MeKenna and Kat are both on the Support team for YNAB. In addition to working for YNAB, they’re both side hustlers: freelance lighting designer (MeKenna) and freelance actor/performer (Kat). Put their suggestions for managing side hustle expenses and income in YNAB into action in your own budget to eliminate some of that tax-time stress!

Regardless of what kind of work your side hustle entails, finding the right processes, tools, or systems to help can make life a whole lot easier. While we both manage our side hustles a bit differently in our budgets, we agree that we couldn’t imagine managing the expenses and income without YNAB.

One thing we do have in common is that all our side hustle income and expenses go into and come out of our personal accounts. This works best for our personal setup, but if you have a separate bank account for your business, a separate business budget is the way to go! Check out this link to our Small Business landing page with lots of resources on setting up a separate business budget.

How to Manage Tax-Deductible Expenses

Option One: Tagging

Kat’s approach:

I took the list of deductible expense categories I got from my accountant and made note of the ones that apply to me. When I spend money for the business, I add my business tag for the year (#katwork22) and the spending type to the memo field. For me, that’s subscriptions, training, transportation, meals, supplies, costumes, and travel.

I add the tag and the spending type to the memo field of any deductible spending. If I bought multiple things in that purchase and only some of them are deductible, I’ll split the transaction and add the information only to the memo field of the corresponding split. For recurring deductible expenses (subscriptions, cell phone bills, etc.), I make sure that the tag is in the memo field of the scheduled repeating transaction for more automation. When the new year comes around and the January transaction drops in with the past year’s date, I just have to remember to update both the January version of the transaction and the repeating future transaction with the new date tag!

The beautiful part about this for me is that the tax category doesn’t have to correspond with the spending category in my budget. I might categorize a workshop under a business category like Performing Expenses, but I might categorize a costume piece I bought to my regular Clothing category. I might want to fund that parking charge in my usual Transportation category, but I want to make sure to write it off on my taxes.

Option Two: Flagging

Now that you can add custom names to flags, they’re also a great alternative to the side hustle tag. You can use one color for all tax-deductible expenses or you can use one for each type of spending: red could be side hustle meals, yellow could be side hustle travel, etc. The only downside of using flags is that you can’t flag a split portion of a transaction, only the full transaction. If you use split transactions for your tax-deductible spending, the tags in the memo field are a better way to go.

Tax Preparation

When tax time comes around, I search for each type of spending and the tag – “#katwork22 training.” For the simplest approach, I can select all the transactions and the Selected Total at the top is what I spent in that category. I can add that to the spreadsheet I share with my accountant.

Alternatively, I can search for just the business tag (in my case, #katwork22), select all the transactions in all those spending types, and Export Selected Transactions to a spreadsheet app. From there, I can sort by the different tax deductible categories and send that along to my accountant.

If you choose to use flags, you can search for flags and follow the same instructions as above!

What to do if one year’s spending is distributed over more than one budget

Maybe you decided to do a fresh start mid-year. Or maybe you’re like Kat — you filed for divorce in the middle of the year and had to create a new budget with new accounts in July! No matter the reason, sometimes having more than one budget that holds transactions in a single year is unavoidable. Here’s how to merge the data into one place!

First, you’ll go to All Accounts and search for your business tag. Select all the transactions for that tax year and use Export Selected Transactions to create a CSV file of just those transactions. Do the same thing in the other budget(s). When you’re finished, you’ll have two or more CSV files with the relevant spending transactions in them.

You can pick one file to be the main file. Next, open the other one, copy all the transactions (without the header) from that budget and then paste all the transactions into the main file. Repeat until all transactions for that year are in one file. From there, you can delete columns you don’t need, sort and filter as desired.

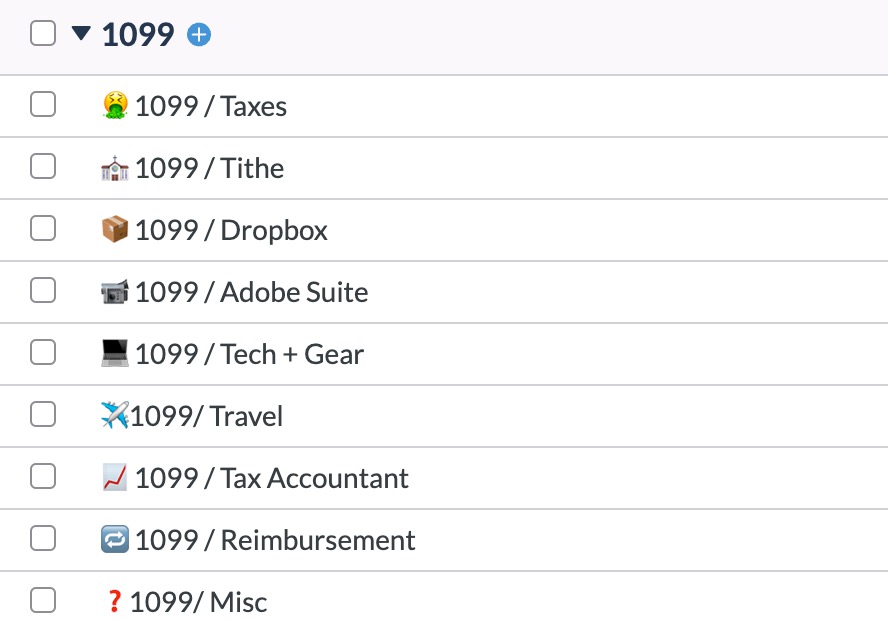

Option Three: 1099 Category Group

MeKenna’s approach:

I have a category group called “1099” and inside of it are all 1099-related categories. Taxes, Tithing, Dropbox, Adobe Suite Subscriptions, Tech & Gear, Travel for Work, Tax Accountant, Reimbursements, and Miscellaneous. You can customize this to be your work-related categories, or keep them all contained within your current budget setup like Kat does. Or some combination of both!

Here’s my setup:

Categorizing and Tracking Side Hustle Income

1099 income isn’t taxed until you file at the end of the year, which can cause two challenges: not having enough set aside when it comes time to pay taxes and inflated income data in YNAB. If you are both an employee and an independent contractor, the paychecks from your employer are the post-tax amount but your side hustle payments are the pre-taxed amount. Kat and MeKenna have two different approaches to these challenges!

MeKenna’s approach:

In my budget, I want to separate my 1099 income and the taxes that I take out of it, so I use a split transaction. The payee is the name of the income source and I click Split in the category field. I personally like to set aside 20% for taxes, so if the invoice is for $2,000, I categorize $1,600 as “Inflow: Ready To Assign” and $400 to my Tax category.

That way, my Income v. Expense report shows my approximate net income instead of gross income for just my 1099 pay. And it also helps me remember to set aside money for self-employment taxes!

Kat’s approach:

The majority of my side hustle income comes in a few annual checks. I’m not too worried about the accuracy of my income data, so I categorize the full inflow amount to Inflow: Ready to Assign. Then I assign a chunk of it to the tax category to make sure I have some set-aside. I set a Target on my tax category so I set aside about the same amount I had to pay last year. Once I’ve fully funded that target for the year, the rest of the 1099 income is free to be assigned anywhere else.

When deciding how to categorize your side hustle income, keep in mind that any money inflowed into a category won’t show as income in reports. If your goal is for your income in YNAB to show as net income, splitting some of the inflows to the taxes category will more accurately reflect that net income.

If you like to see your income by income source/client, you can use distinct payees for each and check the Income v. Expense report to see how much you were paid by each client.

Check out more Fast Tax Time Prep Tips with YNAB

If You Have Separate Business Bank Accounts

As mentioned above, if you have separate accounts for your business, you’ll want to add them to a separate business budget, rather than to your personal budget. That way, you’ll be able to separate personal and business income. You’ll also be able to distinguish between business and personal expenses more easily.

We hope we’ve given you some strategies to apply to this year’s budget (or if you’re like some of us, you may go back and tag all of last year’s expenses to make tax time easier!)

Don’t hesitate to reach out to the Support team if you have any questions about setting this up in your budget!

Are you a freelancer who stumbled upon this post while searching for a better way to manage your finances? With Four Rules, a robust library of free resources, and an award-winning money management app, YNAB has everything you need to take control of your financial life and enjoy less money stress. Try it for free today, no credit card required!

{kind=link}