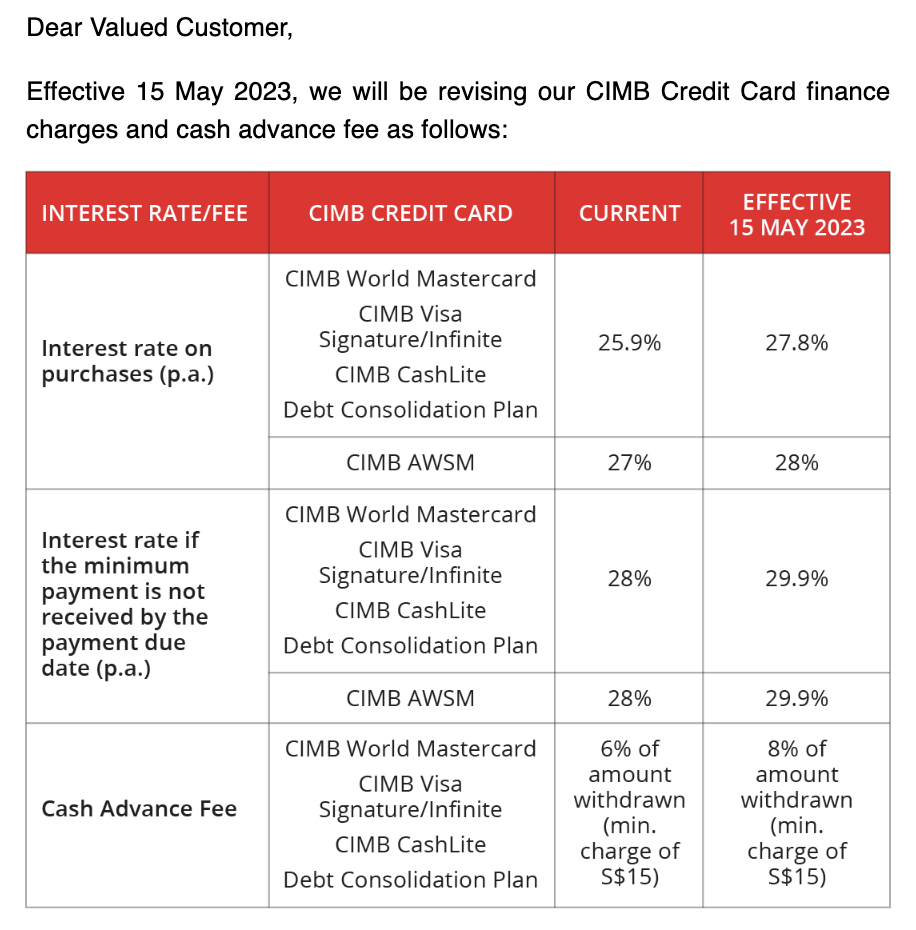

CIMB recently announced a hike in their interest rates for credit cards, which will come into effect next month. Here’s a look at the changes, as well as the prevailing late fees and interest rates right now at the other banks and credit card issuers.

I shared this on my Instagram and many of you DM-ed me to complain about the higher rates. While it is important that we consumers take note of the changes, it is also worth highlighting that we don’t have to worry about them unless we miss or forget any payments.

With this, I decided to check out where the latest interest rates and late fee charges by other banks are at right now, and some tips on how to avoid being charged these fees.

The CIMB announcement that came out earlier today:

At a glance, it seems like CIMB is the first to change their fees (so far in 2023). We’ll have to keep an eye on whether this prompts any of the other banks or issuers to follow suit, so I’ll update this article if that changes later on.

Late fees

This refers to the immediate charge you get slapped with once you miss a credit card payment. For every month that you’re late, you get charged another $100 / month.

The scary part is when you don’t even realize you’re in arrears, and unknowingly get charged $100 every month (even if it is just 1 cent that you owe). And guess what? This $100 fee also incurs interest charges!

Interest Rates

You get charged an interest rate for any outstanding amount that you’ve not yet paid to the bank or credit card issuer (a.k.a. the cost of borrowing). Yes, this means that even if you’ve made the minimum payment and still have $800 outstanding, the bank will levy interest on your $800 remaining sum until everything has been paid off in full.

CIMB may be the bank with the highest interest rate right now, but I won’t be surprised if we see more banks raise their interest rates soon in the coming months.

Why credit card fees can be so insidious

Like most financial instruments, credit cards can be good or bad, depending on how you use them. As long as you’re disciplined about paying off in full each month, you will not have to worry about any charges and can fully enjoy the perks e.g. cashback / miles earned / rewards / merchant discounts / extra interest on your savings account.

However, the trouble starts when you forget, or fail, to pay your credit card bills in full before the due date. And when you have multiple credit cards – each with different billing cycles – it can be easy to overlook the payment for one or two cards.

Source: MoneySense

What happens then?

- You’ll be charged interest on a daily basis for your outstanding amount

- Any interest not settled by the next payment due date will also attract interest in the next statement, on top of a $100 late fee

In short, any unpaid amount will be rolled over to the next bill, and you’ll be charged interest on top of your interest and capital. That’s how credit card debt can easily snowball if you’re not careful / not paying attention!

Strategies to avoid credit card fees

Personally, I use 2 methods to help me avoid unwittingly being charged these late payment fees:

1. Check your bills twice a month

Set a calendar reminder in the first and last week of every month to check on your billing cycles. Why twice a month? That’s because credit card payments are due at the end of a billing cycle, but the length of a billing cycle differs between banks.

For some, it begins from the time you activate the card, whereas some banks set it based on when you made the first charge or purchase on your card.

Hence, the fail-proof method would be to check near the start and the end of every month, because that pretty much covers you for all cycles.

2. Sync your credit card billing cycles

Ideally, you’d want to sync all your credit card billing cycles to coincide with each other so that you can simply log in once, check everything at one go, and clear all payments in a single instance.

However, that is easier said than done. What’s more, some banks have billing cycles of 25 days, whereas others have 30 – 40 days, so even if you call in to set the same start date for each credit card, you may still receive different statements on different dates and have to deal with different payment due dates, which get further and further apart as the months go on.

Honestly, as long as you have multiple credit cards across different banks (which many of us do), it can be hard to keep track! Hence, while you do your best to sync up all the respective billing cycles, don’t forget to keep up with Tip #1 so that you never risk falling behind in payments.

Conclusion: Pay off your credit cards in full every month

I’m an advocate of credit cards and I almost never spend anything in cash / debit, because doing so means I lose out on the cashback and miles that I can get for each dollar spent. Not worth it, especially when I’ve to spend the same amount regardless.

But using credit cards wisely also requires financial discipline, because as you can see, the late fees ($100 per month!!!!) and rolling interest rates are simply NOT worth it.

Be a savvy credit card user by milking all the benefits and rewards, while NEVER paying for any late or interest fees if you can help it.

With love,

Budget Babe

{kind=link}