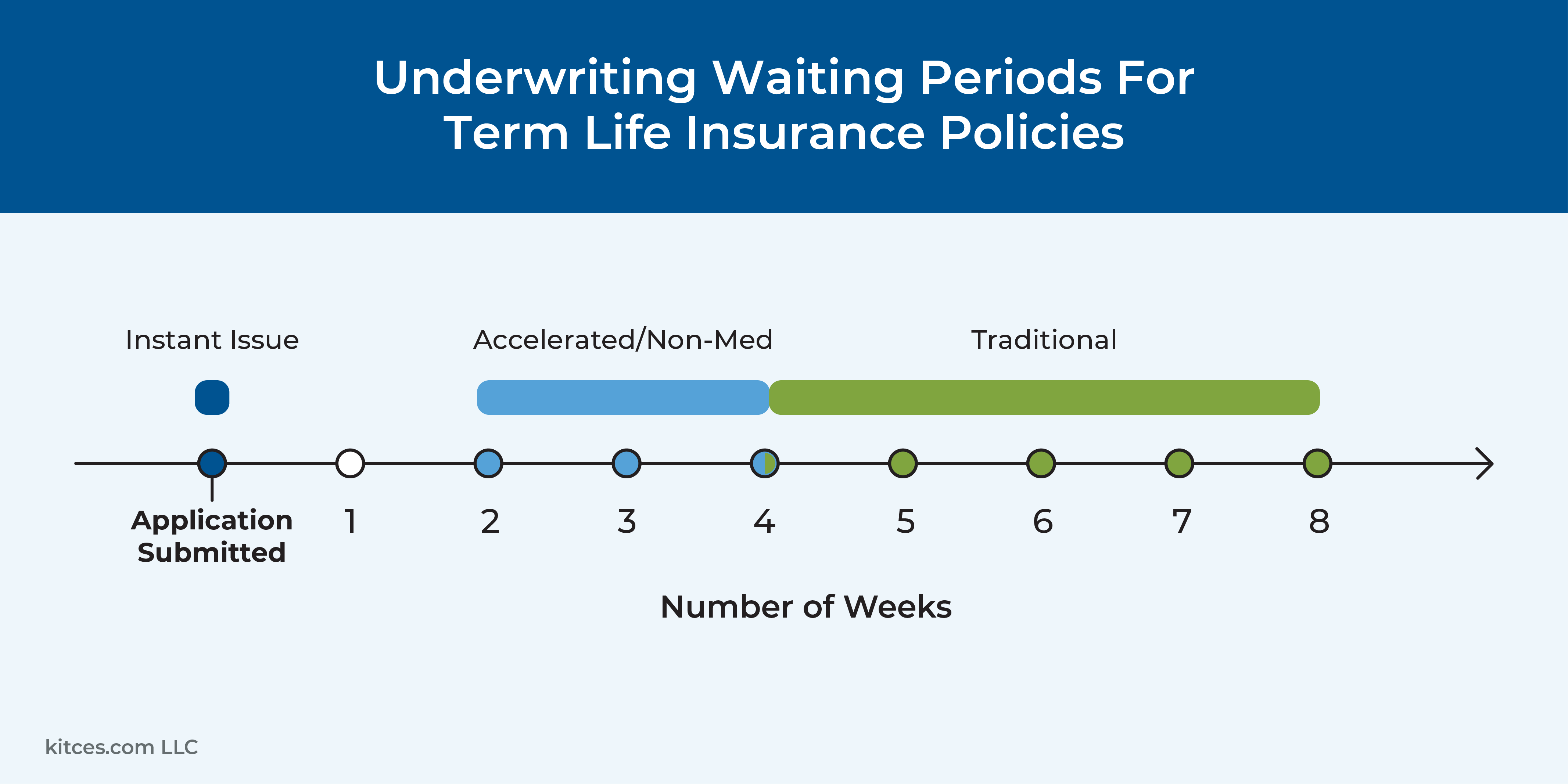

Traditionally, when a person applied for individual life insurance, they would need to go through an extensive underwriting process that lasted several weeks (or months) and may have included personal and family health questionnaires, interviews, and/or physical examinations. Though this process was time-consuming and intrusive from the perspective of the person applying for insurance, it was considered a necessary evil in order for the insurance company to feel comfortable issuing the policy on the person’s life. In more recent years, however, insurance carriers have increasingly offered “instant-issue” term life insurance policies, where a decision is made whether or not to issue a policy for a person within minutes of their submitting an application, with no additional underwriting.

Although these policies make it possible to fast-track the insurance application process for some individuals (who might otherwise be stymied by the traditional underwriting process), they aren’t necessarily right for everyone. For instance, because instant-issue policies require insurers to arrive at a decision without knowing the full details of an applicant’s current health or medical situation, they are generally only offered to the healthiest individuals – while those with pre-existing health conditions (who might still be eligible for insurance through the traditional underwriting process) might be declined after applying for an instant-issue policy. Which frustratingly can make it more difficult (or expensive) to subsequently be insured through traditional underwriting, since the fact of having been declined – albeit for an instant-issue policy with higher health standards than traditional underwriting – can create a ‘black mark’ on the individual’s health history.

Consequently, despite the convenience of instant-issue policies, it’s important not to automatically assume that they will always be the right choice for a person looking to apply for life insurance. Instead, it can be better to weigh the potential benefits of instant-issue (which, beyond the speed and convenience of obtaining coverage, can also avoid the scenario of a previously unknown medical issue coming up during underwriting and jeopardizing the person’s ability to obtain coverage) against the potential costs (which can include higher premiums than traditional underwriting, limits on the amount of death benefit available, and inability to convert to permanent insurance).

Financial advisors can play a key role in helping their clients weigh these factors against their own needs, and – in situations where the client just needs to get at least some coverage in place – guiding them towards a decision that will lead to action. Because ultimately, one of the greatest benefits of instant-issue life insurance is that it can make it much more convenient for healthier individuals to obtain life insurance – which could make it well worth the potential higher costs and other risks involved if the convenience of instant-issue is what catalyzes the client to actually get coverage to begin with!

{kind=link}