CNA Insider recently released an eyebrow-raising documentary that explored the state of personal finance among the younger generation today. To tell the truth, there were a few things that shocked me in the video, hence I’m penning this today in hopes that it’ll inspire a change.

To all the young Singaporeans who find themselves in a similar situation, I can only hope that my letter reaches you before it is too late.

You see, it is easy to take your finances for granted. We never really know the meaning of something until it is lost, and that includes money. But I pray that you will not have to wait until that day comes in order to realise it.

Maybe I was lucky for having learnt this lesson early as a child. Having grown up in a family where money was almost always a sensitive topic, and seeing my mom land into debt just to keep our household going after she got unexpectedly laid off during the Asian Financial Crisis…that cemented this belief in me that I never want to end up in the same situation. And that’s the reason why I save, spend and invest like I do, including exploring and implementing the various hacks and methods that you’ve seen me write about on this blog.

Your 20s is the best time to build a strong foundation

Not just for your career, but also your financial health.

Maybe you don’t realise it yet, but your 20s is the best time for you to build strong financial habits that will serve you for the rest of your life. The savings, insurance and investments that you make in your 20s will greatly shape your life in your 30s, 40s and beyond. The question is, what life do you want to design for yourself?

When I landed my first job, I aimed to save $20,000 every year while on earning $2,500 from my corporate job. It was hard in the first few years, but I did it – and the sense of satisfaction that followed was incredibly rewarding because it made me realise, I can do hard things.

That came in handy again much later when I was struggling to lose weight. Same same but different. The result? I lost 20kg in under a year, a feat that even I myself never believed possible…until I achieved it.

Later, as I climbed the corporate ladder and my income rose, the financial discipline and habits that I built in achieving my first $20k allowed me to resist lifestyle inflation and grow my savings even faster. Later, when I learned how to use money to make more money, that growth became exponential.

Now, as a working mother of 2, I no longer have time to track my expenses or do some of the stuff that I used to be more diligent about when I was in my 20s and managing my finances. But you know what?

It hasn’t gotten more difficult, even though I have a lot more people to plan for now.

All thanks to the habits and financial discipline that I consciously built and enforced in my 20s.

Learn to build healthy financial habits from the get-go, instead of letting your environment (and advertisers) shape your financial life – one which sees you slowly getting used to spending more and more for little luxuries, until you can no longer go back to your old way of life.

Self-care is important, but retail therapy is not the answer.

I know, self-care and mental health is important, but retail therapy is not the answer.

Using retail therapy to make yourself feel good is keeping you in the hedonic treadmill. Here’s the neuroscience behind retail therapy. And the scariest part? Over time, you’ll need more and more of it.

When we say spend “within your means”, it is not just about how much you can afford to spare today, but also how much you’re taking away from your future.

You see, every dollar spent could have been a dollar saved and invested. So it is not just that $20 for that taxi ride, but over time, that $20 could have grown to so much more.

Ok, I’ll confess, I had my own indulgences too. When I was in my 20s, as a reward for working hard at my job, I treated myself to a movie every week, and a new dress every month. But these came with some rules that I set for myself: the movie ticket had to be less than $10 (so if I wanted to watch on weekends, I had to find ways to reduce the price), and each dress could not exceed $28. What’s more, if I couldn’t see myself wearing an outfit at least 10 times, then I wouldn’t allow myself to buy it.

Don’t allow yourself to get addicted to the dopamine release of retail therapy; try finding other ways that don’t cost you as much instead.

How much are you saving?

With the rise of personal finance content, it can be easy to feel like you’re doing well when you follow the “recommended guidelines” for saving / spending / investing.

But guidelines are just guidelines. Whether or not 20% or 50% is better for you is a question that only you can answer.

The other thing to think about is, does meeting these “recommended guidelines” produce a placebo effect or an actual impact on your financial health?

In this case, Joey felt she was doing “well”…until life threw her a curveball in the form of her dog getting cancer, which then wiped out all of her savings.

And that is what life does – it throws us curveballs (often expensive ones) when we least expect it. You literally can go from “doing well” to “broke” overnight.

Which is why having emergency savings – on top of your savings for longer-term needs like retirement / a house / your wedding – is so important. Because when emergencies hit, you don’t always get the chance to work and earn the money to pay for it.

Learn to figure how much you need to put in your emergency fund here.

Debt is a double-edged sword

I know how tempting it can be to spend on credit, or to even buy something because it went viral on social media. Buy Now Pay Later (BNPL) services aren’t making it any better, but you should know that the item is not more affordable just because you’re paying less for it now.

Sometimes, it is better to pay in full so you feel the sting of what it really costs you when you buy it.

The next time you’re tempted to buy something using BNPL or spend on credit, try applying this second rule: can you pay it off every month even if your financial circumstances change?

E.g. if you lose your job tomorrow, can you still upkeep the instalments?

If the answer is no, then maybe you should walk away from that purchase.

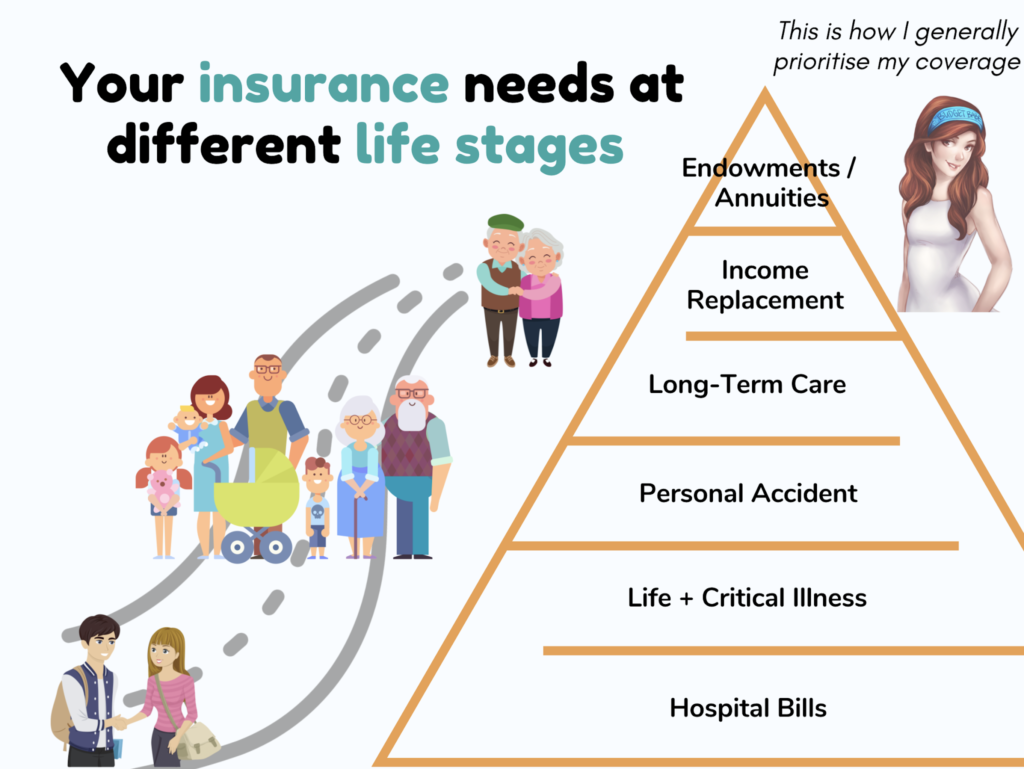

How much insurance is enough?

It is easy to conclude from the video that to avoid having one’s life savings wiped out (like Joey), just go get insurance!

But before you rush to meet your insurance agent, you might want to take a look at this first:

After taking care of all those premiums, will you still have enough for pet insurance?

Of course, you can try to predict some and hence protect yourself against it, which is why insurance exists. But for the most part, we don’t get to accurately predict everything that eventually happens to us.

What if, in an alternate scenario, Joey had bought pet insurance for her dog but ended up being served another curveball instead?

Everyone will tell you to buy, but how many will teach you how to say no?

When a product goes “viral”, it can be tempting to buy it. But just because it is good for many people, is it necessarily going to be good for you (and your pocket)? More importantly, does the product truly serve YOU?

It is the job of advertisers (and arguably, influencers too) to entice you to inflate your lifestyle as you go along, but it is your job to learn how to resist it.

But you must first want to act on it.

If you find that your social media consumption is making you spend more than you otherwise would have, then perhaps it is time to rethink the type of content you choose to expose yourself to.

Out of sight, out of mind.

For me, I have zero temptation to buy blogshop clothes because I (consciously) don’t follow their Instagram accounts or subscribe to their email lists. But last year after I successfully lost weight and could fit into smaller-sized apparel again, I started following my (current) favourite clothing brand on Instagram. Their clothes are not cheap either, starting from $70 a dress. Without realising it, I found myself having 5 Claude dresses in my wardrobe. Then it hit me – that was wayyyy too much. So I unfollowed the account. But then Instagram served me the ad in my feed again, and now I’m feeling tempted to buy two dresses from their latest launches once more.

It gets harder to say no when it is in front of you.

That’s why YOU have to be the one training yourself how to say “no”.

Learn to invest

Ok, I’m already hearing some of you complain: so what’s the point of reducing one’s expenses and saving more money? Where’s the joy in that?

Look, I’m not telling you to cut down until you no longer have any joy in life. Instead, what I hope you can see is that there are plenty of joys that money cannot buy.

Move away from the tangible, material goods. These are fleeting, and they don’t last.

Instead, invest in your future and you’ll find the joy in having attained financial freedom.

Invest in your relationships and you’ll find the joy in having loved ones to walk this journey of life with, so you’ll never be alone.

Invest in your health (even if it means ditching paid workouts for free Youtube ones) so that you’ll experience the joy of mobility and functional strength.

It gets easier when you build (right) from young.

Or you can choose to ignore this rambling woman in her 30s. I mean, that’s the easier way, isn’t it?

Or do you want to start by building and designing your financial life today for true freedom? I’ll gladly point you in the right direction if you do.

With love,

Dawn

{kind=link}