How to protect your Cash

Posted

on Mar 15, 2023

on Mar 15, 2023

Many are worried about the security of their money following the collapse of Silicon Valley Bank (SVB) last week. There are numerous approaches that can be taken to safeguard your cash deposits.

Even though the federal government has rescued SVB and guaranteed all deposits over the FDIC insurance limit of $250,000 per account, that doesn’t mean they will be doing it again for other banks.

Let’s review and recap how Federal Deposit Insurance Corporation (FDIC) insurance works and what other alternatives are available.

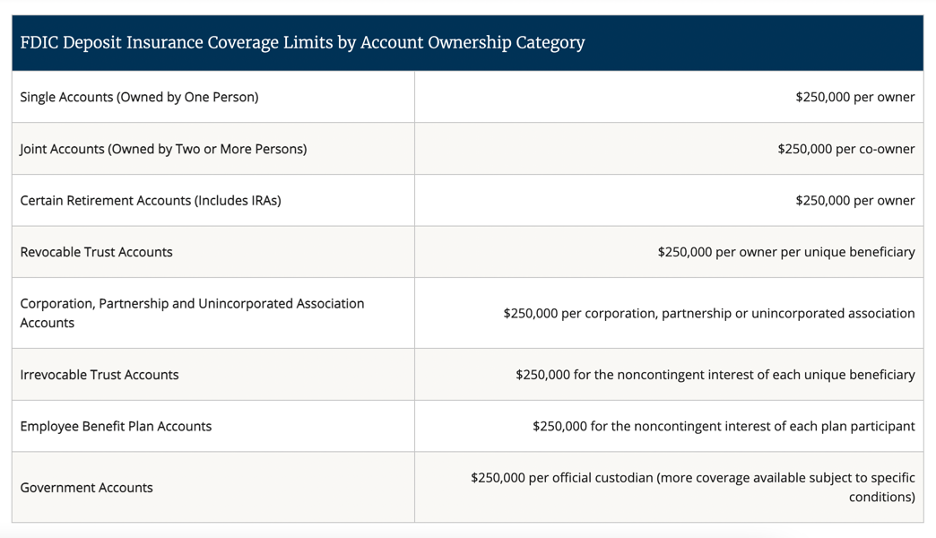

In the United States, any individual account with a balance of up to $250,000 at a bank is insured. Expanding this coverage is straightforward since each type of account at each bank has a coverage of $250,000. For example, a married couple is entitled to $500,000 of protection for a joint account and $250,000 for each of their personal accounts, resulting in a total of $1 million in coverage at a single bank.

Determining the total coverage for trust accounts can be more complex since you will have to examine beneficiary designations.

FDIC also has a very useful calculator FDIC’s Electronic Deposit Insurance Estimator (EDIE). It helps consumers understand how deposit insurance rules and limits apply to their specific group of deposit accounts at a particular bank.

By entering information about their deposit accounts into the EDIE tool, users can generate a report that provides information on how their deposits are insured, what portion (if any) exceeds coverage limits, and what steps they can take to maximize their insurance coverage.

The report can be used to help make informed decisions about how to structure their deposits to ensure maximum insurance coverage.

Are my Retirement Accounts, such as IRA, 401k, or Investment Brokerage Insured?

The Securities Investor Protection Corporation (SIPC) is a non-profit organization created by Congress to protect customers of SIPC-member brokerage firms against the loss of cash and securities in the event of a firm’s financial failure or insolvency.

SIPC provides protection up to $500,000 per customer, which includes a $250,000 limit for cash. This means that if a brokerage firm fails and a customer’s cash and securities are lost, SIPC will work to recover the assets and return them to the customer up to the coverage limit.

It’s important to note that SIPC protection does not cover losses resulting from market fluctuations, fraud, or bad investment decisions. It also does not cover certain types of investments, such as commodities or futures contracts. You should always review your account agreements with each institution and understand the risks associated with the investments.

What you need to keep in mind, just like with the FDIC limit, there is a limit of coverage for Multiple Accounts. SIPC refers to this as “separate capacity”, for example, individual, joint accounts, or trust accounts. Accounts held in the same capacity are combined for purposes of the SIPC protection limits.

Many banks and brokerage firms also offer “excess SIPC coverage” over the SIPC limit. This type of coverage is provided by a private insurer, not SIPC. Exact eligibility is not determined until the limits of SIPC are exhausted. You should contact your brokerage firm if you have questions regarding excess SIPC insurance.

Here are a few most typical brokerage firms our clients have accounts at:

TD Ameritrade Excess SIPC limit

Vanguard Excess SPIC limit – from Vanguard site- “Vanguard funds not held in a brokerage account are held by The Vanguard Group, Inc., and are not protected by SIPC. Brokerage assets are held by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation, member FINRA and SIPC.

A workaround for this could be to convert or move funds into a brokerage account.

What if I have my cash accounts with a Credit Union?

Credit Unions, similar to banks, have insurance up to $250,000 per account, but credit unions are insured by the National Credit Union Administration (NCUA). This means that if your credit union was to fail, your deposits would be protected up to that $250,000 amount. You can check if your credit union is insured by the NCUA by using the “Credit Union Locator” tool on their website and looking for the blue NCUA logo.

Similar to the FDIC coverage estimator EDIE, credit union members can estimate what their “Share insurance” coverage is thru Share Insurance Estimator.

Money Market Accounts vs Money Market Funds

While both a money market account and a money market fund have the word “money market” in their name and are used for short-term savings or investment purposes, they are quite different financial products with unique features and risks.

A Money Market Account is a type of savings account that is typically offered by banks or credit unions. It usually offers a higher interest rate than a traditional savings account, but also requires a higher minimum balance. Money market accounts are FDIC-insured up to $250,000 per account, meaning that your money is protected in case the bank or credit union fails. With a money market account, you can withdraw your money at any time, but there may be limits on the number of withdrawals you can make per month.

On the other hand, a Money Market Fund is a type of investment fund that invests in short-term, low-risk debt securities such as treasury bills, commercial paper, and certificates of deposit. Money market funds are typically offered by investment companies and can be purchased through a broker or directly from the fund, examples, Vanguard, Schwab, Fidelity. Unlike a money market account, a money market fund is not FDIC-insured and is not guaranteed to maintain a stable net asset value (NAV). The NAV of a money market fund can fluctuate based on the performance of its underlying securities, and there is a risk of losing money if the fund performs poorly.

Open Multiple Accounts

It’s important to note that while opening multiple accounts at different banks can increase FDIC coverage or Share Insurance with a credit union, it may not always be the most practical or convenient option for everyone. In addition to the added complexity of managing multiple accounts, there may be other costs associated with maintaining these accounts, such as fees or minimum balance requirements.

“Deposit Swapping”- source wsj.com

A more sophisticated way to manage multiple bank account relationships is to utilize a Deposit Swapping Service. You enroll in a service such as IntraFi and utilize their network of banks that participate in ICS and CDARS programs to provide coverage of multiple millions of dollars of FDIC Insurance. Here is how it works.

Your investment strategy should be aligned with your financial goals and time horizon. Short-term investments, such as cash and cash equivalents, are generally used to meet immediate needs or to serve as a safety net in case of emergencies. However, if your financial goals have a longer-term horizon, it may be more appropriate to consider investing in stocks, bonds, ETFs, mutual funds, or real estate.

These types of investments offer the potential for higher returns over the long-term, but they also come with greater risk. Before investing, it’s important to understand your risk tolerance, investment objectives, and time horizon. You should also consider seeking advice from a financial planner who can help you create a personalized investment plan based on your goals and risk profile.

Ultimately, the key to a successful investment strategy is finding the right balance between risk and reward and staying committed to your long-term goals.

{kind=link}