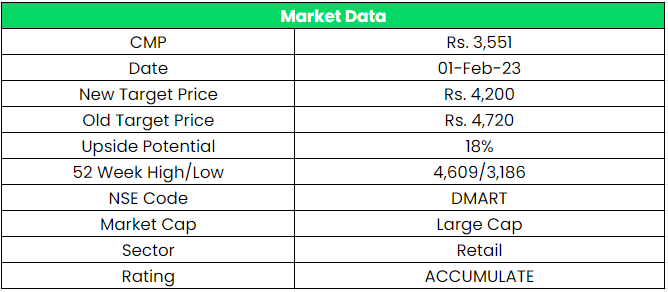

Avenue Supermarts (DMart) Ltd. – Wealth Builder

Avenue Supermarts Limited is an India-based company, which owns and operates DMart stores. DMart is a supermarket chain that offers customers a range of home and personal products under one roof. The Company offers its products under various categories, such as bed and bath, dairy and frozen foods, fruits and vegetables, crockery, toys and games, kids apparel, ladies’ garments, apparel for men, home and personal care, daily essentials, grocery and staples, and own DMart brands.

The Company opened its first store in Mumbai, Maharashtra in 2002. As of December 31, 2022, the Company had 306 operating stores with a Retail Business Area of 12.6 million sq. ft across Maharashtra, Gujarat, Daman, Andhra Pradesh, Karnataka, Telangana, Tamil Nadu, Madhya Pradesh, Rajasthan, NCR, Chattisgarh, and Punjab.

Products & Services:

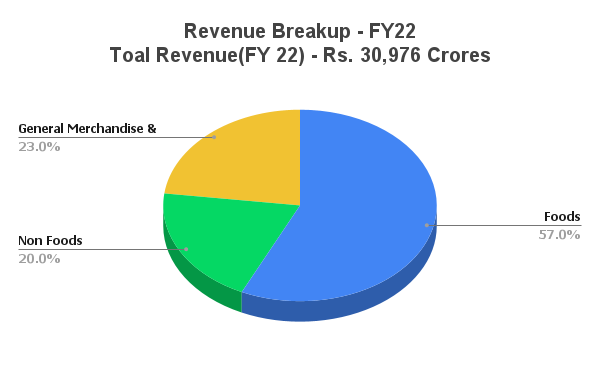

The company has a wide range of products under three segments.

- Foods – This category includes staples, groceries, snacks & processed foods, dairy & frozen products, beverages, and confectionery.

- Non-Foods (FMCG) – This category includes home care products, personal care and toiletries, and other over-the-counter products.

- General Merchandise & Apparel – This category includes bed & bath products, toys & games, home appliances, crockery, utensils, plastic goods, garments, and footwear.

Subsidiaries: As on Mar’22, the company has 5 subsidiaries.

Key Rationale

- Strong position in the organized retail segment – Market position is reinforced by steady same-store growth (barring fiscal 2021), retail productivity, and short gestation for new stores. Avenue Supermarts currently operates 306 stores (as on Dec’30, 2022) under the DMart brand. Strong procurement abilities, low-priced products along with high-cost control will lead to greater footfall. This results in high inventory turnover and revenue per square foot (sq ft) and translates into industry-leading retail store productivity. Aggregate revenue per sq. ft at about Rs.27,454 in fiscal 2022 (Rs.27306 in 2021) is higher than most retailers in the same segment. Currently, the operations of the company are largely concentrated in West and South India. Expected large cluster-focused store addition over the next three years will help diversify geographical reach. Track record of outpacing peers in growth, strong merchandising, compelling value proposition, and benefits of economies of scale will strengthen the market share of DMart over the medium term.

- Q3FY23 – Avenue Supermarts reported a revenue growth of 26% YoY in Q3FY23 to Rs.11569 vs. Rs.9218 crs in Q3FY22. The company added four new DMart outlets (22 in 9MFY23) taking the total store count to 306 with a total business area of 12.6 million sq ft. The average square feet of new stores added is around 60000 (vs. FY22 average of ~41000). D-Mart ready online business) continues to perform well with revenue growth of 72% YoY to Rs.264 crs. Revenue per sq ft did witness a marginal improvement on a YoY basis (~3% YoY) to Rs.9182.

- New Segment – DMart has entered into a new segment by commencing a pharmacy shop-in-shop through its subsidiary (Reflect Healthcare and Retail Private Limited). Currently, the project is in the pilot stage. The Management highlighted that the new segment will complement its current business model as it utilizes existing store infrastructure and no separate Capex is required. Please note D-Mart already sells OTC products, however, more clarity on the pure pharma portfolio is pending from the management.

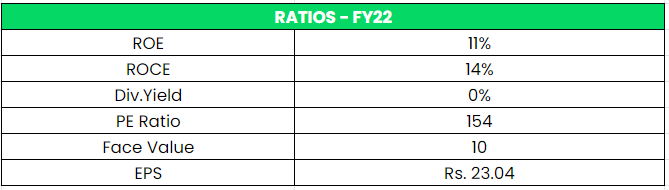

- Financial Performance – Despite capital intensive strategy, the company has maintained high ROE and ROCE in comparison to the industry. The company has generated a revenue CAGR of 30%, an EBITDA CAGR of 34%, and a PAT CAGR of 38% for the period of FY13-22. The net cash flow from Operations grew at a 3-year 21% from Rs.1153 crs in FY19 to Rs.2050 crs in FY22.

Industry Analysis

The retail market in India has undergone a major transformation and has witnessed tremendous growth in the last 10 years. Indian retail market is projected to reach approximately $2 Trn by 2032 from 690 $ Bn in 2021. India currently has the 4th Largest retail market in the world. Indian retail market recovered from pandemic lows and grew 10% YoY from 630 $ Bn to reach 690$ Bn in 2021. The retail sector in India contributed ~800 Bn to India’s GDP in FY20 and employed 8% of its workforce (35+ Mn). It is expected to create 25 Mn new jobs by 2030. The overall retail industry is estimated to have grown by 16-17% in FY2021-22 and within this, the organized brick-and-mortar industry is estimated to have grown by 19-21%. E-Commerce continued its acceleration during FY2021-22. Consumer adoption of E-Commerce continued during the year. The industry is estimated to have grown by 27-32% during FY2021-22. Within the E-Retail, Food & Grocery segment continued to see strong growth in FY2021-22.

Growth Drivers

- By 2030 India will add 140 mn middle-income and 21 mn high-income households – Leading to a huge emerging middle class.

- Rural per capita consumption will grow 4.3 times by 2030, compared to 3.5 times in urban areas.

- India’s retail trading sector attracted US$ 4.11 billion FDIs between April 2000-June 2022. 100% FDI in single-brand retail under the automatic route.

Peer Analysis

Competitors: Vmart, Trent, etc.

D-Mart is the only successful retail business even in the pandemic times compared with its peers. It is easily understood through the comparison that D-Mart has a healthy RoE and RoCE with a strong EPS in FY22. The company is continuously generating operating cash flow which is used in the expansion of further stores.

*Took TTM EPS & P/E for Comparison

Outlook

The company has been on an expansion spree in the last 3 years with an impressive square feet addition. The average size of new stores is 60000 square feet vs. 35000 square feet a few years back (3 Year CAGR of ~22%). The Management highlighted that FMCG and staples continued to outperform the general merchandise and apparel segment. On the account of festive purchases in the General Merchandise & apparel segment, Q3 generally tends to yield gross margins in excess of 15%. However low gross margin (14.8%) recorded in Q3FY23 reflects some challenges in the short term, which could possibly be on account of heightened competitive intensity over the past two years and inflationary stress still pertaining to the discretionary value segment. Irrespective of the situation, D-Mart continues to remain India’s most profitable low-cost retailer, a strong play on India’s retail growth story, and a key beneficiary of the unorganized to organized segment shifts.

Valuation

We believe the recovery in sales of general merchandise and apparel segment is around the corner as FMCG companies are likely to pass on the lower raw material price benefits to the consumers. Moreover, the RBI’s stance on controlling the overall inflation will benefit the lower end of the customers which will increase the overall demand cycle. Hence, we recommend an ACCUMULATE rating in the stock with the target price (TP) of Rs.4200, 70x FY25E EPS.

Risks

- E-Commerce Risk – There has been a significant shift in consumer behavior post-Covid-19 – towards online commerce. Underinvestment in online grocery would hurt DMart’s market share. Online would hurt DMart’s margins, as typically online accounts for lower sales of general merchandise, which has high margins.

- Free Cashflow Risk – DMart owns a majority of the stores, as it buys real estate. With strong store opening capex, FCF generation over the next couple of years could remain subdued and could get delayed even more if leased store openings are low.

- Competitive Risk – Sustenance of everyday lower prices is critical for the success of the company. However, with increasing competition, the company could be forced to increase discounting to maintain its loyal customers and its competitive advantage. This would impact margins that are already wafer-thin.

Source – Tickertape, Company’s Website, BSE Website

Other articles you may like

{kind=link}