As soon as clients see their invoice, they’ll immediately know how to make a payment.

7. Use technology to help boost productivity and track profits

Don’t spend all your time looking for data or stubbornly crunching numbers by hand. Fifty-six percent of accountants report that technology increases their productivity.

With the right technology, you can:

- Store needed documents online so all parties can access them whenever needed

- Spot patterns and predict trends

- Provide insight into future opportunities for growth

Artificial intelligence (AI) is already changing what’s possible. For example, AI can boost the quality of an audit by deepening an auditor’s understanding of a client’s financial statements. Auditors can use AI to analyze complete transaction data (rather than just sampling data) and automate manual tasks.

Believe it or not, boosting your productivity and making your firm integral to the life of your client’s business is a great way to promote on-time payments.

Time means money. Don’t waste your time with outdated accounting and payroll software. Patriot Software’s Partner Program offers award-winning accounting and payroll software at discounted pricing. Schedule a call and get started today!

{kind=link}