Running a business also means paying business taxes. Regardless of what you’ve heard, business taxes don’t have to be stressful. In fact, you can actually reduce your tax bill. Read on to learn about business taxes and how to reduce your tax bill as a small business owner. Plus, get five tips for reducing your tax bill.

Your business entity and tax liabilities

There are several ways to reduce your tax bill. Before we dive in, let’s take a brief refresher on business taxes, including business tax entities and tax liabilities.

Generally, as a for-profit business owner, you must pay business taxes on your profits and your individual income. Depending on your business structure, you may have pass-through taxation, which lets your tax liability pass from your business to you instead of paying them at the business entity level. With pass-through taxation, you file a personal tax return for business and personal income.

Tax liabilities

Tax liability is the amount of money a business or individual owes to tax authorities. The tax liability of your business depends on your business structure. For instance, you have pass-through taxation if your business is a sole proprietorship. Here’s a quick look at the tax liability of specific business structures:

*Unless your business elects to be taxed as a corporation.

Your business tax liability isn’t the only type of tax liability you might have.

Here are some other types of tax liability you should know:

- Earned income tax

- Self-employment tax

- Payroll tax

- Sales tax

- Capital gains tax

- Property tax

If the amount of possible tax liabilities has you worried, there’s good news. The more tax liabilities you have, the better the chances are that you can reduce your taxes through credits and deductions.

How to reduce your tax bill

Have you ever wondered, How can I reduce my tax bill? Of course you have! Tax credits and deductions are a great way to reduce your tax bill. You may even qualify for a refund, depending on your credits and deductions. How great is that?

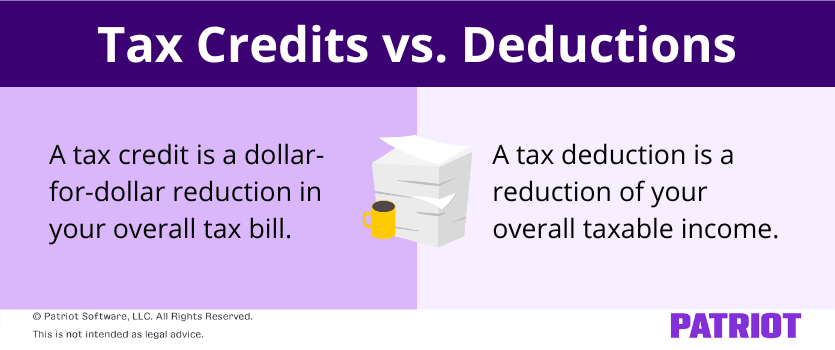

What is a tax credit?

A business tax credit is a dollar-for-dollar reduction of the taxes you owe. Businesses and individuals can claim tax credits. Tax credits are either refundable or nonrefundable.

A refundable tax credit is paid out in full. In other words, if your refundable tax credit exceeds your tax amount, you’re entitled to the remaining credit.

Let’s look at an example of this in action. If you owe $20,000 in taxes and have refundable tax credits that total $20,150, you’d have $150 left over once your tax bill was paid in full. And you’d receive that $150 as a refund.

On the other hand, nonrefundable tax credits don’t offer a refund. Instead, the tax credit covers your tax bill and any remaining credit essentially disappears.

Going back to our previous example, if you owe $20,000 in taxes and have nonrefundable tax credits that total $20,150, once your balance is $0, the remainder of the credit disappears. You can’t use the remaining $150 because it no longer exists once your tax bill is paid in full.

If you claim both refundable and nonrefundable credits, make sure to claim the nonrefundable credits first. That way, you have a better chance of getting a refund.

Here are just a few of the tax credits you may qualify for:

What is a tax deduction?

Business tax deductions lower the total taxable income of your business, which means you get to keep more of your money. Both businesses and individuals can claim tax deductions.

Here’s an example of how a tax deduction works. A tax deduction of $3,000 would decrease your $90,000 taxable income to $87,000.

Here are just a few of the deductions you might be able to claim:

Tips for reducing your tax bill

Reducing your tax bill can be exactly what your company needs, especially when you’re faced with a heavy tax bill. But if you do things incorrectly, you may have to worry about an IRS audit.

Before you start the mad dash to claim tax credits and deductions, make sure you do things right. Follow these five tips to keep things legal.

1. Don’t claim too much

In a perfect world, you’d like to get your tax bill as close to $0 as possible. But claiming too many credits or deductions can alert the IRS that something’s afoot. Remember that no matter what you claim, you must be able to prove the action was for business purposes.

The business mileage tax deduction is a good example. With the business mileage tax deduction, you can only deduct the miles you drove for business purposes. The IRS will probably have a few questions if you claimed 100% of your miles for business purposes.

If you work remotely, it can be hard to separate your business life and home life. This is a must when it comes to claiming business tax credits or deductions. For instance, renovating your kitchen doesn’t qualify for the home office tax deduction. But you can claim the office furniture you purchased for your home office.

2. Claim the right credits and deductions

When it comes to deductions, here are some common deductions small business owners can take:

- The cost of advertising and promotion of your business

- Bank fees (e.g., transfer and overdraft fees)

- Premiums for business insurance (e.g., property coverage, professional liability, workers’ compensation, etc.)

- Depreciation of business assets

- The interest paid on a loan or credit card used to cover business expenses

- Rent paid for your business location (as long as it isn’t your home) and for business equipment

There are so many different credits and deductions to choose from that it can be hard to make the right choice. Take a look at Form 3800, General Business Credit—specifically Part III. Part III lists the possible credits you can claim and the forms needed to make the claim.

If you see a claim on Form 3800 you think applies to your business, see the associated form to make sure.

3. File on time

Deadlines are important, especially when it comes to claiming credits and deductions for your business. If you miss certain deadlines, you’ll miss the chance to claim certain credits and deductions.

Here are some deadlines you’ll want to put in your calendar:

| Tax Structure | Tax Return | Tax Deadline |

|---|---|---|

| Multi-member LLC | Schedule K-1, Form 1065 | March 15 |

| Partnership | Schedule K-1, Form 1065 | April 15 |

| S Corporation | Form 1120-S | March 15 |

| Corporation | Form 1120 | The 15th day of the fourth month after the end of the company’s fiscal year. |

| Individual | Form 1040 | April 15 |

| LLC Taxed as a Corporation | Form 1120 | April 15 |

| Single-member LLC | Schedule C, Form 1040 | April 15 |

| Sole Proprietor | Schedule C, Form 1040 | April 15 |

4. Attach the right forms

Business credits and deductions come with specific forms you have to file.

To get started claiming business tax credits, complete Form 3800, General Business Credit, and attach it to your tax return. You must include supplemental forms for specific credits.

For example, here are a few of the supplemental forms you’ll need:

5. Keep detailed records

Detailed records are the name of the game when making a deduction or a claim (say that five times fast). Without detailed records, you can’t substantiate any of your claims. And if you can’t do that, you may find yourself in hot water with the IRS.

Here are some things you should keep in mind when trying to keep detailed records:

- Record your business transactions diligently

- Keep copies of receipts and previous tax returns

- Use accounting software to simplify your recordkeeping responsibilities

Make tax time simple with Patriot’s accounting software. Easily track your expenses, record payments, and automatically import bank transactions. Try it for free today!

This is not intended as legal advice; for more information, please click here.

{kind=link}