Cash flow problems happen—often. It’s why 82% of small businesses fail. But if you have issues with your cash flow, you’re not doomed to close up shop. Instead, it’s like coming to a fork in the road. Turn right to power through, or turn left to call it quits. To get out of the red, learn what to do when your business runs out of money.

Why is my small business running out of money?

If you dip into negative cash flow territory, your knee-jerk reaction might be to demand answers. Did I do this? Did the economy do this? Is it temporary? Permanent? Why exactly is my business running out of cash?

According to PNC, four factors are most commonly to blame for cash flow problems:

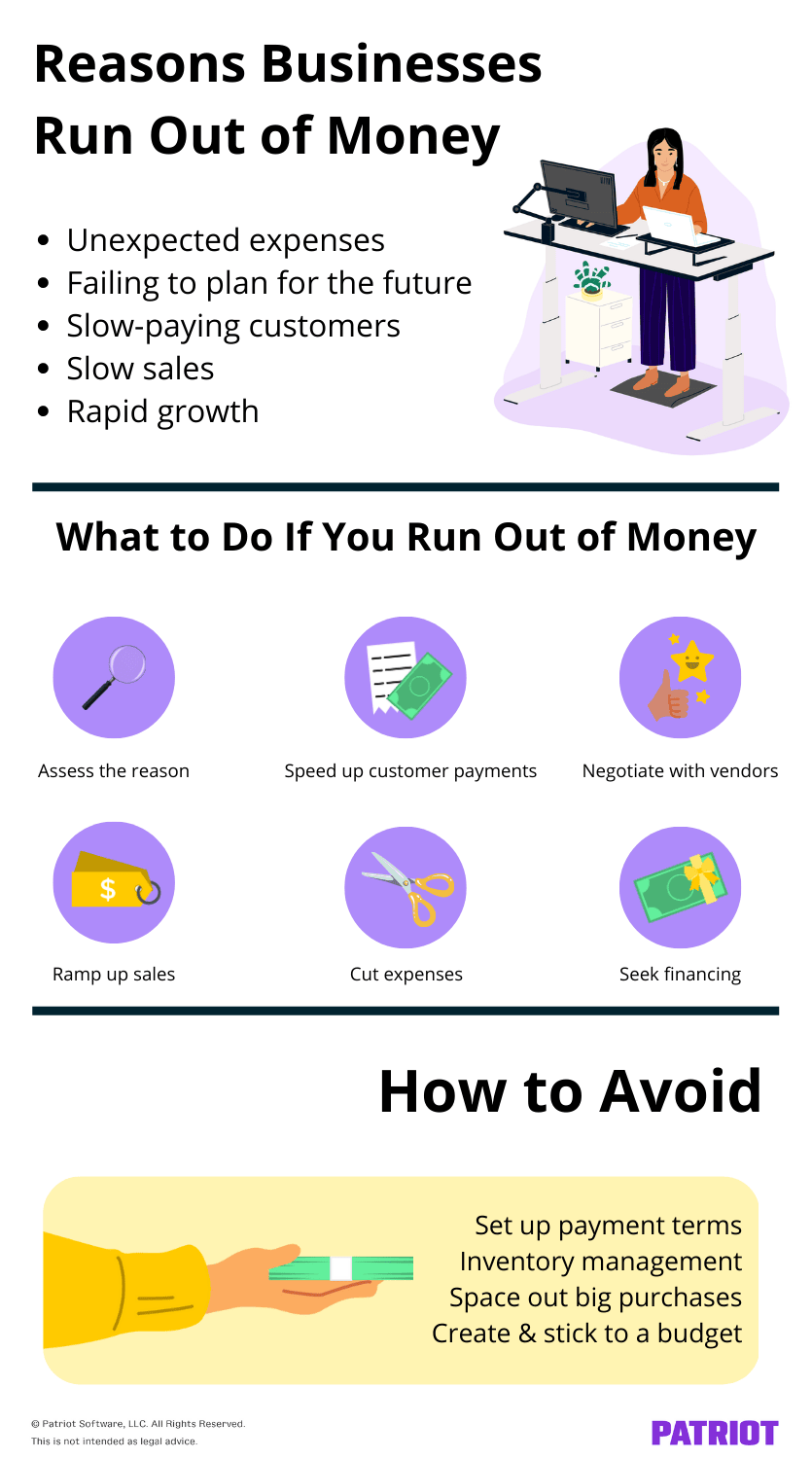

- Not paying attention to expenses (e.g., unexpected expenses, overspending, etc.)

- Uncertainty about future cash flow (i.e., failing to plan for future months with a cash flow projection)

- Slow-paying customers (do you have policies to ensure customers pay on time?)

- No plan for collections (do you have a process to collect on unpaid bills?)

Sure, unexpected expenses and failing to budget are common reasons businesses run out of money. But, the other reasons revolve around getting your customers to pay you on time. So when your business runs out of cash, your customers may be a great source of income (which we’ll cover later).

There are other reasons money might be tight. For example, rapid growth may cause you to purchase more inventory, scale operations, and hire more employees. You may temporarily run out of cash as you prepare for growth.

If you pay employees biweekly, keep an eye on cash flow during 3-paycheck months. Generally, you pay employees twice per month under a biweekly schedule. But, there are two months per year when you must pay employees an “extra” third paycheck.

Another reason for low cash is slow sales. Slow sales may be due to seasonality, market conditions, a drop in customer demand, an increase in competition, or a combination.

What to do when your business runs out of money

First things first: Don’t panic if you run out of cash! Running out of money doesn’t mean your business dream is over. In fact, it takes most businesses three to four years to even become profitable.

To make up for periods of low cash, check out the following tips.

1. Assess the reason

If you’re suddenly out of cash, figuring out why is a good place to start. That way, you can put an effective solution in place that addresses the root cause. Assessing the reason can also help you from making the same mistake in the future.

When determining why you ran out of money, ask yourself some questions. Did it happen over time (e.g., was there a gradual decline in sales)? Or, did it come on suddenly because of poor planning or timing (e.g., a major expense you weren’t prepared for)?

To find out, look at key financial records like:

- Accounts receivable aging reports

- Receipts and bank statements

- Your business budget

- Income statement

- Cash flow statement

- Year-over-year metrics (if applicable)

More than likely, you won’t be able to blame one thing for the cash drought. Instead, it’s likely a culmination of factors. List out possible events you can directly attribute to your small business running out of money. Then, map out specific strategies to prevent it from happening in the future.

2. Speed up customer payments

You love your customers. Without them, you wouldn’t have a business. But sometimes, they make you want to scream—like when they don’t pay their bills on time. Slow customer payments can spell disaster for your bottom line.

Many businesses run out of money due to slow customer payments. To get out of the pit of despair, you need to speed things up. You’d be surprised how quickly your situation changes when the payments start pouring in.

Take a look at the following must-try tips to speed up customer payments

- Create clear invoice terms and conditions: Leave no room for confusion. Your invoice should clearly state how much is due, when it’s due, and the payment methods you accept.

- Track receivables with an accounts receivable aging report: This report generally breaks up customer invoices into a few intervals to show you the number of days an invoice is past due (e.g., 1-30 days, 31-60 days, etc.).

- Offer an early payment discount: An early payment discount gives customers who pay ahead of time a small price cut on their final bill.

- Send out invoice reminders: Sometimes, one invoice doesn’t cut it. You may need to send out several reminders to get customers to pay their bill. If you use accounting software, you may be able to set up automatic invoice reminders.

- Apply a late payment fee: Want to limit the number of customers who pay late—and give yourself a little extra money when they do? Apply a late fee to customers whose invoices are past overdue—and let them know about it ahead of time.

If your customers still aren’t paying you and you need quick capital, you might consider invoice factoring. Keep in mind that you won’t receive the full amount the customer owes you if you turn to invoice factoring.

Create & track invoices with Patriot’s accounting software.

Create, send, and track invoices for as many customers as you need.

3. Negotiate with vendors

Don’t have enough money to pay your bills? If you have a strong relationship with your vendors, they may be apt to work with you on upcoming payment terms.

You might ask your vendors to:

- Work out discounted rates

- Set up a payment plan

- Extend your payment due date

4. Ramp up sales

Sometimes, a slow sales month is the reason you run out of money. So, driving sales can be a great way to get out of the slow sales slump. But, ramping up sales is easier said than done—especially if slow sales are due to seasonality.

To drive sales when your business runs out of money, you can:

- Advertise upcoming sales events

- Offer discounts or send out coupons

- Create a customer loyalty program

- Adjust your pricing strategy

- Introduce new products or services

- Remove friction in the buying process (e.g., optimize your e-Commerce store)

5. Cut expenses

Want to know how to run a business with no money? Make sure you have no immediate expenses. If necessary, cut out some expenses until you get cash flowing again. In some cases, you may opt to permanently get rid of unnecessary expenses.

Decide which expenses you can scale back on and which to cut altogether by looking at your bank statements, budget, and accounting records.

If you can’t scale back on or eliminate the expense, consider finding a less expensive alternative with another vendor or provider.

6. Weigh your financing options

If your business runs out of money and you need capital ASAP (e.g., you have a payroll to run), you may need to weigh your financing options.

To get money for your business, you may apply for a business credit card or take out a small business loan. Or, you might turn to family and friends, take out of your personal savings, or work with an investor.

Consider hiring an accounting professional to discuss whether taking on debt is the right move for your business.

How to prevent your small business from running out of money

Whew. You’ve put the panic of your small business running out of money behind you. Now, how can you prevent it from happening again?

There are several ways to avoid running out of money in the first place or prevent it from happening again, such as:

- Creating and sticking to a budget

- Setting up clear customer payment terms

- Improving your inventory management

- Spacing out big purchases

- Cutting unnecessary expenses permanently

- Thinking of creative ways to drive sales during slow seasons (e.g., sales)

Sometimes, poor cash flow is inevitable. To protect your business from completely running out of money, set up a cash reserve. A cash reserve is an emergency fund you can use to meet unplanned, short-term financial needs (without taking on more business debt!). You can start setting up your cash reserve by putting aside money each month.

Track your expenses, income, and money with Patriot’s accounting software. Get started with a free trial and enjoy easy onboarding, free USA-based support, and more!

This is not intended as legal advice; for more information, please click here.

{kind=link}