US stocks are at the center of most investment portfolios. Diversification is still a positive thing, and many investors are looking to balance their portfolios with exposure to emerging markets.

Emerging markets can be tempting, but for many investors, they are a completely new world. Here are some points to consider as you build an emerging market portfolio.

Does Emerging Market Investing Work?

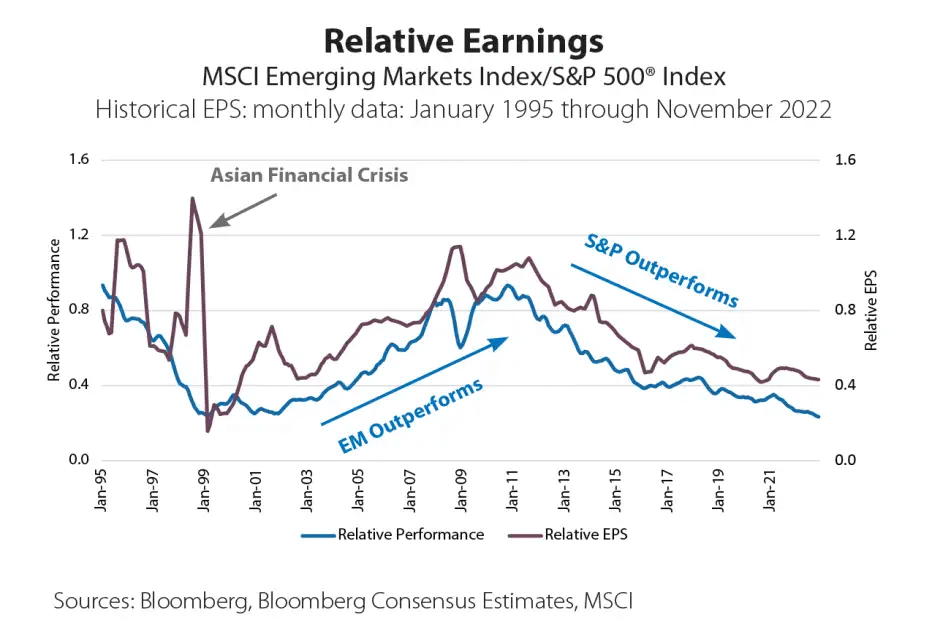

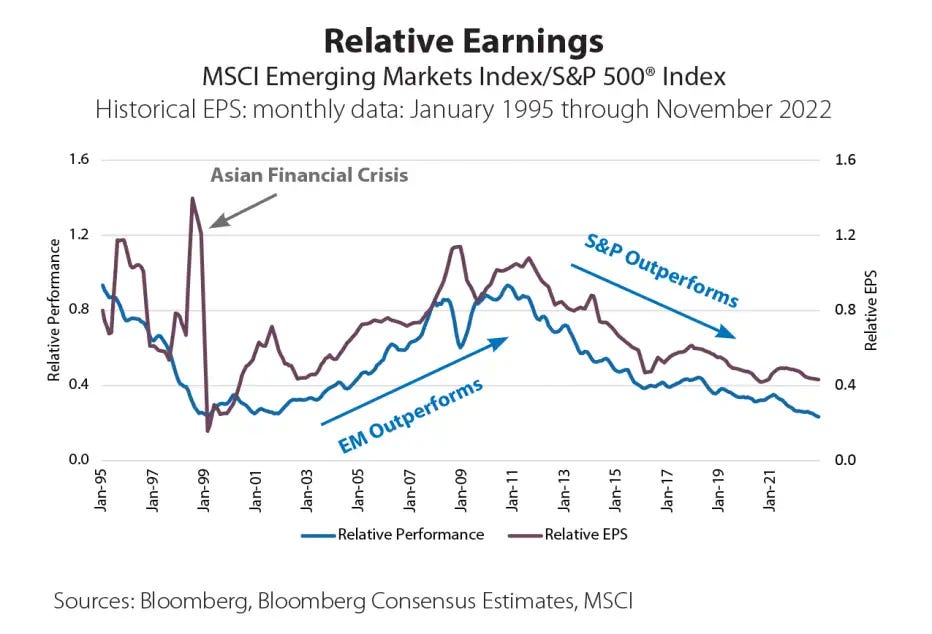

In our previous article on Brazil, we explained how the US and emerging markets tend to follow a roughly 10-year-long cycle of alternating performance.

Looking at an even longer timeline, the MSCI USA index has never been higher compared to the MSCI World Index in 50 years. So it might make sense to expect a reversion to the mean at some point in the future.

There are never any guarantees, but these indicators do suggest that exposure to a diversified emerging market portfolio is a rational move.

Understanding Emerging Markets

Here are some of the features that characterize emerging markets.

Strengths of Emerging Market Investing

One of the key characteristics of emerging markets is their growth profile. Most have shown 5-10% GDP growth over several decades. Investments in such countries have generally done well, as “a rising tide lifts all boats”.

They are also generally countries with young and growing populations. These demographic trends are supportive of economic growth.

Another factor that is very real but hard to quantify is the “grit” of emerging markets. People that have known dire poverty until 1-2 generations ago tend to be hard-working, resourceful, and ambitious. If the entire society is focused on seizing the opportunity and achieving economic growth, this usually pays off.

Dangers of Emerging Market Investing

The first risk with emerging markets is the same argument we started this article with. They tend to outperform in some periods and underperform in others. So investors need to acknowledge that cyclicality and avoid overstaying their welcome.

Another risk is that many emerging countries are not democratic or have weak rule of law. Corruption and legal instability are common, and forced nationalization is always possible. Paying attention to local politics and social situation is a must, as is a diversified portfolio that avoids overconcentration in a single market.

One last problem is the immaturity of these markets. Reporting standards may be low, regulation is often weak, and many companies might not publish their reports in English. Accounting practices might not be up to international standards. Governance might be less than ideal. Finding a broker giving access to these markets can be a challenge. Overall, emerging markets are more complicated and require a lot more due diligence.

Because of the weakness in reporting standards, the difficulty of gaining access to accurate information, and the challenge of finding a broker that handles emerging markets, emerging market portfolios rarely focus on individual stocks. ETFs are a more common vehicle.

Building an Emerging Market Portfolio

Here are some ways to build an emerging market portfolio:

Geographical Diversification

It is easy to see emerging markets as a uniform blob. Most of the time, though, sub-regions will have a common pattern not shared by others.

Historically, specific areas have been known to outperform or underperform for their own peculiar reasons. For example, the 1997 Asian financial crisis or the 1980s Latin American debt crisis.

With geopolitics once again relevant to markets, geographical diversification is a must for any emerging market portfolio. For example, South America and Africa would not be impacted the same way as Asia in case of a Taiwan crisis.

There are a number of common groupings, like the MINT (Mexico, Indonesia, Nigeria & Turkey), The BRICS (Brazil, Russia, India, China, and South Africa), or the “Next Eleven” ( Bangladesh, Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, the Philippines, South Korea, Turkey, and Vietnam).

Country Profile Diversification

Not all emerging markets are the same. Incorporating different macroeconomic profiles in a portfolio can help reduce volatility.

Commodity-Based Economies

Some emerging economies rely on commodities for 80%-90% of their exports. This is most common in Africa and some parts of South America.

This will mean that the economies and even the political stability of these countries are deeply tied to international commodity prices. Sometimes, only one commodity, like cacao, sugar, or palm oil, will be the backbone of the country’s prosperity.

Emerging Industrial Powers

The best example of economies that “emerged” using this template are Japan and South Korea. It is the path currently being followed by China or Poland. The economic growth is built on the back of its integration into the globalized economy, and its ability to manufacture goods at a competitive price.

The cost of labor, quality of infrastructure, political stability, corruption levels, and overall international competitiveness will determine the country’s future success.

Petrostates

Most common in the Arab Gulf region, these are countries whose main added value to the world economy is fossil fuels. These countries will prosper or suffer recession depending on global energy prices and the oil & gas supply and demand.

Middle-Income Countries

These could be called “semi-emerged countries”. They are more developed than most “developing markets”, but not to the West or Japan’s level of prosperity either.

They are at risk of the “middle-income trap“, which describes the situation of an economy failing to transition to high-added value goods, but also trying to develop and grow mainly or solely by exploiting cheap wages or commodity exports.

If they manage to escape this trap, they will go on to become fully developed countries. In many cases, this progress has been impeded by rule of law issues and the dominance of self-interested neo-feudal elites.

Sector Diversification

Not all emerging markets are producing the same goods or are active in the same sectors. Clothes manufacturing in Bangladesh had little to do with car parts manufacturing in Poland or Mexico or call centers in India.

A good emerging market portfolio should be diversified in multiple industries and economic sectors.

Following Known Templates

With globalization at full speed in the last decade, we now have a few proven successful development templates. This gives investors the chance to estimate which emerging markets are the most promising and which are at risk of soon stagnating.

Cheap Labor and Climbing the Industrial Value Chain

This is the pattern followed by Japan and South Korea. And currently imitated by China.

The idea is to first capitalize on cheap and abundant labor for industries like textiles, shoes, toys, and other simple manufactured goods, then progressively use the created capital to buy better machinery, finance R&D, and boost education.

This allows a country to start making more valuable products like cars, computer chips, appliances, TVs, ships, etc., and capture more of the added value on the way.

Service-Driven

This is the model followed by India. The idea is to directly skip the industrial stage and immediately target the growth of the service industry. This can include things like call centers, delocalized customer service, and software.

This is a more debated model, with the risk that the lack of an industrial base stays a handicap for the country. Good infrastructure, adequate education, and limited bureaucracy (quick Internet, stable power grid, good roads, clean water) are a must for it to succeed.

Many service-driven economies, notably India and the Philippines, also rely heavily on labor exports and remittances.

Infrastructure or Speculation-Driven

This is often the low-hanging fruit for many governments. Public spending on new highways, railroads, dams, real estate, etc., can create a lot of jobs and economic growth. And it “only” requires taking on a lot of debt.

This is by far the riskiest and less durable method of development. The resulting asset bubble tends to pop and might lead to decades-long periods of stagnation. Japan in the 1990s or Greece in the 2000s made that mistake, and it is possible that China is in a similar situation currently.

These economies can post exceptional growth figures for some time, which attracts many investors. If the investments driving the growth do not generate enough long-term ROI or if too much debt is incurred to finance them, this growth is not sustainable.

Specialization

This is usually a viable option only for small countries. It can be a focus on finance (Singapore) or IT (Estonia), or even tourism (Maldives, Belize). The idea is for the country to become excellent at ONE thing, counting on this sole activity to bring enough foreign currency to buy the other things the country needs and does not produce itself.

This can a sensible approach for small jurisdictions. Small countries with just a few million people will never be independent when it comes to the supply of chips, cars, or natural resources. So a good commercial balance and competitiveness in the chosen sector can be enough to produce quick results.

Sector Rotation with Development Stages

A good comparison to past patterns will also give investors an idea of what stage an emerging market is in. When a country starts developing, it usually sees a lot of growth in the same sectors for a given stage.

First, solving the most basic needs with a rise in:

- Cement consumption & production and real estate.

- Utilities (power, water).

- Agricultural tools and fertilizers.

- Simple consumer goods like AC, meat, bikes & motorcycles.

- Simple industrial equipment.

When the essential need of the population is more satisfied, other sectors take the relay, counting on the emerging middle class:

- Higher education.

- Basic healthcare.

- Advanced industrial equipment.

- Cars.

- Luxury goods (jewelry, imported liquor, …) and brands.

- Electronics.

- High-end real estate.

- Overseas and domestic tourism.

- Restaurants, cafes, and fast-food chains.

Finally, when a country really “emerged”, it starts to adopt developed countries’ consumption patterns.

This is also often a phase where the country is feared to soon “take over the world”, like Japan in the 1980s or China currently. While its growth is likely to actually slow down from there, contradicting simpler linear projections.

- “Luxury” healthcare like fertility clinics or cosmetic surgery

- Luxury cars.

- High-end electronics.

- Safety and social security nets (insurance, pensions, etc…).

- Sophisticated investments and finance.

- Legal services.

- Social media and entertainment.

Analyzing consumption and investment trends can help us understand the true development level of an economy.

Conclusion

Investing in emerging markets has been a very successful way to make money in the past decades. It is also now somewhat following well-studied and known patterns that can guide investors.

Nevertheless, this should not distract from inherent risks due to weaker rule of law or less than modern accounting practices. It is also possible that previous “recipes” fail due to the growing international tensions and the “deglobalization” trend.

As always, diversification will help reduce risks. Investors that spread their assets across several of the categories described above will see less volatility and less risk than those who focus on one type of emerging economy or a small group of emerging markets.

Emerging market investing requires more work, as each country has its own specific opportunities and problems. You can bypass some of that work with generalized emerging market ETFs or funds, but if you’re serious about emerging markets, you’ll want to look more closely at individual markets and their risks and opportunities.

Emerging Value

This is a series focused on opportunities in emerging markets. The goal is not to discuss breaking news. Instead, we will focus on long-term trends and lasting phenomena that impact investing in a country or region. It will also look at a selection of companies that might be worth a deeper look.

{kind=link}

{kind=link}