Seasoned financial advisors have likely worked with clients with a wide variety of workplace retirement accounts, which can vary in terms of their investment offerings, fees, and other characteristics. But given that the U.S. government is the largest employer in the country, it can be especially helpful for advisors to be familiar with the ins and outs of (and recent changes to) the Federal government’s own defined contribution plan: the Thrift Savings Plan (TSP).

The TSP is available to both civilian Federal government employees as well as military servicemembers, and those who have left service can choose to maintain their TSP accounts (though they can no longer make contributions). While many features of the TSP (e.g., Roth contribution options and employer matches) are common to other workplace-defined contribution plans, the TSP has certain unique attributes, including lower fees than many private-sector plans and a fixed-income investment option exclusive to the plan.

In 2022, the TSP underwent a series of changes impacting its many account holders. These include the opening of a “Mutual Fund Window” to supplement the limited offering of investment funds previously available to plan participants (though the associated expenses make it prohibitively expensive for many participants). In addition, the TSP updated its website and introduced a smartphone app, which required participants to create new credentials and verify their personal information. Notably, advisors can support clients in navigating these new changes by helping them decide if investing through the Mutual Fund Window makes sense, walking them through the registration process for the new site (if they have not already), and ensuring that their information (including beneficiary information) transferred over correctly.

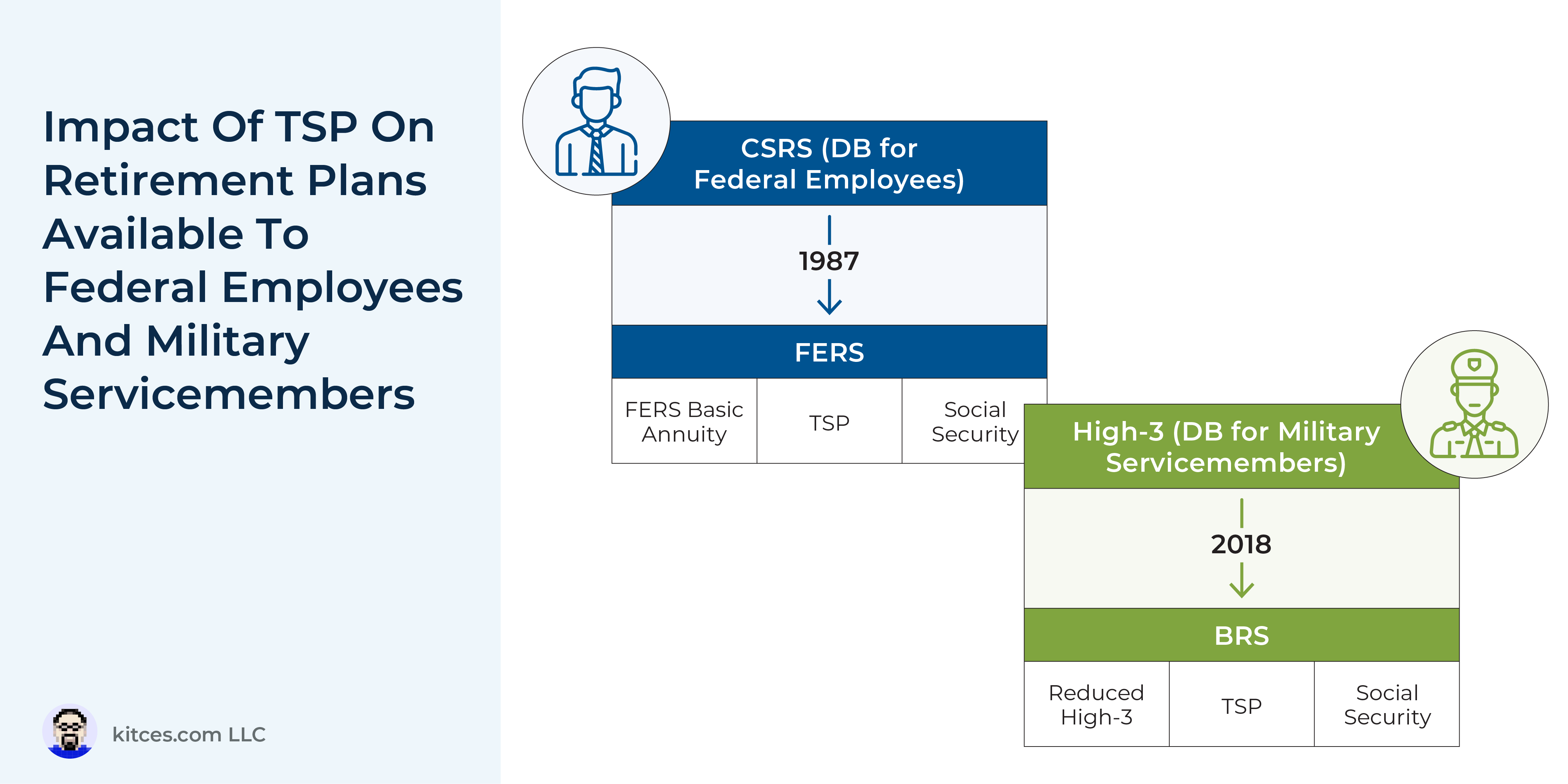

Advisors can also add value for clients who are TSP participants by understanding how the TSP fits within the Federal employee and military retirement systems, which combine the defined contribution TSP feature with a defined benefit pension (though because the value of this pension has been reduced, TSP management has increased in importance). Further, advisors can support these clients by helping them manage the retirement savings choices that come with career transitions; for example, because many military members have ‘encore’ careers (as they are often eligible to retire well before ‘traditional’ retirement age), balancing their cash flow and retirement savings needs is crucial during their transition period.

Advisors working with clients who have been deployed to combat zones can also add value by being aware of the related TSP considerations. For instance, because income earned while deployed in a combat zone is tax-free, any pre-tax TSP contributions can result in a commingling of tax-free combat pay and taxable earnings (though this can be prevented by making Roth contributions during periods where income is untaxed). In addition, the annual deferral limit increases significantly during the year of a combat deployment, providing an opportunity to contribute even more money to the TSP (if doing so fits within the client’s cash flow plan).

Ultimately, the key point is that while the TSP is similar to many other workplace retirement plans, advisors who understand its unique attributes and stay up to date with its ongoing changes can better serve the Federal employees and military servicemembers who participate in the plan. And given that there are about 6.2 million TSP account holders, these individuals represent a large potential pool of clients!

{kind=link}