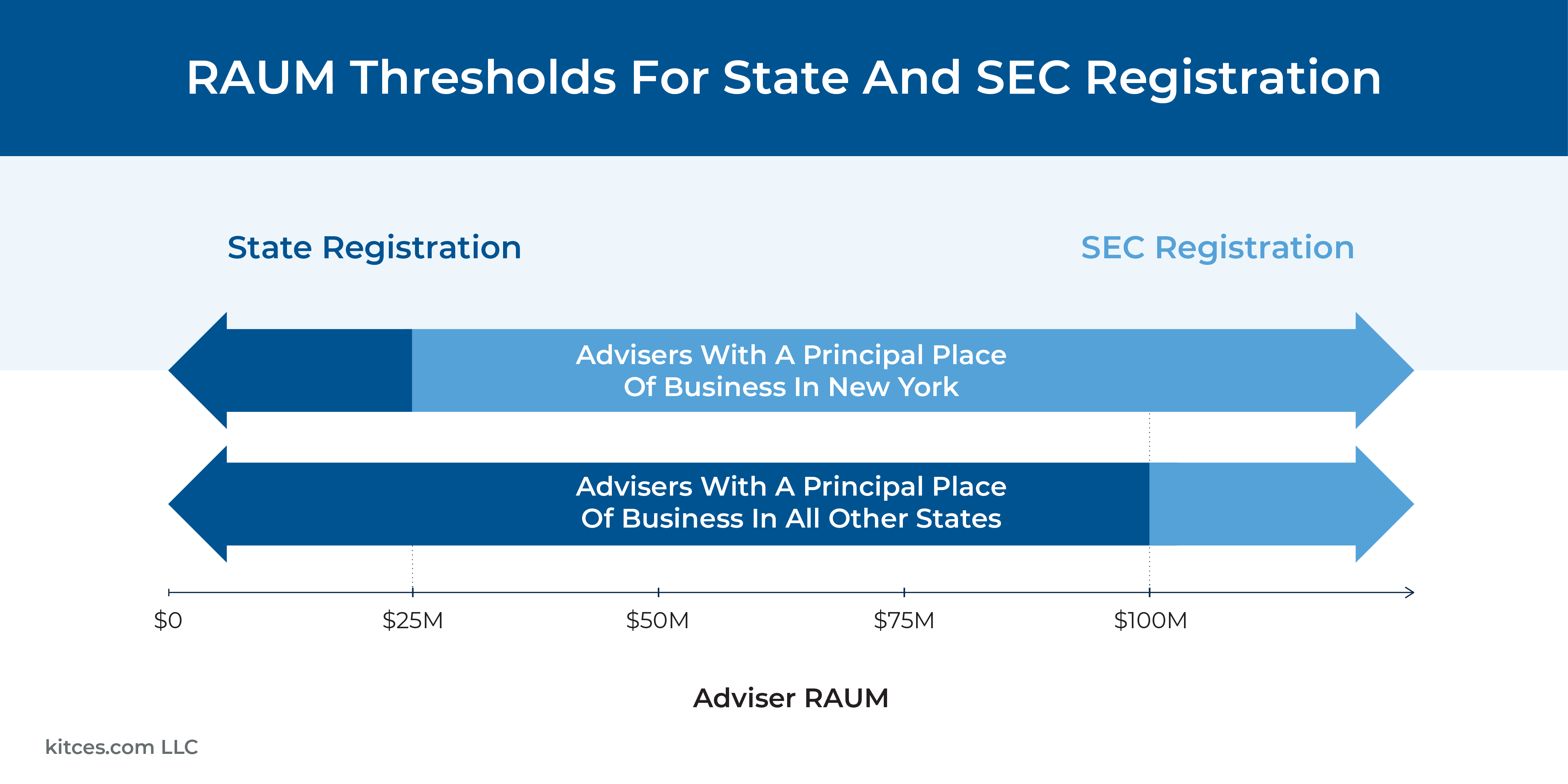

When an RIA reaches the threshold of $100 million in Regulatory Assets Under Management (RAUM), it must generally switch from being registered at the state level to registering with the SEC. But while $100 million may be the general rule, in practice it isn’t always a hard line. The reality is that volatile markets and shifting client bases can often cause an RIA’s RAUM to flutter above and below the $100 million line. And because of this, the SEC includes several wrinkles in its registration rules that allow RIAs some leeway in deciding when to become SEC-registered.

For state-registered RIAs, it’s helpful to know when it’s possible (and when it’s required) to register with the SEC, particularly for firms near the $100 million threshold for SEC registration. Conversely, for RIAs who are already SEC-registered but whose RAUM is close to crossing below the $100 million threshold, it’s useful to know when it would be necessary to switch back to state registration.

The first important guideline in knowing when to register with the SEC is understanding that the registration requirements are generally triggered by the RIA’s year-end RAUM as reported on Form ADV, Part 1A. Firms that cross the threshold midyear may register if they choose to do so, but only after their Form ADV update is filed does the switch become required. Additionally, there is a ‘buffer zone’ for state-registered firms with RAUM between $100 million and $110 million at the end of the year in which they may (but aren’t required to) register with the SEC – meaning that state-registered firms aren’t truly required to become SEC-registered until they have at least $110 million at year-end!

Similarly, there is a buffer zone of RAUM between $90 million and $100 million for SEC-registered firms where they need not deregister (and revert to state registration) until they’ve crossed below $90 million of RAUM at year-end. Notably, however, if RAUM crosses back above $90 million at any time during the 180-day period following the end of the RIA’s fiscal year, it can opt against deregistering and remain as an SEC-registered firm (at least until the end of the year, where it could face the same situation if RAUM again crosses below $90 million).

Ultimately, what’s important for investment advisers to remember is that they may have options in deciding when to register (or deregister) with the SEC, and that the best strategy might be determined by how they expect their assets to change and, most crucially, what will keep them from needing to go through the opposite process in the near future. Because even though investment advisers only need to contemplate registering or deregistering once per year, once that decision is triggered it becomes a complex process requiring a lot of paperwork and careful timeline management to avoid a gap in registration – which few firms would want to go through more than once!

{kind=link}