Bharat Electronics Ltd. – Defence Electronics Leader

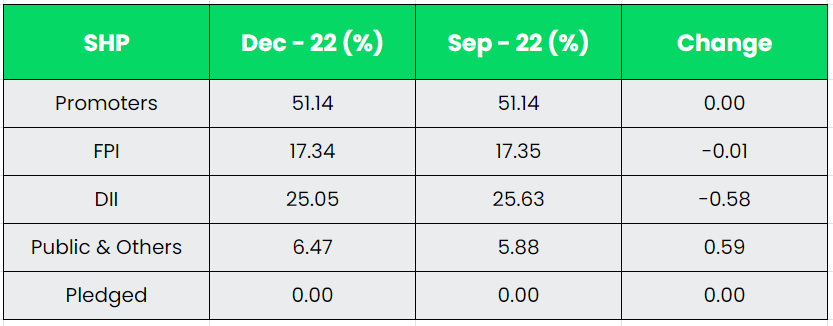

BEL, a Navratna defence public sector undertaking (DPSU), was established in 1954 under the Ministry of Defence, the GOI, to cater to the electronic equipment requirements of the defence sector. The GOI remains BEL’s largest shareholder with the current shareholding of 51.14%. BEL was conferred the Navratna PSU status in June 2007.

BEL is the dominant supplier of radar, communication and electronic warfare equipment to the Indian armed forces. The company has nine manufacturing units across India and two research units. The Bangalore and the Ghaziabad units are BEL’s two major units, with the former contributing the largest share to the company’s total revenue and profits.

Products & Services:

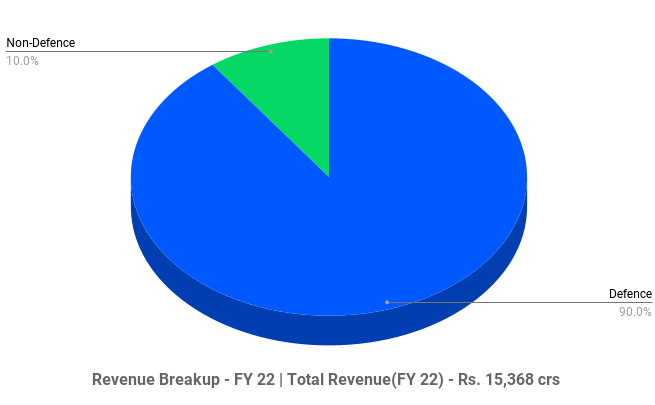

The Company designs, manufactures and supplies state-of-the-art products and systems in a wide variety of fields including Radars, Missile Systems, Military Communications, Naval Systems, Electronic Warfare & Avionics, C4I Systems, Electro Optics, Tank Electronics & Gun/Weapon System Upgrades, and Electronic Fuzes in the Defence segment. BEL’s non-Defence business segment includes areas such as Electronic Voting Machines, Homeland Security & Smart Cities, Satellite Integration & Space Electronics, Railways, Artificial Intelligence, Cyber Security, Software as a Service, Energy Storage Products, besides Composite Shelters & Masts.

Subsidiaries: As on 31st Mar 2022, the Company has 2 subsidiaries and 2 Associate companies.

Key Rationale:

- Strong Market Position with high entry barrier – Bharat Electronics Ltd (BEL) is the leading player in the India’s defence electronics sector with a market share of more than 50%. It helps in most of the country’s defence electronics needs. The company has a strong competitive advantage with its dominant position, established infra and facility, Association with the Indian army and strong R&D. Added to the above, the high entry barrier status of the underlying sector will give more advantage to the company.

- MOU with Triton EV – BEL has signed a MOU (Memorandum of Understanding) with US based Triton EV for Manufacturing Hydrogen fuel cells to meet the requirements of the Indian market and mutually agreed export markets. It also issued an LOI (Letter of Intent) to BEL for procurement of 300 KW Li-Ion Battery packs for its Semi-truck project in India at a value of Rs.8060 crs. The said battery packs are to be delivered to Triton in 24 months which was said to commence from Jan’23. These deals are a huge positive for the company to diversify its revenue from its over dependency on Defence segment.

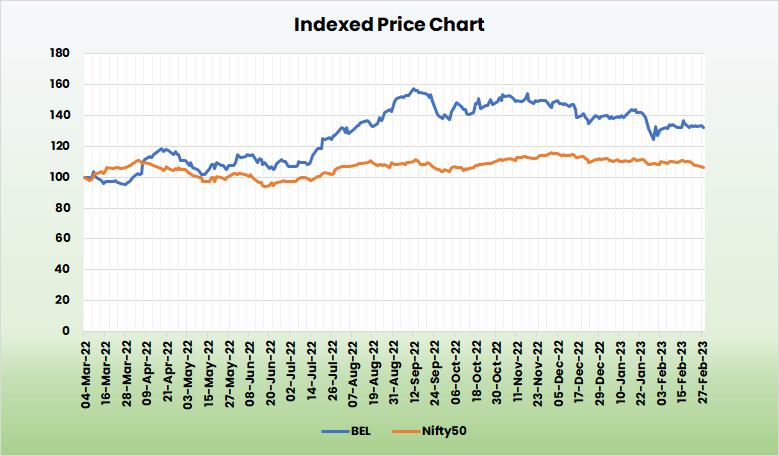

- Q3FY23 – The company reported consolidated revenue growth of 12% YoY to ~Rs.4153 crs. The YoY growth was primarily driven by better execution. EBITDA increased by 4% YoY basis at Rs.863 crs as the revenue growth of 12% has been negated by contraction in margins. Sequentially, EBITDA remained largely flattish. EBITDA margins declined by 160 bps on YoY basis to 20.8% in Q3FY23. The orderbook position of the company was at Rs.50116 crs as of December 2022 end (~2.9x TTM revenues). Almost 80% of the total orderbook caters to Defence segment. Implied order inflows were at Rs.1452 crs during Q3FY23 and Rs.3736 crs during 9MFY23.

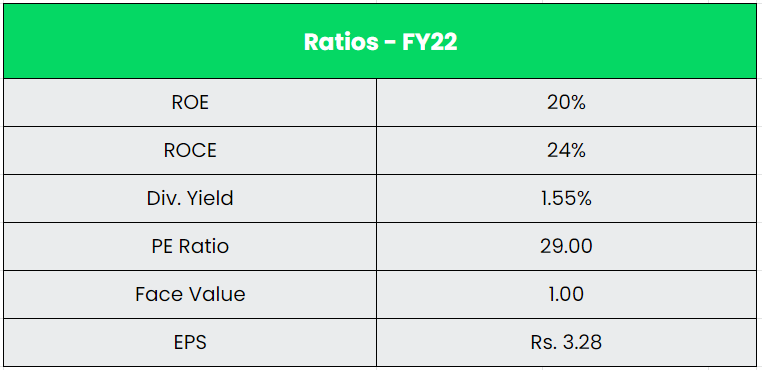

- Financial Performance – The company’s 4 Year Revenue and PAT CAGR stood at 10% and 14% between FY18-22, respectively. The Cashflow from operations of the company grew at a CAGR of 41% between FY19-22. The Free cash flow of the company grew at a CAGR of 67% for the same period. The company is financially strong with consistent profitability, cashflow generation and a zero-debt balance sheet with strong internal accruals for expansion.

Industry:

The Indian Defence sector, the second largest armed force is at the cusp of revolution. The Government has identified the Defence and Aerospace sector as a focus area for the ‘Aatmanirbhar Bharat’ or Self-Reliant India initiative, with a formidable push on the establishment of indigenous manufacturing infrastructure supported by a requisite research and development ecosystem. India is positioned as the 3rd largest military spender in the world, with its defence budget accounting for 2.15% of the country’s total GDP. The vision of the government is to achieve a turnover of $25 Bn including export of $5 Bn in Aerospace and Defence goods and services by 2025. Till October 2022, a total of 595 Industrial Licences have been issued to 366 companies operating in Defence Sector.

Growth Drivers:

- To promote export and liberalise foreign investments, FDI in Defence Sector has been enhanced up to 74% through the Automatic Route and 100% by Government Route.

- Apart from the Atmanirbhar boost for the sector, the government has also put a ban on import of 411 items of Services and total 3,738 items of Defence Public Sector Undertakings (DPSUs) to support the sector.

- In FY2023-24, Ministry of Defence (MoD) has been allocated a total Budget of Rs.5.94 lakh crore, which is 13.18% of the total budget (Rs.45.03 lakh crore). Capital outlay pertaining to modernisation and infrastructure development has been increased to Rs.1.63 lakh crore.

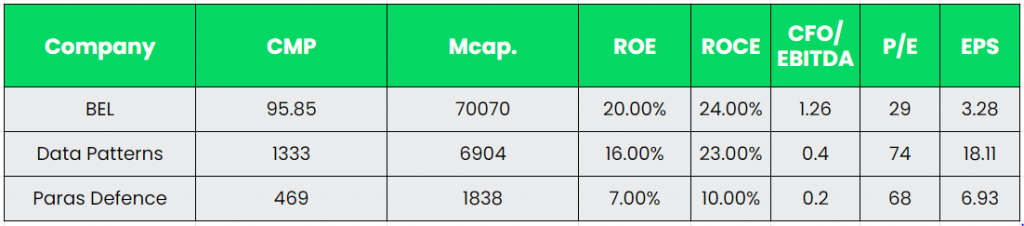

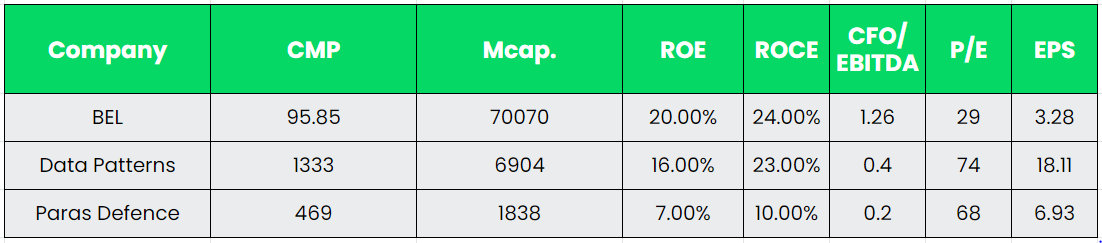

Competitors: Data Patterns, Paras Defence, etc.

Peer Analysis:

In the Defence Electronics sector, BEL is the largest player with strong return ratios and robust cashflow generation. The company’s CFO/EBITDA is more than 1 for BEL which is strong and less than 1 for its peers.

Outlook:

The Management guided a revenue growth of 15% in FY23 and 15-20% thereafter. Gross margin for FY23 is expected to remain at similar level to that in 9MFY23 i.e., at ~42%. They have reiterated the order book inflow of Rs.20,000 crs in FY23 despite having only orderbook inflow of just Rs.3736 crs during 9MFY23. The strong reiteration from the management is based on the expected order inflow of around Rs.15500 crs in Q4FY23. The inflow of Rs.15500 crs is based on the ordering of Himshakti programme of Rs.3300 crs, Atulya medium-power radar of ~Rs.2000-3000 crs and ~Rs.10000 crs expected from naval shipyards for radars and SONAR. The discussions are almost confirmed for Rs.12000 crs worth of orders and the balance Rs.3500 crs is in the various stages of approval. BEL is also expecting its new facilities for defence orders to be completed in next 2-3 years. The company is going to incur a capex of Rs.600 crs in FY23 and Rs.600-800 crs in FY24. BEL is attractive on the basis of a) New order Inflow b) Robust expansion for revenue growth c) Increase in the share of Non Defence revenue. The Management’s focus is to increase the non-defence share to ~20% over two to three years.

Valuation:

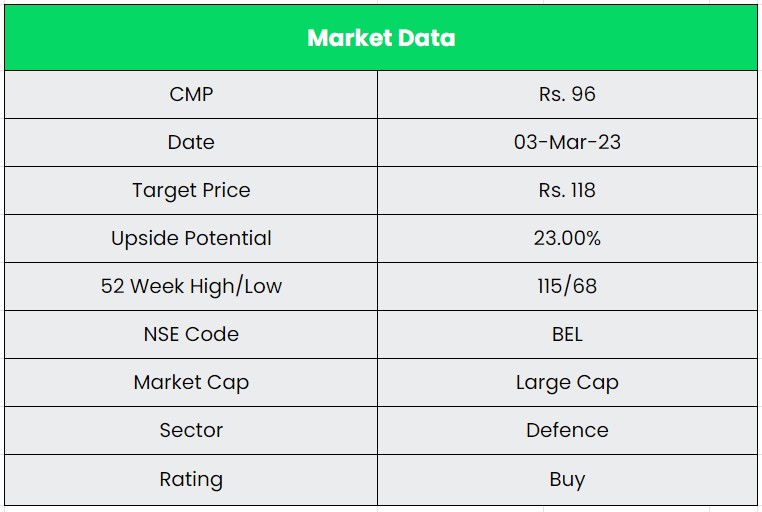

The Company’s sound financial position and a wide product portfolio helped it to attain a major chunk of Atmanirbhar Boost. The Management’s strategy to diversify its revenue, focus on increasing exports will assist the long-term growth of the company. Hence, we recommend a BUY rating in the stock with the target price (TP) of Rs.118, 27x FY24E EPS.

Risks:

- Client Concentration Risk – BEL is deriving more than 85% of its revenue from the Indian defence sector. Any major cut in the defence spending by the Government will significantly impact the order book and thereby revenue.

- Capital Intensive Risk – The company’s operations possess an elongated working capital risk. Since the major customer is the GOI, there is a high chance of delay in the receivables.

- Execution Risk – Any delay in the execution of the orderbook will be a key risk and it will directly impact the revenue of the company.

Other articles you may like

{kind=link}

{kind=link}