College is expensive and will only get more expensive over time. If you can get good college financial aid in terms of grants and scholarships (free money), as opposed to bad financial aid (loans), attending college will be much more affordable.

We’ve already talked about the different ways to pay for college. Now let’s discuss how we can get other institutions to pay for college for us!

After all, roughly half of working Americans don’t pay federal income taxes and society is fine with this reality. Why not let other institutions subsidize our children’s college education as well? A better educated public creates a stronger nation.

There is so much free money out there, we might as well learn how to game the college financial aid system.

Gaming The System Is What Rational People Do

Gaming the system sounds bad, but it’s not illegal. I didn’t say cheat the college financial aid system. We should all understand the ins and outs of any system in order to legally take full advantage of the benefits.

Examples of gaming the system:

- Multi-millionaires who game the health care system by getting subsidized health care.

- Retirees who game the system by doing a backdoor Roth IRA and then move to a no-income-tax state to save on taxes.

- Savvy people who game the system by simply reading great books because most people don’t read books anymore.

- Tenants who gamed the housing system in 2020 and 2021 by not paying rent because government passed new laws prohibiting eviction.

- Students and politicians who claim to be another race despite only being 1/1024th of that race.

If you haven’t thought about gaming the complicated college financial aid system, then maybe you don’t care enough about setting up you and your children for a better life!

The Income And Asset Threshold To Get Free Financial Aid

If your household earns up to about $300,000 a year and has $200,000 in assets or less per child outside of tax-advantaged retirement accounts, your family should be able to get college grants and scholarships. These thresholds will likely increase with inflation each year.

If this wealth profile fits your family, then this article should benefit your family immensely. If you make more or have more outside your tax-advantaged retirement accounts, getting free college money based on need will be difficult. You’ll need to go the merit route, which may be more subjective.

How To Game The College Financial Aid System To Get Free Money

Laurence J. Kotlikoff’s book Money Magic provides nine ways to lower the Expected Parental Contribution (EPC) figure on the FAFSA application, thereby increasing a family’s chance of getting free money. Kotlikoff is a Boston University professor.

- Contribute as much as possible to retirement accounts to limit the amount of your regular assets. If possible, arrange with your employer to receive more of your compensation as retirement contributions.

- Use your regular assets to pay down your mortgage. FAFSA doesn’t include home equity. However, certain individual colleges may incorporate home equity in computing a student’s financial need.

- Use regular assets to buy durables and personal collectibles, including easily resellable jewelry, which aren’t included in your child’s financial need calculation.

- Make your child’s grandparents the account holders of 529 plans, education savings accounts, and other college savings plans, since these assets will otherwise lower your child’s financial need.

- Defer taking capital gains on regular assets, which will factor in the government’s FAFSA income calculation.

- Save within whole-life or universal-life insurance policies. The cash value in these policies is generally not included in student-aid calculations.

- Defer withdrawals from retirement accounts, which would raise your FAFSA-measured income.

- Keep assets out of your child’s name. Your child’s assets and income will limit their aid.

- Defer getting married if this will lower your child’s calculated aid by increase your assets.

The goal of these nine strategies is to reduce the amount of income and assets in both the parent’s names and the child’s name attending college. The poorer both parties look, the greater the amount of good financial aid your family could receive from a college.

Let me touch upon a number of these strategies, including the missing obvious 10th strategy: make less money for at least two years before your child attends college.

What Is FAFSA?

The FAFSA is the Free Application for Federal Student Aid. It is a tool that schools use to evaluate students’ financial strength on a consistent set of metrics by calculating an Expected Family Contribution (EFC). It is based on the parents’ and student’s income and assets. Filing the FAFSA is an annual event for families of college students, starting in fall of senior year of high school.

To get the most amount of good financial aid, you want to get the lowest EFC amount possible. The difference between EFC and Cost of Attendance at a given college is your financial need. Starting in 2023, EFC will be referred to as Student Aid Index (SAI).

Your financial need will then largely be provided for by the university that accepts you or your child. The more the university wants a student, the more money the university will provide. Strategically, many universities will classify aid as “merit aid” to make prospective students feel better about attending.

If a student demonstrates exceptional financial need, then the federal government will step in and offer a Pell Grant. A Pell Grant is free money in the amount of $7,395 for the 2023-2024 academic year.

Parent Income on the FAFSA Is The Most Important Variable

The higher the parental income, the higher the EFC, and the lower the financial aid.

Parent income is calculated as Adjusted Gross Income, which means you have to add back all of your untaxed income, whether that’s your 401k contributions or tax-free interest, or a Roth IRA distribution.

You get an income protection allowance that’s roughly equivalent to the federal poverty level (FPL) for a family your size, and you subtract your tax liability– federal, state, and payroll taxes. It’s the most heavily-assessed at 47% for most families. That means that another $1,000 of income will raise your EFC by $470.

To game the college financial aid system, your household should earn the lowest AGI possible for at least the prior two years before your child attends college. In other words, your first FAFSA income year is when your child is a sophomore in high school.

If parents can earn lower income for four years before their child attends college, that’s probably safer. Hence, if you’ve ever thought about retiring early, taking a lower paying job, or simply taking a long sabbatical, the years before your child attends college makes sense. During this time, you can also consider doing a Roth IRA conversion since you’ll be in a lower tax bracket.

Parent income treatment on the FAFSA

Adjusted Gross Income

+ Untaxed income

– Income protection allowance

– Taxes paid

= Available income (AI)

- Rate between 22% – 47% of AI | $1,000 more income can translate to a $470 increase to your EFC/SAI

Parent Assets On The FAFSA Aren’t As Impactful

Curiously, the government doesn’t believe a high income translates into having lots of assets. Given the long-term median saving rate is in the single digits, the government knows the average American isn’t a good wealth accumulator.

As a result, only 5.64% of your assets is considered available to contribute to paying for college. In other words, if you have $100,000 in a brokerage account, it is expected you’d contribute only $5,640 of it toward college.

Given the low 5.64%, it’s still wise to save for college and your financial future. Every $1,000 you have in savings only adds $56 to your EFC, which means you come out ahead by $944. But if you want to game the college financial aid system, then you want to focus your savings in a retirement account.

Derivative thought: This low savings expectation of 5.64% by the government, improves the probability Social Security will be there for all of us in retirement. The government believes the average American is so bad at saving money that it must take care of us for social stability.

Assets That Count In The FAFSA Calculation

Reducing your income as close to $0 for two-to-four years before your child enters college is the most important way to game the FAFSA. Reducing the amount of recognizable assets you have on the FAFSA is the second most important way to game the system. But it’s much harder to do.

Below are the assets that count in the FAFSA calculation. Knowing what’s included will guide you toward how to spend, save, and rebalance your assets accordingly.

- All 529s owned by the parents

- Trusts for which you or your children are beneficiaries

- Your elderly relative’s bank account where you are joint owner

- UGMAs (Uniform Gift to Minors Act) and UTMAs (Uniform Transfer to Minors Act)

5.64% of the total gets added to the FAFSA | $1,000 more of assets translates to a $56 increase to your EFC/SAI

Assets That Don’t Count In The FAFSA Calculation

Here are the assets where you should accumulate as much as possible.

- Retirement accounts such as 401(k), IRA, Roth IRA, 403(b)

- 529 owned by grandparents

- Small business you own – not an asset so long as you or your directly-related family owns more than 50% and the business employs less than 100 people

- Family farm you live on and operate

Student Income And Assets Treatment On The FAFSA

Now that we know what parents need to do to game the FAFSA, it’s time to look at what students can do to get more free money.

The government will use 50% of a student’s reported income (above the protection allowance) when calculating EFC. Meanwhile, student assets count at 20% of their value, so an extra $1,000 in your student’s bank account will increase their EFC by $200.

Having your son or daughter take on a summer job before college will increase their EFC/SAI. Your children owning taxable brokerage accounts will also increase their EFC/SAI.

Therefore, perhaps think twice about making your children millionaires before 20. Maybe encouraging more YOLOing is a better strategy to enjoy life more and get more free college money.

The Ideal Wealth-Building Strategy For Kids Before And During College

Despite what I just wrote, the Roth IRA isn’t factored into the EFC/SAI calculation on the FAFSA. Therefore, all the more reason to open up one while your children are young to game the FAFSA.

Encourage your children to earn up to the maximum Roth IRA contribution amount each year and fully fund their Roth IRA. If the student income allowance is more than the Roth IRA maximum contribution, you might as well shoot for that amount.

This way, none of the student’s income or assets will count toward FAFSA.

Student Income Treatment On The FAFSA

Income (net of taxes)

-$6,800 allowance

50% of the total gets added to the FAFSA | $1,000 more income results in a $500 increase to EFC/SAI

Assets: no allowance.

20% of the total gets added to the FAFSA | $1,000 more income results in a $200 increase to EFC/SAI

The Net Price Versus The Sticker Price Of Attending College

Thankfully, the majority of private university students do not pay the sticker price due to financial aid and merit award. More college are also calling financial aid merit aid to woo students to matriculate given merit sounds better.

One of the reasons why colleges keep their tuition prices is high is due to signaling. The idea is that the higher the price, the higher the perceived quality. It’s called the “Chivas Regal Effect.”

Some families would happily paying $48,000 a year in tuition after a $10,000 “merit scholarship” versus pay the full sticker tuition of $45,000 a year and receive no merit scholarship at a comparable university.

A Good Financial Aid College Cost Calculator

Chances are high if your household makes $100,000 or less per child, your child can get financial aid. To see how much your family is expected to pay for college, check out Myintuition.org, a helpful financial calculator for colleges. It has a number of schools to choose from.

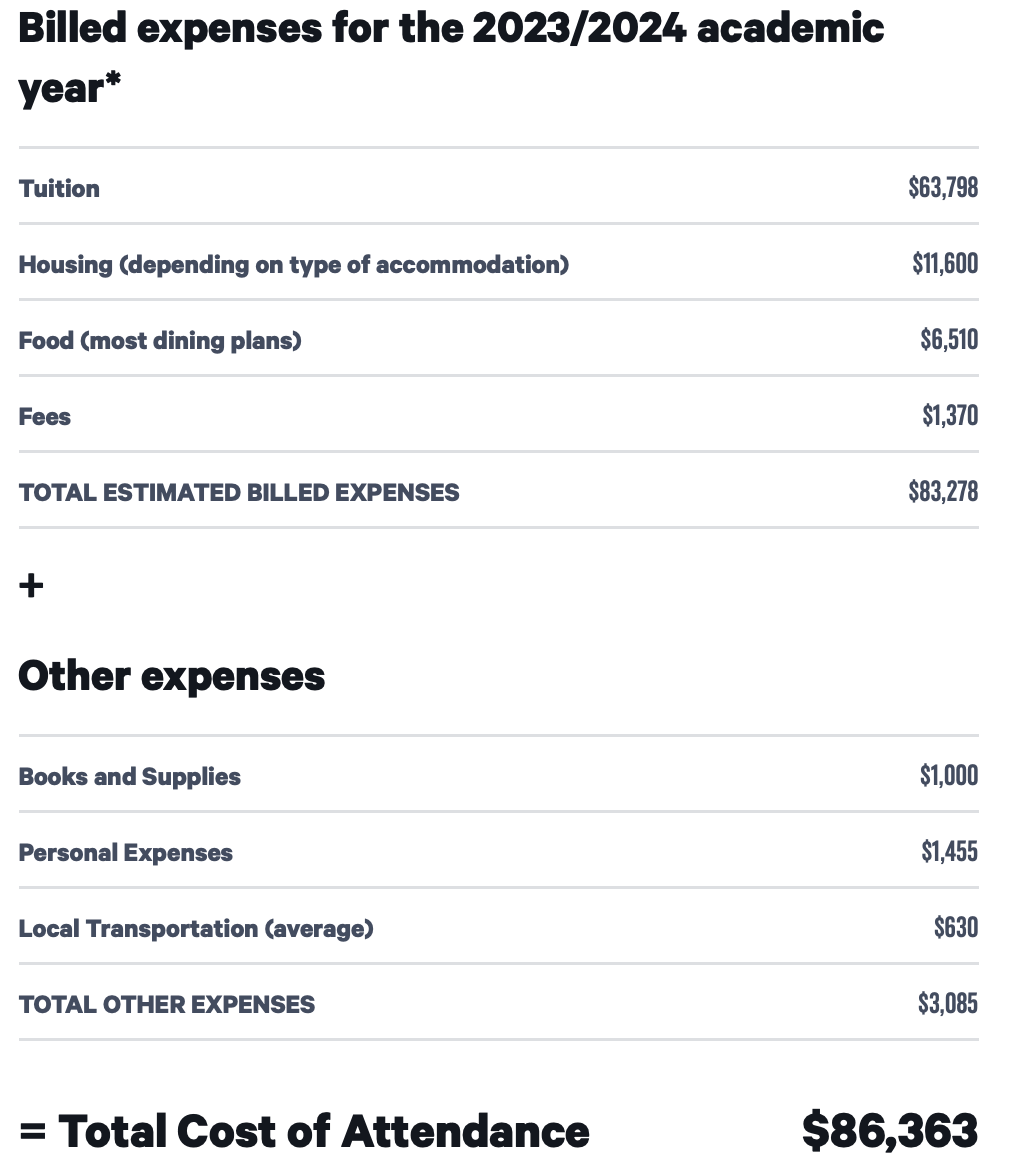

Boston University Cost Example: $86,363 All-In

- If parents have a combined income of $50,000 and $0 assets, the cost to attend BU will be at most ~$8,500, down from $86,363.

- If parents earn $100,000 annually and have $100,000 in the bank, BU’s maximum net price is ~$30,000, down from $86,363.

- If parents earn $100,000 but have all their savings in a 401(k), BU’s maximum net price is ~$17,000. Not bad!

Hard To Get College Financial Aid If You’re Mass Affluent

I highly encourage you to play around with the Myintuition.org financial aid calculator for different schools. You’ll soon discover that if you are part of the mass affluent class who reads personal finance websites and saves aggressively, good financial aid is hard to come by.

Take a look a this other example of an out-of-state student wanting to attend my alma mater, The College of William & Mary.

With a middle-class household income of $135,000, $10,000 in cash, $500,000 in a 401(k), and $350,000 in taxable brokerage accounts and a 529 plan, the household is expected to only get $4,700 in need-based scholarship. I’m not a fan of borrowing for college. And the $1,900 aid is in the form of student employment, which is not financial aid.

The key “problem” with this profile is the family’s $350,000 in non-retirement investments. If the family’s non-retirement investments was $0, the family would get $1,9740 more in need-based scholarship (free money).

Reduce Your Non-Retirement Investments As Much As Possible

To prove how much having assets outside of your tax-advantaged retirement accounts hurt, take a look at the below example. The family makes a handsome $250,000 a year and has an impressive $3,000,000 in their 401(k).

With only $10,000 in cash and $0 in a taxable brokerage account, no 529 account, and no investment properties, this multi-millionaire family will receive a $29,250 need-based scholarship!

What To Spend Your Non-Retirement Assets On

To get your non-retirement investments and cash down to $0, use them to pay down debt: credit card balances, auto loans, and your primary mortgage.

Given your primary residence isn’t included as an asset in FAFSA, if you’ve ever wanted to buy your forever home, consider doing so by your child’s sophomore year in high school.

Big expensive homes are the easiest way to spend down non-retirement assets. Although, strategically, the best time to buy the nicest house you can afford is when your kids are young. This way, more people can enjoy the home for longer.

Below is an example of a $4.5 million house that will easily suck up a lot of a family’s non-retirement assets. We’re talking a $2 million down payment and $18,605 a month in housing expenses.

Parents should also accelerate as many necessary expenses before filing the FAFSA as well. Expenses such as a new roof, exterior and interior painting, home remodeling, and replacing an old car are all considerations for spending down non-retirement assets.

If you’ve always wanted that $550,000 Ferrari SF90 Stradale, your time has come! YOLO baby! Although be careful, some schools will ask you what car you drive.

Imagine living in a $4.5 million house and driving a $550,000 car and getting free need-based money for college. Now that’s gaming the college financial aid system!

Perhaps Feel Fortunate You Can’t Get College Financial Aid

If you read Financial Samurai, then I expect you to eventually have an above average net worth for your age. It should be relatively easy to do given the government only expects the average American household to save 5.64% of their income.

By the time your kids go to college, the vast majority of you will likely also make above the median household income of $75,000. You will have found ways to get paid and promoted faster than the average person. You will also have started side businesses and worked side hustles to bolster your overall income.

Finally, I expect you to generate a noticeable amount of passive investment income by 50. After all, you’ve been aggressively building your taxable portfolio and rental property portfolio to have more options.

With this type of wealth profile, it’s too hard to game the college financial aid system to get free money. Sorry, you’re too financially healthy!

Your likely only hope to get good college financial aid is through merit scholarships. Hence, best to save as much as possible.

Perspective Of A Poor Student Who Attended An Expensive Private University

Let me conclude by sharing a very insightful perspective from a graduate who received a full ride at Boston University. Her household only made about $18,000 a year. Although, that’s reported income since she said her dad was a drug dealer.

For those of us lucky enough to earn or have too much to qualify for good financial aid, it’s good to remember that not everybody is as fortunate.

Reader Questions And Suggestions

Do you think it’s possible to game the college financial aid system to get free money? If so, what are some other strategies I haven’t discussed? If you or your children were able to get grants and scholarships, what do you think were the factors? Do you think trying to game the FAFSA is morally OK?

Plan for college better by signing up with Empower, the best free financial planning tool. With Empower, you can track your investments, see your asset allocation, x-ray your portfolios for excessive fees, and more.

For 99.99% less than the cost of college, pick up a copy of Buy This, Not That, my instant Wall Street Journal bestseller. The book helps you make more optimal investment decisions so you can live a better, more fulfilling life.

Join 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

{kind=link}